Huh. This is interesting...after a couple dozen states with near-flat or even reduced 2020 premiums, Louisiana is just the third state I've come across where the carriers are seeking double-digit rate increases for next year.

There's actually only 3 carriers offering individual market plans in Louisiana, but there's seven listings because two of the carriers have broken out their submissions into several different product lines. Overall, HMO LA, LA Health Service & Indemnity (Blue Cross Blue Shield of LA) and Vantage Health Plan are requesting average premium increases of 11.7% statewide.

I should note that there's also one odd listing (see second screenshot below), from UnitedHealthcare. It claims to be for off-exchange ACA-compliant individual market plans, but two things about it make no sense:

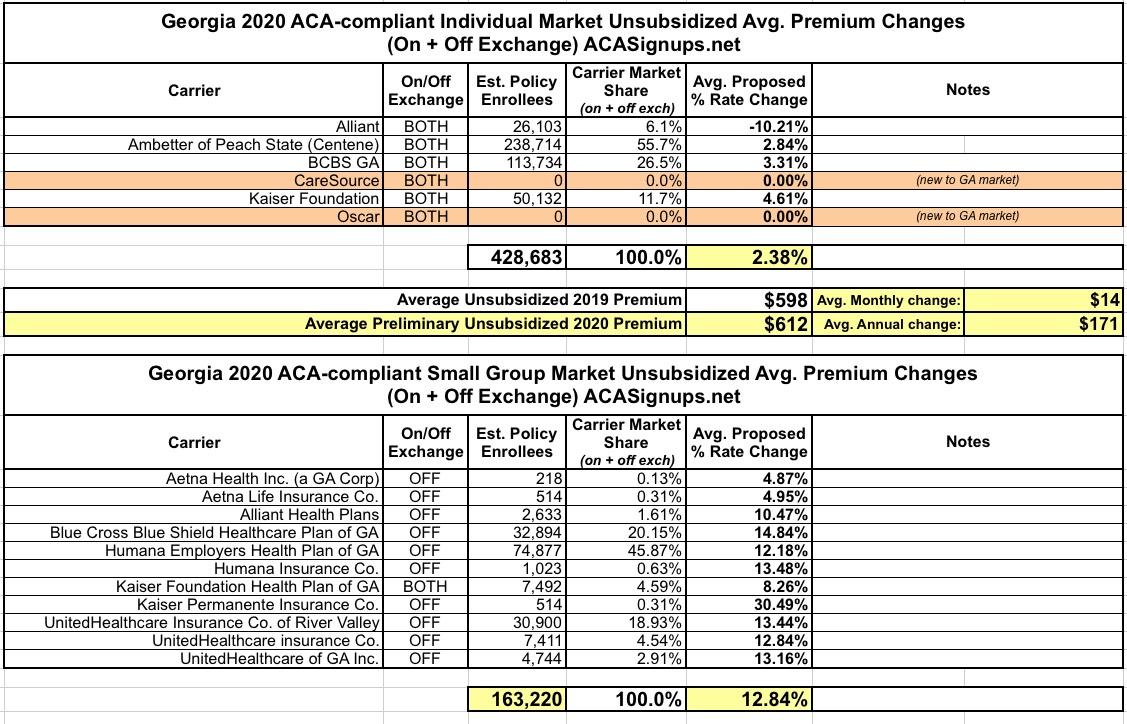

After several years with four carriers participating in their ACA individual market, the Peach State is gaining not one but two additional carriers this year: CareSource and Oscar are joining Alliant, Ambetter/Centene, Blue Cross Blue Shield and Kaiser. Unlike a lot of the states I've crunched numbers for recently, I was able to acquire hard enrollment numbers for every single Georgia carrier...including both the Individual and Small Group markets, which is a rarity this year!

Statewide, GA's individual market carriers are requesting average unsubsidized 2020 rate hikes of just 2.4%, while the small group carriers are looking for a 12.8% average increase:

