New Mexico: BCBS drops out as expected, avg. rate increase plummets (sort of)

Fri, 08/28/2015 - 4:58pm

When I last checked in on the ongoing saga between the New Mexico Insurance Commissioner and Blue Cross Blue Shield of New Mexico, BCBS was threatening to take their ball and go home if NM Insurance Commish John Franchini didn't cave and agree to let them jack rates up by 51% on the individual market (Franchini had agreed to a 24% hike instead).

Well, Franchini called BCBS's bluff...but they weren't bluffing:

Thousands of New Mexicans will need to shop for new health insurance plans later this year after a decision by Blue Cross Blue Shield to stop offering individual insurance plans through the state health exchange beginning Jan. 1.

...The letter said Blue Cross Blue Shield of New Mexico lost $19.2 million in 2015 on the 35,000 individuals covered by plans they purchased on and off the exchange.

...Blue Cross will offer a basic-level insurance plan outside the exchange in 2016, which will be available to all consumers at the same rate as in 2015.

...Insurance Superintendent John Franchini earlier this month rejected Blue Cross Blue Shield’s request for a rate increase averaging 51.6 percent. Franchini said he was prepared to instead approve a 24 percent increase and was waiting for Blue Cross Blue Shield’s response.

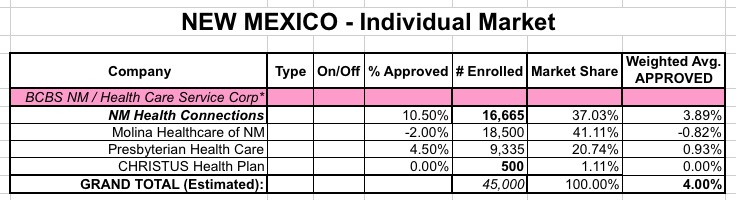

He had approved much smaller rate increases for the other insurance companies that offer plans on the exchange – Presbyterian Health Plan, Molina Healthcare of New Mexico, Christus Health Plan and New Mexico Health Connections.

As for the other companies, 3 of them are pretty nominal (4.5% for Presbyterian, a 2% decrease for Molina and no change at all for Christus), while NM Health Connections was approved for a 10.5% hike (they'd requested 14.7%).

UPDATE: Thanks to Colin Baillio for this additional link which gives a better idea of the relative market share between the other 5 companies.

Officially, with BCBS off the table, this means that the "weighted average rate increase" for New Mexico's individual market has actually dropped dramatically for the other enrollees: From around 11.7% (or 24.5% if you use BCBS's 51% request) to just 4.0% or so:

Of course, realistically, this is pretty misleading, since Blue Cross's 35,000 enrollees will have to go somewhere, and I have no idea whether they'd be looking at rate hikes, rate cuts or roughly the same premiums if they make the move to one of the other four companies in question. Companies have dropped out of other states as well (most notably Assurant across multiple states), but this has a huge impact on New Mexico's tiny risk pool; it's similar to PreferredOne dropping out of MNsure in Minnesota last year.

Anyway, don't cry too hard for Blue Cross; they got their losses back:

Blue Cross actually lost more than the $19.2 million the company cited in the letter Wednesday but received more than $23 million from a pool set up by the Centers for Medicare and Medicaid Services to help insurers offset unusually high claims. The pool is financed with mandatory contributions from insurers.

Advertisement