The total individual/family policy health insurance market was roughly 10.6 million people in 2013. This included people enrolled in either "grandfathered" policies (i.e., policies enrolled in prior to the ACA being signed into law in 2010) or in "transitional" policies (those enrolled in between 2010 and late 2013, just before the ACA required all new individual market policies to be fully compliant with the new healthcare law.

How many of those 10.6 million people are still enrolled in grandfathered (GR) or transitional (TR) policies today? Unfortunately, there seems to be very little available data about just how many people are still in these policies. The Kaiser Family Foundation gave a rough estimate of around 2.1 million people last year, which sounded about right to me. However...Kaiser didn't include a state-level breakout of their estimates, and of course it's a year later so that number, if accurate, has probably shrunk a bit more.

Last month I noted that while Congressional Republicans spent all of 2017 desperately attempting to "blow up" the Affordable Care Act via a combination of legislation, the Trump Administration simultaneously tried to tear down the law via various regulatory sabotage efforts. This year the GOP Congress appears to have mostly given up on their mischief (they did manage to partially wound the ACA by repealing the individual mandate), the Trump Administration is doubling down on regulatory sabotage, laying what I've termed "Regulatory Siege" to the law.

In my mind, "phase one" included the non-legislative stuff Trump did last year, including stuff like cutting off CSR reimbursements, slashing the Open Enrollment Period in half, slashing marketing funding by 90%, slashing the outreach budget by 40% and so on. "Phase two" includes the previously-announced #ShortAssPlans executive order, CMS allowing work requirements for Medicaid and so forth (individual mandate repeal belongs here as well, although that was legislative, not regulatory...although there's overlap as you'll see below).

The total individual/family policy health insurance market was roughly 10.6 million people in 2013. This included people enrolled in either "grandfathered" policies (i.e., policies enrolled in prior to the ACA being signed into law in 2010) or in "transitional" policies (those enrolled in between 2010 and late 2013, just before the ACA required all new individual market policies to be fully compliant with the new healthcare law.

How many of those 10.6 million people are still enrolled in grandfathered (GR) or transitional (TR) policies today? Unfortunately, there seems to be very little available data about just how many people are still in these policies.

Health Insurance Subsidies and Related Spending.Outlays for health insurance subsidies and related spending are estimated to increase by $10 billion, or 21 percent, in 2018.8 That jump mostly stems from an average increase of 34 percent in premiums for the second-lowest-cost “silver” plan in health insurance marketplaces established under the Affordable Care Act. (Those premiums are the benchmark for determining subsidies for plans obtained through the marketplaces.) Over the 2019–2028 period, the average growth in spending is projected to lessen considerably, to just under 5 percent per year, as per-beneficiary spending rises with the costs of providing medical care. CBO estimates that, under current law, outlays for health insurance subsidies and related spending would rise by about 60 percent over the projection period, increasing from $58 billion in 2018 to $91 billion by 2028.

Yup, thanks to deliberate sabotage from the first two years of the Trump Administration, premiums have spiked by ~30% this year and will do so again next year, requiring federal spending on subsidies to increase accordingly.

Positive Blue Cross results trigger rebates to consumers

It is legally required to return about $30 million of its 2017 profit to subscribers.

After three years of losses in the state’s market where individuals buy health insurance, Blue Cross and Blue Shield of Minnesota made so much money last year that it has to give some back.

The Eagan-based carrier, which is the state’s largest nonprofit health plan, disclosed last week that it expects to provide $30 million in consumer rebates as required by rules in the federal Affordable Care Act (ACA).

Analysts said that Blue Cross likely isn’t alone in having overshot with rates last year, since insurers across the country have been struggling to figure out how much premium revenue they need to cover the cost of medical bills in the individual market.

In Minnesota, rebates driven by big margins are a surprising cap to a year that started with fears that mounting losses would cause a market collapse.

Maryland Governor Larry Hogan signed a bipartisan bill on Thursday that state officials say will help keep healthcare premiums from spiking again next year.

The bill creates what’s known as a reinsurance program for the state’s health insurance marketplace, which was created as part of the Affordable Care Act.