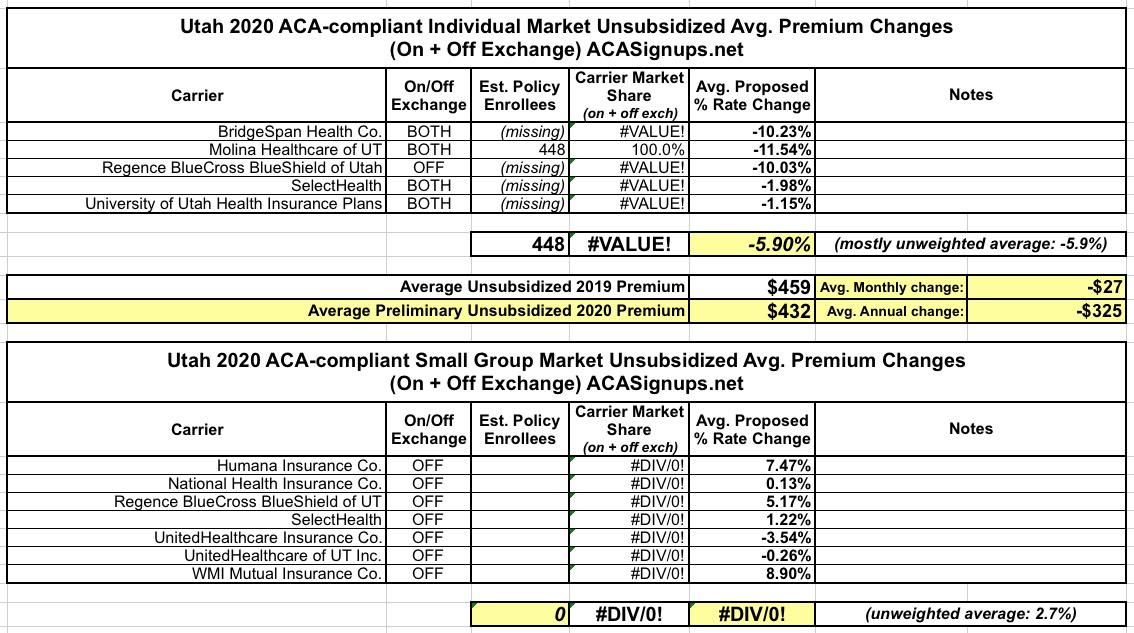

(sigh) The good news is that none of the five carrier rate filings for Utah's individual market have been redacted. Hooray! The bad news is taht only one of the five (Molina) included their current enrollment total on the filing at all. Boo!

As a result, I'm only able to run a "mostly" unweighted average...that is, it's an unweighted average of the other four carriers, plus a slight additional tweak based on the tiny number (448 people) enrolled in Molina policies. Utah's total individual market should be around 240,000 people, so that's barely a rounding error. My best guess is that unsubsidized enrollees are looking at roughly a 5.9% average premium drop next year.

For the state's small group market, the unweighted average increase is 2.7%.

West Virginia has three carriers offering policies on the Individual Market: CareSource, Highmark and The Health Plan of WV (aka Optum). I was ble to find the hard enrollment number for CareSource, while both HighMark and Optum are redacted, so I based my enrollment estimates on 83% of last year's (WV's total ACA exchange enrollment dropped 17% this year). Even if that ratio is off, it won't make that much of a difference since the two are pretty close anyway (+5.9% and +6.5% respectively).

Statewide, unsubsidized West Virginians will be seeing roughly a 6.7% average increase...to a whopping $1,000/month on average, one of the highest rates in the country. Of course, WV is also one of the few states which, to my knowledge, is still refusing to Silver Load or Silver Switch their premium increases, which makes it even worse for the few unsubsidized enrollees they have.

Meanwhile, the unweighted average increase on the WV small group market is +11.2%.

Just hours after explaining what a dramatic impact the nearly-flat average 2020 premium changes are going to have on this year's (and next year's) Medical Loss Ratio rebate payments, I've discovered that rates are going to be increasing even less than I thought nationally.

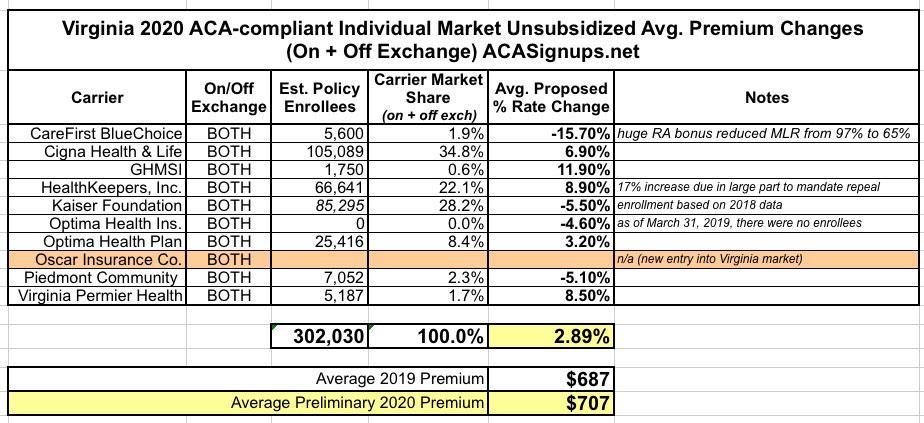

Back in late May, Virginia was one of the first states to post their preliminary 2020 premium rate filings. At the time, the 10 carriers participating in VA's individual market (one of which is new for 2020) were asking for average increases of 2.9% statewide:

For weeks now, my blog posts have been overwhelmed by my state-by-state analysis of the preliminary 2020 ACA individual market rate filings. With the addition yesterday of Illinois, Hawaii, Iowa, Kansas and especially Florida, I've now accounted for over 75% of the total ACA Individual Market nationally.

