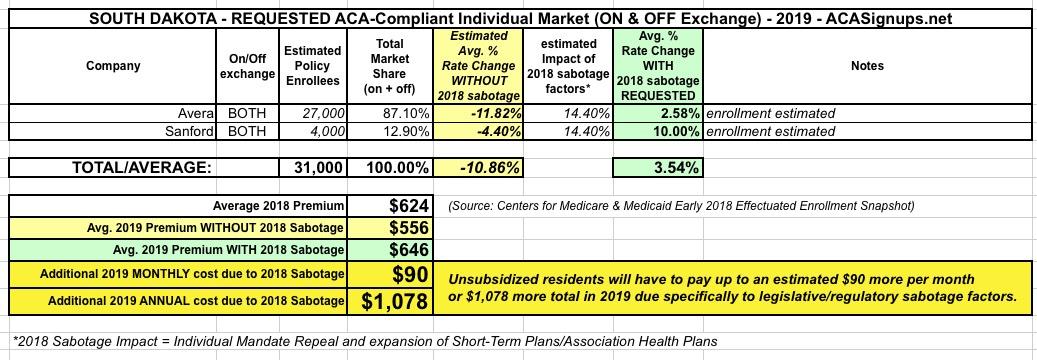

South Dakota has two ACA indy market carriers, Avera and Sanford. The relative enrollment market shares are based on last year's numbers. The 14.4% #ACASabotage impact assumes 2/3 of the Urban Institute's projections to err on the side of caution.

THe average unsubsidized SD indy market enrollee pays $624/month this year; instead of that dropping by around $68/month, it's expected to increase by $22...for a total monthly difference of $90.

Assuming that's accurate, this means unsubsidized SD residents will be paying over $1,000 more apiece next year than they'd otherwise have to.

The only confusing thing about South Carolina's 2019 rate filings is that I'm not sure whether the "BlueChoice Health Plan" should be rolled in with the main Blue Cross Blue Shield of SC population. Carriers often have multiple listings in the same state for different policy lines, but they're generally listed under the same official corporate name. In this case, "BlueChoice" (which is clearly still part of BCBS) has a completely seaparate listing.

The BCBS filing clearly states the number of enrollees as around 203,000 people. The BlueChoice listing doesn't give a membership number, but appears to be roughly 6,800 people based on the full premium dollars they received in all of 2017 ($53.5 million divided by 12 months, divided by the statewide average of $654/month this year). This doesn't really make much difference, however, since BCBS still holds nearly 99% of the market anyway.

Assuming an 11.5% #ACASabotage factor (mandate repeal + shortassplans), this translates into unsubsidized enrollees having to pay an extra $900 than they'd otherwise have to (a 9.2% rate increase instead of a 2.3% rate drop).

Oklahoma is pretty clear cut: BCBSOK holds nearly all of the ACA-compliant market share, with CommunityCare HMO having a small number of off-exchange enrollees (the numbers are estimates based on last year's figures).

The Urban Institute projected an 18.4% rate increase due to #MandateRepeal and #ShortAssPlans. BCBSOK doesn't go into specifics about the impact, but does list both of these as significant factors. Knocking 1/3 off this projection gives around 12.4%.

Unsubsidized Oklahoma enrollees are paying an average of $694/month in 2018. Without ACA sabotage, they'd likely see this drop to around $595; instead, they're likely looking at paying roughly $681/month, or an additional $1,033 apiece.

In direct response to this, Medica Health Plans dropped out of the ND on-exchange individual market this year to avoid taking the CSR hit. They hung around the off-exchange market, however, and therefore still have about 600 enrollees in the state.

New Hampshire is perhaps the most striking example of both insurance carriers significantly overshooting the mark for 2018 premiums while also proving my point that just because premiums are dropping next year, #ACASabotage is still causing unsubsidized enrollees to pay a lot more than they'd have to otherwise.

All three of the carriers offering ACA policies on New Hampshire's individual market are reducing their 2019 premiums, by anywhere from 7.4% for Harvard Pilgrim to a whopping 15.2% in the case of Ambetter/Celtic.

