You got Individual Market in my Small Group! You got Small Group in my Individual Market!

Wed, 08/10/2016 - 6:19pm

(as whoever posted the commercial to YouTube noted, "Seriously, who struts down the sidewalk munching on a jar of peanut butter?")

I've written quite a few times before about how the small group insurance market is sort of the odd man out when it comes to the Affordable Care Act. The SHOP exchanges have turned out to be mostly a dud (to the point that the HHS Dept. has only stated once just how many people are even enrolled in SHOP policies (and even that was missing some states; my best guesstimate is arouns 150,000 nationally).

There was, in the early days of the ACA, some controversy over just how large a "small business" could be defined as--the law bumped it up from 50 employees to 100, though this provision was later repealed, keeping 50 as the cut-off point.

In terms of the size of the small group market, I know it was around 17 million people in 2013, but has since shrunk to around 13.5 million today.

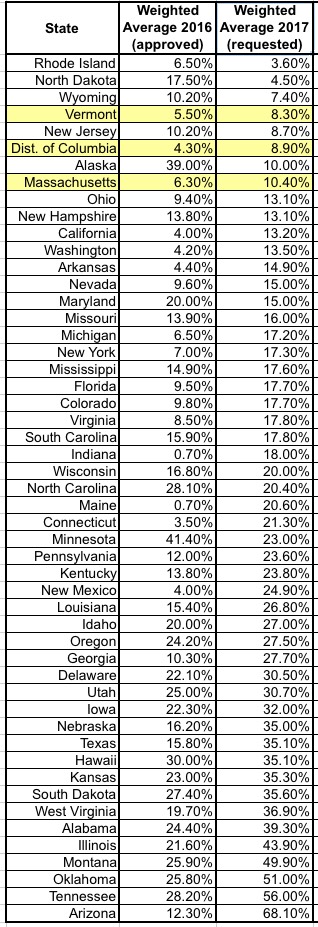

Massachusetts, Vermont and the District of Columbia all have laws/regulations which combine their small group risk pools with those of their individual markets, which makes total sense to me from a sheer simplicity POV. However, as someone who wishes to remain anonymous has brought to my attention, there's a far larger benefit to be had from merging the Indy and Sm. Group markets together:

In reading your 2017 premium increase post, I'm prompted to revisit what I've long considered a great problem with the ACA: It lumped a lot of high risk people (formerly uninsured due to pre-existing conditions) into a relatively small risk pool, the individual market. It should be no surprise that this drove up premiums in this pool. If you look at your 2017 data, it appears to me the states that merged small groups with the individual market will have increases near the bottom end. This makes sense, since the high risk expensive people were averaged across a larger pool. I don't see much if anyone commenting on this issue, but it appears to me to be the single most important factor on ACA premium escalation. It needs to be discussed more widely. Perhaps you could do a blog post on the issue.

Consider it done! This is an interesting point...and when I look at the requested rate hike table, sure enough, here's what you get:

Consider it done! This is an interesting point...and when I look at the requested rate hike table, sure enough, here's what you get:

As you can see, the writer appears to be onto something here. I've posted the weighted average increases for both 2016 (mostly approved) and 2017 (requested only); they're sorted out from lowest to highest by the 2017 requests, and all three "merged risk pool" markets come in at the low end of the range. Last year there were a couple more states which came in lower, but all three were still very much towards the bottom end of the scale.

The problem as I see it is that while the cost of subsidizes was socialized across all tax payers, the cost of premiums for these high risk people was largely dumped on just the backs of those in the individual market, and for those in that market who get no subsidies, it has been very painful.

Why wasn't the premium risk spread across all insured individuals, rather than singling out those of us in the individual market for the brunt of it. I know we didn't take it all, because some fraction of the formerly uninsured get jobs and switch to group plans, and some went on Medicare, etc, but a large fraction would have gone into the individual market, and that has driven premiums there up significantly. ACA supporters tend to counter that subsidies in the individual market counter this, but that is only a means tested solution, and it leaves many individual of moderate means with huge increases that essentially have decimated their standard of living. My wife and I make about $60K/yr placing us just at the cut off, and our insurance has gone from <4K/yr to what looks like will be abour $14K/yr in 2017, which has wiped out all discretionary spending, and most savings as well. All because the cost of the formerly uninsured was normalized over a relatively small fraction of the USA population, which for some reasons was chosen as a target. Why I'm not sure.

This is, in my view, an important point. Regular readers know that while I do generally support the ACA, I also prefer to look at rate hikes across the entire individual market as a whole (on + off-exchange) instead of limiting myself to the exchange enrollees...for the very reasons noted above. It's awesome that around 9.4 million people are receiving APTC assistance...but there's another 10 million or so people who are in the same risk pool but have to pay full price (roughly 1.7 million on-exchange and another 8 million or so off-exchange). As it happens, depending on the year (I have a highly variable income), I might find myself in one of these populations or the other...and the full price premiums are, indeed, getting pretty ugly for a good 10 million of us.

Anyway, if you have time, and can bring your excellent talents to this angle, it might help prompt others to think more on it, and perhaps a better solution will evolve over time. Vermont, DC, and Mass I think are the states with merged pools, and they have relatively low increase requests per your tables. It would be interesting to compare their history over the prior years. One would assume the group rates went up more, since the individual rates went up less. But at least the pain is spread over more people. IMHO, it should be spread over everyone, not just some particular group being singled out.

If you merge the risk pools for the individual and small group markets in every state, instead of having two risk pools (19 million & 13.5 million), you'd have a single pool with around 32.5 million people...roughly 10% of the total population. You'd basically be shifting about 40% of the burden on the indy enrollees over to the small group enrollees, so I'm sure there'd be a lot of grumbling about it, but obviously MA, VT & DC managed to get this done.

Sounds like a good idea to me. Thoughts?

Advertisement