Jibbers Crabst on a stick. Any time University of Michigan Law Professor Nicholas Bagley begins his Twitter threads with a screenshot of legalese, it's bad news.

First, here's his full thread:

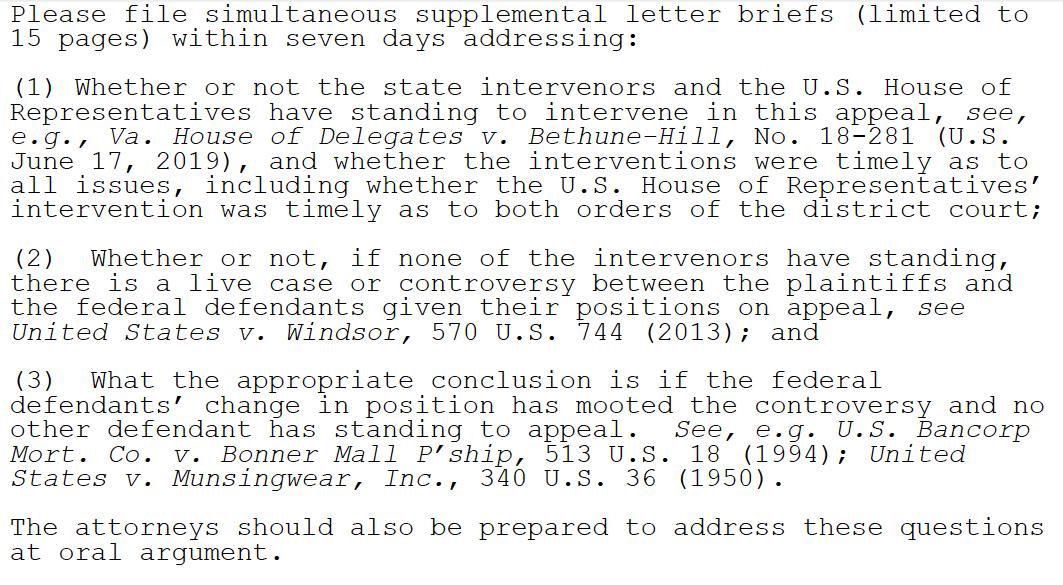

The panel in the Fifth Circuit that's about to hear Texas v. United States has just asked for further briefing on standing -- and in particular on whether the intervenor states and the House of Representatives can properly appeal the case.

I know I rip on Republicans a lot here at ACASignups.net, and I stand by pretty much all of it. Once in a while, however, a GOP member of Congress does do (or tries to do) something useful when it comes to healthcare policy...and the name most often attached to that is Senator Lamar Alexander of Tennessee. Alexander happens to be retiring, I should note. These two facts may or may not be connected, but I digress.

In any event, Sen. Alexander and Democratic Senator Patty Murray of Washington State have been working together for quite some time now on several healthcare bills to help stabilize the ACA, reduce drug prices and so forth, to varying degrees of success. I may not have agreed with most of Alexander's ideas, but he seems to be genuinely interested in improving the situation...and of course I can't say enough good things about Sen. Murray.

Regular readers may have noticed that I didn't post a single blog entry on Tuesday even though there's been a ton of healthcare policy stuff going on. No, I didn't take the day off; I started poring over a spreadsheet at around 10am and was working on it almost nonstop all day.

Big news: SCOTUS is taking up the ACA risk corridors case. GOP's decision to stymie that program arguably did the most damage to the ACA marketplaces. https://t.co/VeMRcd5MYn

When the ACA was first developed and voted on, lawmakers knew that the disruption to the individual health insurance market was going to be pretty rocky for the first few years, so they put three types of market stabilization programs into place. They were known as the "Three 'R's"...Risk Adjustment, Reinsurance and Risk Corridors:

...Risk adjustment interrupts these cycles by doing exactly what its name implies. It adjusts for differences in the health of plans’ enrollees by redistributing funds from companies with healthier-than-average customers to plans with sicker-than-average customers. Such transfers could occur within or across health plan tiers in the exchanges (bronze, silver, gold, platinum). All the redistributed monies come from insurance companies in the marketplaces. No taxpayer bailout here.

I'm neither an attorney nor a Constitutional expert, so this may not have any legal significance beyond confirming what everyone already knew about the Trump Administration. Then again, perhaps it will.

Several studies, including this one from just the other day, have driven home this point clearly: Adding work requirements to Medicaid expansion enrollees serves no useful purpose other than to kick tens of thousands of people off of their healthcare coverage (which, of course, is the whole point from the POV of those who add the requirements).

As for the one positive-sounding goal (increasing employment) which supporters always use to try and justify them, that's a complete joke:

The first major study on the nation’s first Medicaid work requirements finds that people fell off of the Medicaid rolls but didn’t seem to find more work.

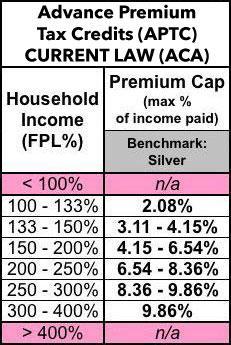

As I've noted several times, one of the biggest flaws in the Affordable Care Act is a very simple one on paper: The Subsidy Cliff. People who enroll in ACA exchange policies are entitled to financial assistance on a sliding scale...but only if their household incomes fall between 100-400% of the Federal Povery Level. Those below the lower threshold (actually, below 138% FPL) are expected to enroll in Medicaid, but those over the upper threshold of 400% FPL (around $50,000/year for a single person, roughly $103,000/year for a family of four) are completely on their own.

Here's the current federal premium subsidy formula (the precise premium cap percentages change slightly from year to year...and the Trump Administration is even messing with that a bit, so I'm not sure what it'll be in 2020):

In other words, only about 10% (at most) of those still in the Medicaid Gap could even remotely match the GOP's cliche of a "lazy, good-for-nothing layabout" type who's able-bodied, has no serious extenuating circumstances and so forth. The "get off your ass and work!" requirements appear to be nearly as big a waste of time and resources as the infamous "drug testing for welfare recipients" bandwagon which a bunch of states jumped on board over the past few years.

One Ohio resident paid $240 a month for health insurance that she later learned didn’t cover her knee replacement. Saddled with $48,000 in medical bills, she decided not to get the other knee replaced.

...A Kansas resident paid premiums on a policy for two years, then found out his insurance would not cover surgery for a newly diagnosed cancer.

The two policyholders have filed a lawsuit in federal court against Health Insurance Innovations, based in Tampa, Fla., accusing the company of misleading them about the kind of policy they were buying.

They say they believed they were purchasing Affordable Care Act plans that include coverage guarantees. But they were sold much less comprehensive coverage that left them vulnerable to tens of thousands of dollars in unpaid medical bills, according to the lawsuit.

The state of Maine's Bureau of Professional & Financial Regulation has released their preliminary 2020 rate filings for the Individual and Small Group markets. Overall, the three carriers participating in their individual market are seeking a weighted average rate increase of 4.7% vs. last year. If approved as is, that would bring the average unsubsidized premium up from $675/month to $707/month, or around $381/year.

It's important to keep in mind why premiums are going up. I've included screenshots of the rate filing memos--Maine Community Health Options, which holds over 50% of the individual marketshare, clarifies that the combination of the individual mandate being repealed and the expansion of #ShortAssPlans are causing an 11% increase. They also note that Maine's recent Medicaid expansion implementation may be a factor, although normally that reduces premiums since lower-income populations tend to be less healthy than higher-income populations, so I'm not sure what to make of that.