...Without the fix or any action in Washington, Maryland officials predicted that healthcare premiums in 2019 could jump up to 50 percent, driving more of the 150,000 people to abandon the state’s marketplace — possibly leading to its collapse.

As you may have noticed, I'm on a bit of a grandfathered/transitional plan data kick this week (there's a reason for it which you'll understand next week). These numbers are tricky to hunt down, since they aren't tracked by the ACA exchanges. Most states either don't track them at all or don't make it easy for the public to locate, and it's even treated as a proprietary trade secret in a few states.

The Kaiser Family Foundation gave a rough estimate of around 2.1 million people still being enrolled in GF/TR plans last year, but they never broke it out by state. Plus, of course, that was last summer; since no one can newly enter these types of policies, their numbers continue to gradually shrink year after year.

OK, I'm just seeing this now so I could be seriously misreading the article, but if I'm not, this is quite the eye-opener:

Virginia is on the cusp of expanding Medicaid to 400,000 low-income residents, after a veteran Republican state senator said Friday that he is willing to split with his party and help Democrats realize a goal they have been chasing for years.

Virginia state Sen. Frank Wagner (Virginia Beach) said he supports allowing more poor people to enroll in the federal-state healthcare program on two conditions.

He wants the plan structured so that Medicaid recipients do not suddenly lose coverage if their earnings rise. And he wants a tax credit or some other help for middle-income people who already have insurance but are struggling to pay soaring premiums and co-pays.

Earlier today I wrote an extensive post about California's individual market, specifically breaking out the number of off-exchange policies, including a rare look at some hard grandfathered plan enrollment numbers.

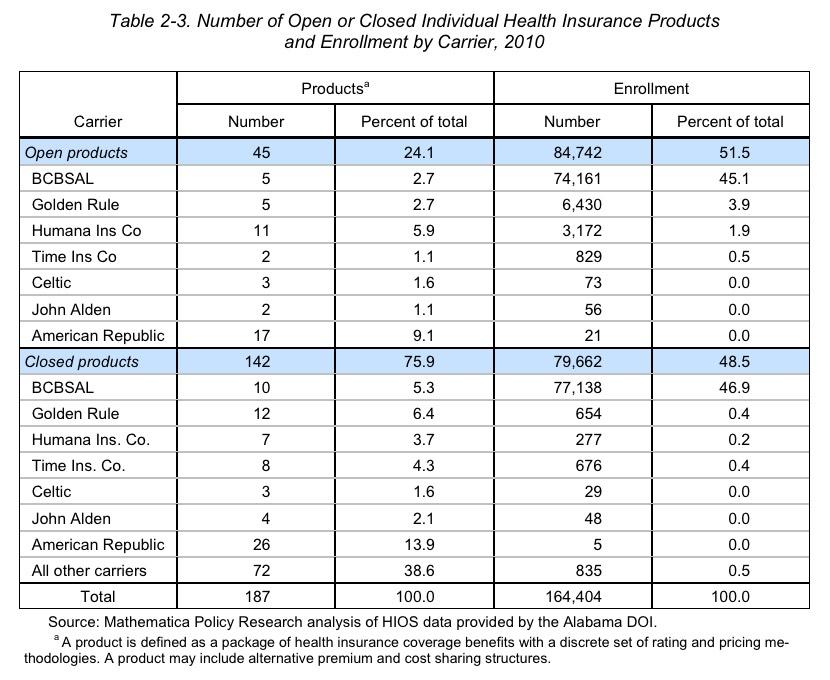

I've also managed to dig up a fascinating document from 2010 buried on the Alabama Insurance Department's website, which provides quite a bit of demographic insight into Alabama'soverall health insurance market. While all of this info is now 8 years out of date (and even precedes the first ACA open enrollment period), it does provide a few clues into estimating what's going on in Alabama today.

This first table shows exactly what Alabama's individual market looked like: 164,404 people were enrolled in pre-ACA "major medical" policies in 2010:

The California Health Care Foundation is a nonprofit philanthropic organization. From their About page:

The California Health Care Foundation is dedicated to advancing meaningful, measurable improvements in the way the health care delivery system provides care to the people of California, particularly those with low incomes and those whose needs are not well served by the status quo. We work to ensure that people have access to the care they need, when they need it, at a price they can afford.