I still have a dozen states to go, including large ones like Texas and Georgia, but barring some devastatingly huge rate hikes, the picture is clear: Average unsubsidized 2020 ACA individual market premiums will only be going up an average of less than 1% nationally.

I've now analyzed the preliminary average (weighted or, in a few unfortunate cases, unweighted) premium change requests for over 3 dozen states. Of the dozen or so left, the largest states unanalyzed are Georgia, Texas...and Florida.

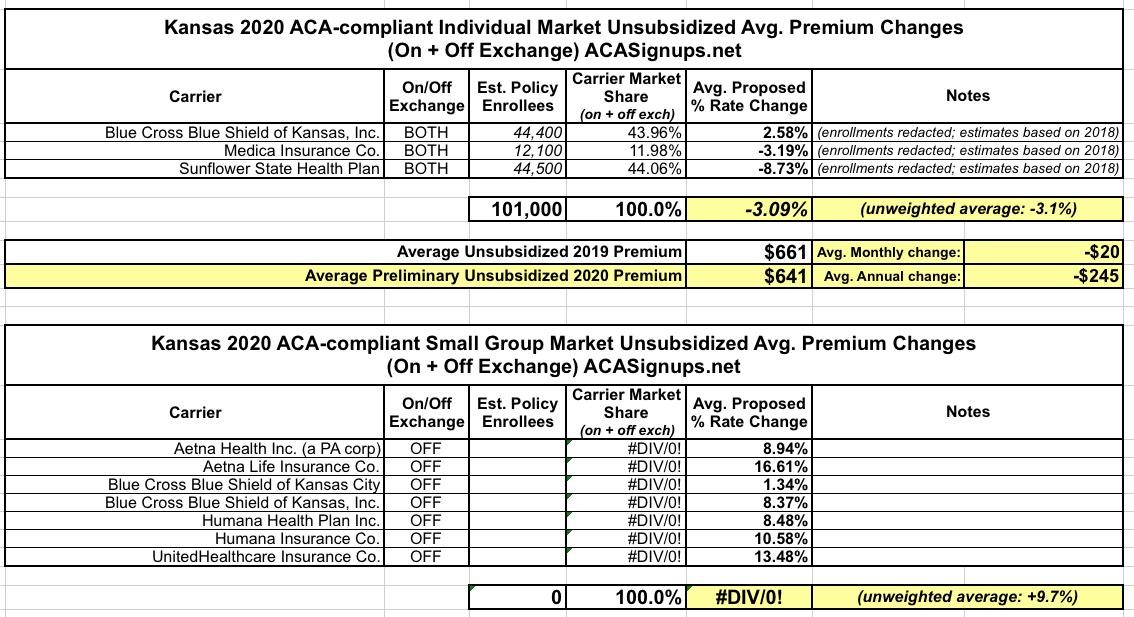

(sigh) Kansas is yet another state where the enrollment data for each of the carriers is redacted on the filing forms this year. To run the weighted average, I'm using last year's estimated enrollment numbers for each, which may have shifted around this year.

Assuming things haven't shfited around too much, unsubsidized Kansans will likely be looking at roughly a 3.1% average premium reduction in 2020...which also happens to be the same as the unweighted average change.

Meanwhile, the small group market is looking at an unweighted average increase of 9.7% statewide.

(sigh) As is common this year, the rate filings for Iowa's Individual and Small Group market are heavily redacted, making it impossible to calculate a weighted average premium rate change. On the Indy market, Medica is reducing their unsubsidized 2020 premiums by 11.3%, while Wellmark is raising theirs by around 4.8%.

Seeing how Wellmark only re-entered the ACA-compliant individual market this year, I'm assuming Medica has the lion's share of enrollees...but who knows? Also, Wellmark is offering two different types of policies; I'm assuming that at most the two combine to be similar to Medica's total. If so, that should mean an average premium reduction of around 3.3%.

For the small group market, I just ran an unweighted average of the 12 different companies offering policies, coming up woth an average 5.4% increase.

There is one interesting tidbit in the Wellmark filing, however: They expect 100% of their 2020 enrollees to do so on-exchange, which basically means that their unsubsidized premiums have gone up so much that they don't expect anyone to be willing to pay full price (off-exchange) for them.

Hawaii only has two carriers participating in the Individual health insurance market. For 2020, they're reducing unsubsidized premiums slightly.

The state's small group market has four carriers; unfortunately, only one of the four (Kaiser Foundation Health Plan) has posted their enrollment data; the other three are redacted. The unweighted average increase on the small group market is a mere 0.8%, however.