THe enrollee market share numbers come from the monthly report from the New Hampshire insurance department (I'd love it if every state required one of these...it includes both on and off-exchange enrollees). The "PAP" column refers to NH residents enrolled in their "private option" Medicaid expansion program...but those are still part of the same risk pool as the other enrollees, so they still have to be factored into the market share formula.

Nebraska is about as simple as it gets--there's only one carrier offering ACA individual market plans. Unfortunately, they've redacted the combined average rate change request between their two plan entries, so all I can do is split the difference and assume around a 1% average increase.

The Urban Institute projected that Nebraska rates would see a whopping 20.4 percentage point increase due to #MandateRepeal and #ShortAssPlans, which are both referenced in Medica's filing. Since they don't get more specific than that, I'm assuming 2/3 of Urban's estimate, or a 13.6% increase.

Unsubsidized Nebraska enrollees are currently paying an average of $854/month, so if accurate, that's a difference of around $116/month or nearly $1,400 for the year. Ouch.

Mississippi is pretty easy: Only two carriers. I have no idea what their relative market share is (the enrollment data along with a lot of other stuff is redacted in their filings), but in this case it really doesn't matter because both of the carriers are requesting nearly identical rate changes anyway...which is to say, just about no change whatsoever.

The Urban Institute projected that #MandateRepeal and #ShortAssPlans would add a 17.2 percentage point rate hike factor in Mississippi. I generally knock 1/3 off of their estimates to err on the side of caution (11.4%), but given Ambetter specifically stating that they didn't add any increase to account for #ShortAssPlans (why?? interesting!), I'm shaving off a bit more and assuming a flat 10% impact.

This means that unsubsidized Mississippi enrollees would likely have saved a good $800 apiece next year without Trump/GOP efforts to undermine the ACA this year.

NOTE: The good news is that I don't have to worry about any sabotage impact for Massachusetts in 2019 (thanks to the state still having their pre-ACA individual mandate penalty in place and banning #ShortAssPlans outright). This obviously makes that part of my analysis very easy--I can just enter "0%" across the board in the "2018 sabotage factor" columns.

The bad news is that determining the market share for each carrier in Massachusetts is a royal pain in the ass. only two of the twelve carriers offering individual market plans actually state what their enrollment numbers are, and this is further confused by the fact that several of them (Fallon, Harvard Pilgrim and Tufts) have two or three different listings for different divisions of the company.

In addition, Massachusetts is one of just two states where the individual and small group market risk pools are merged, making it even more difficult to separate out the two for market share purposes.

Kansas is pretty frustrating. There's only three carriers offering ACA individual market policies, but two of the three have heavily redacted actuarial memos, so I don't know what their market share is...and the same two were new (or "semi-new") to the exchange this year so I can't even use last year's effectuated enrollment as a guideline. In light of that, I had to split the estimate right down the middle to get an estimated overall market share.

In addition, Medica is the only one of the three to specifally mention mandate repeal and/or #ShortAssPlans as a contributing factor; that's also redacted in the filings for the other two. Therefore, instead of assuming 2/3 of the Urban Institute's sabotage projection, I'm being extra-cautious and assuming just half (9.6% instead of 19.2%). This gives a rough statewide average increase of around 6.1%, which would likely be closer to a 3.5% premium reduction without mandate repeal and short-term plan expansion.

Illinois has the same four ACA indy market carriers participating next year as they do this year. All four rate filings specificlaly call out Mandate Repeal and #ShortAssPlans as significant factors in their rate requests, but none of them break out the actual amount, so I'm relying on my standard assumption of 2/3 of the Urban Institute's projections.

In Illinois' case, that's 2/3 of 19.4%, or around a 12.9% #ACASabotage premium increase for unsubsidized enrollees.

I should also note that only one of the four carriers (Health Alliance) specifies just how many enrollees they have; for the other three I'm basing my estimates on last year's numbers for now. The two carriers with what I assume are still the largest market share (BCBS and Celtic) are basically keeping rates flat year over year, while the other two are 7.5% and 10% apiece, for an average rate increase of just 0.7% statewide.

Unsubsidized Illinois residents are currently paying $644/month on average, so a 12.9% sabotage effect means that each of them will have to pay nearly $1,000 extra next year. Ouch.