I wasn't expecting my analysis of Rhode Island's 2020 ACA premium changes to be of any particular interest; it's a small state with only two carriers offering individual market policies, after all, so there's not usually much to it.

A week or so ago I reported that Covered California had released their preliminary 2020 ACA individual market premium rate changes, with a record-low 0.8% average increase statewide. They detailed in the report how the combination of reinstating the ACA's individual mandate penalty and using that funding to provide additional financial subsidies to the enrollees lowered the average rate increases from 4.0% to 0.8%, saving unsubsidized enrollees around 3.2 points or $167/year on average.

Today, CoveredCA has posted more details about some of the specifics:

Covered California Releases Regional Data Behind Record-Low 0.8 Percent Rate Change for the Individual Market in 2020

I've gotten a lot of praise over the years for my "Psychedelic Donut®" depiction of the total healthcare coverage landscape nationally.

For comparison, here's a similar state-level pie chart from the Vermont Agency of Human Services. It doesn't start out too bad, breaking out the total statewide coverage along the lines of the Donut. As you'd expect, around half the state's 627,000 residents are covered via private insurance (45% via their employer, 5% via the ACA individual market, 1% via "Association Health Plans"), while the other half is mostly covered via Medicare or Medicaid. Vermont has only a 3% uninsured rate.

Back in March, I noted that a federal judge had shot down the Trump Administration's attempt to expand so-called "Association Health Plans", which are quasi-ACA compliant but which also have a long, ugly history of fraud and other abuses:

There is a long history of shady and inept operators of association health plans and related multiple employer welfare arrangements, with dozens of civil and criminal enforcement actions at the state and federal levels. The U.S. Government Accountability Office identified 144 "unauthorized or bogus" plans from 2000 to 2002, covering at least 15,000 employers and more than 200,000 policyholders, leaving $252 million in unpaid medical claims. Some were run as pyramid schemes, while others charged too little for premiums and became insolvent.

...Powerful words from DC District Court Judge John Bates in holding a Trump DOL rule unlawful: "The Final Rule was intended and designed to end run the requirements of the ACA, but it does so only by ignoring the language and purpose of both ERISA and the ACA."

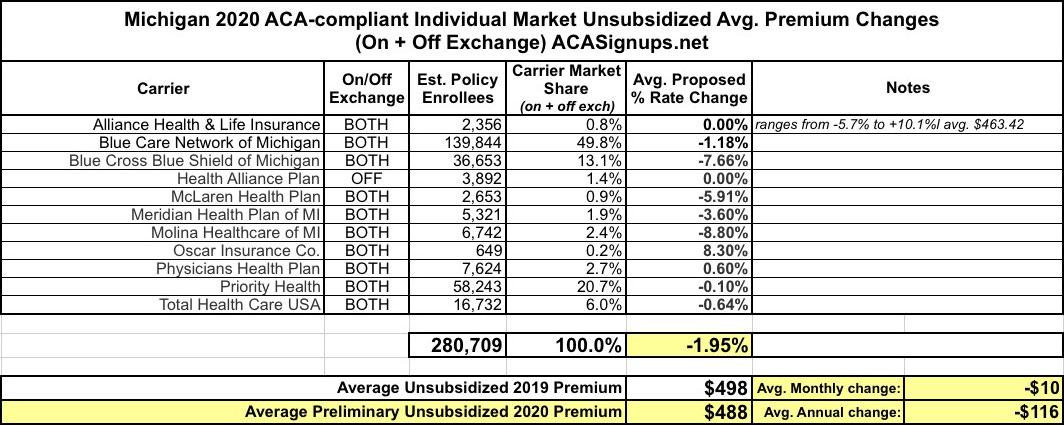

At the time, I concluded that the weighted average change marketwide was a 1.95% reduction in premiums compared to 2019, for around 281,000 Michiganders on the Indy market. This would mean roughly a $10 average premium reduction per unsubsidized enrollee per month, or $116 per year:

Polis Administration Projects 18.2% Average Decrease in Premiums for Individual Health Insurance Plans in 2020

Reducing health care costs has been a top priority for Polis.

DENVER (July 16, 2019) – Today, the Colorado Division of Insurance (DOI), part of the Department of Regulatory Agencies (DORA), announced that for the first time ever, Colorado health insurance companies that sell individual plans (for people who do not get their health insurance from an employer or government program) expect to reduce premiums by an average of 18.2 percent (-18.2%) over their 2019 premiums, provided the reinsurance program is approved by the federal government. These are the health insurance plans available on the Connect for Health Insurance Exchange, the state’s health exchange made possible by the Affordable Care Act (ACA).

If I could only ask one question of the 20-odd candidates vying for the Democratic nomination for President at the next debate coming up right here in Detroit, Michigan, here's how I would word it. I've customized it for each of the five major candidates (apologies to the rest of them):

Preface to each of the candidates:

"Earlier this month, oral arguments were heard by the 5th Circuit Court of Appeals over a lawsuit against the Affordable Care Act filed by 20 Republican Attorneys General and fully supported by the Trump Administration.

"If the plaintiffs are successful and the ACA is struck down entirely, up to 20 million Americans would find themselves without healthcare coverage and tens of millions more with pre-existing conditions would lose critical protections, while states would lose hundreds of millions, or even billions of federal funding.

"Every Democratic candidate has come out in favor of significantly expanding publicly-funded healthcare coverage to some degree or another. Some want to build upon the Affordable Care Act. Some want to add a public option. Some want guaranteed universal coverage, and some are demanding universal single payer healthcare for everyone in the United States.

I promised to have a writeup about Joe Biden's just-rolled-out healthcare proposal yesterday, but I ended up stuck at the Apple Store for nearly six hours (don't ask).

On March 23, 2010, President Obama signed the Affordable Care Act into law, with Vice President Biden standing by his side, and made history. It was a victory 100 years in the making. It was the conclusion of a tough fight that required taking on Republicans, special interests, and the status quo to do what’s right. But the Obama-Biden Administration got it done.

Yes, I'm back from Netroots Nation 2019, and yes, I know that Joe Biden just rolled out his official healthcare policy proposal for the 2020 Presidential election.

I still have to read his plan through and will write up my thoughts about it later today, but before that, I have to take care of this:

A new set of proposals provide some of the strongest evidence yet that Obamacare -- once on the verge of collapse in Tennessee -- has stabilized.

The state’s largest insurance company, BlueCross BlueShield of Tennessee, plans to reenter the Affordable Care Act marketplace in Nashville, Memphis and surrounding counties next year, providing another option for residents on Obamacare. Additionally, two other insurance companies that already offer Obamacare in these cities, Cigna and Oscar Health, are planning to significantly reduce the cost of their coverage plans.

Although the proposals are not final, it appears Tennesseans will have more options and competitive prices in the coming year, said Kevin Walters, a spokesman for the Department of Commerce and Insurance.