When Maryland insurance carriers originally submitted their proposed 2019 premium changes back in May, it looked pretty grim...they were expected to average around 29.5% statewide for the ACA-compliant individual market., increasing from around $631/month on average to roughly $817/month for unsubsidized enrollees.

Thanks to swift, bipartisan action on the part of the Democratically-controlled Maryland state legislature and the Republican Governor, Maryland was able to pass several bills which partially negated or cancelled out Trump/Congressional Republican sabotage of the Affordable Care Act. In particular, they passed laws which locked in current restrictions on both short-term plans and association health plans (the types of "junk policies" which Trump is pushing hard to expand upon)...along with an extremely robust reinsurance program.

Just in case anyone thinks state insurance regulatory boards can't be hard-core badasses, consider the Optima Health situation in Virginia which I wrote about a couple of weeks ago:

By early September, it was clear that Trump would indeed be cutting off CSR funding. With just a few weeks left before the final deadline to sign 2018 ACA exchange contracts, Optima suddenly announced that they were not only jacking up rates a whopping 81%, they were also pulling out of a large chunk of the state, leaving large areas at risk of "going bare" without any ACA carriers whatsoever.

...Then, on September 14, with just days to spare and thanks to what I assume were some pretty intense backroom deals being made, Anthem suddenly announced that they were back in the game after all!

Ready for Open Enrollment, Health Connector sets 2019 plans with lower premium increases, selects community organizations to provide in-person support to residents

Boston – September 13, 2018 – The Massachusetts Health Connector Board of Directors today approved 57 Qualified Health Plans from nine carriers for individuals and families, with new plan designs that create better value for members and premium increases that average under 5 percent from 2018.

Unfortunately, the press release doesn't specify what "under 5%" means, nor does it break that out by carrier/market share. I've put in a request for those details and will update this as soon as I hear back from them. They sent me the following chart, but this only includes enrollees earning between 300-400% of the Federal Poverty Level, which means the marketshare across the entire individual market is likely somewhat different. I'm assuming the 4.4% overall average applies to the entire market but could be wrong about that as well:

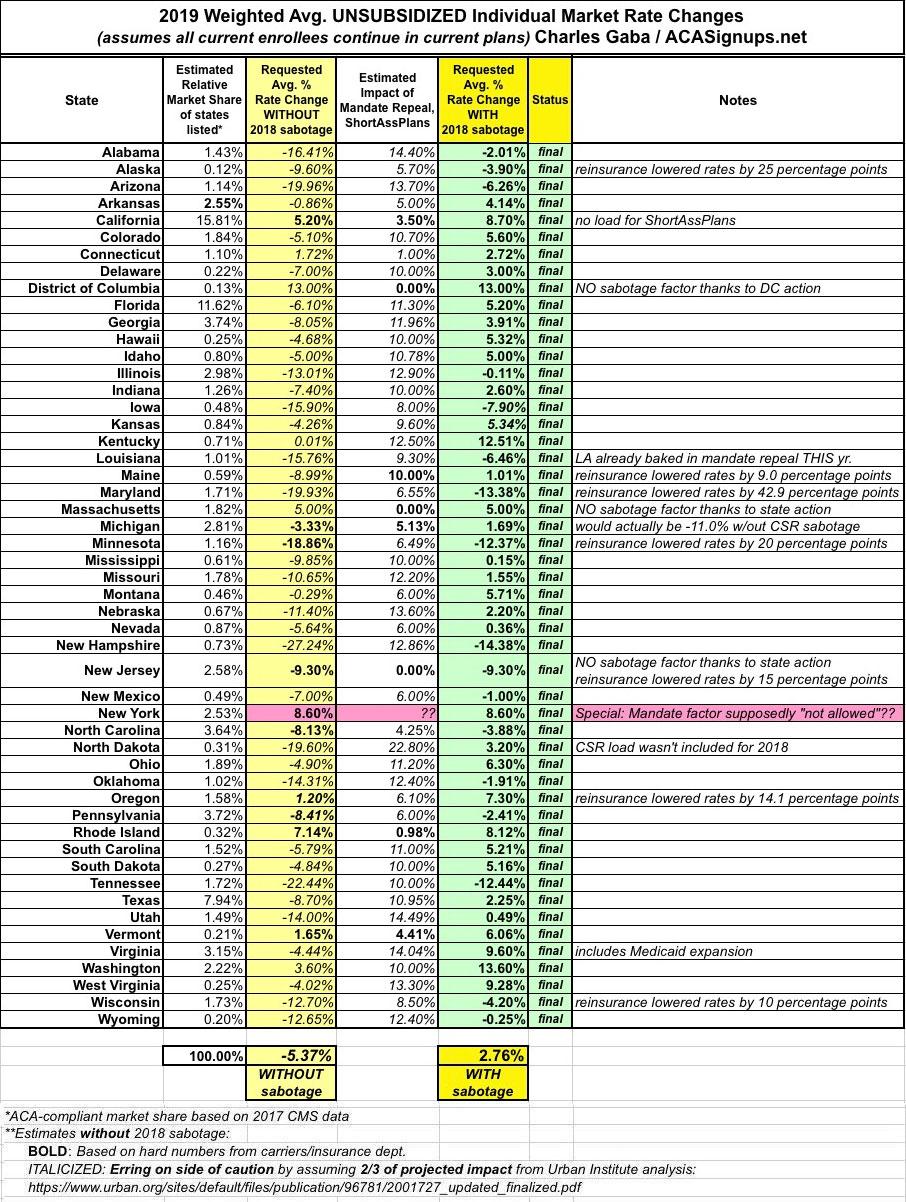

For months now, I've been trying to get people to understand that when it comes to sabotage of the Affordable Care Act, especially in terms of individual market premium increases, you have to include the impact of actions taken by Donald Trump and Congressional Republicans in BOTH 2017 and 2018, not just 2018 alone.

In 2017, the single largest factor in the ~28% average national unsubsidized premium increase for ACA plans was Donald Trump's cutting off of Cost Sharing Reduction (CSR) reimbursement payments to carriers. This alone accounted for fully half of the 2018 increase. However, there were other, smaller actions taken which added up to another 3% or so: Slashing the Open Enrollment Period in half, CMS slashing the marketing budget for the federal exchange down 90%, slashing the outreach/navigator budget down 40% and so on.

Iowa has only a single insurance carrier offering ACA-compliant individual market policies this year. Next year they'll have two, as Wellmark has decided to Hokey Pokey their way back onto the exchange again in 2019...but since they weren't around this year, there's no current policy premiums to measure any increase (or decrease) against.

Medica, the sole carrier now selling individual health insurance policies in Iowa, plans to raise its 2019 premiums by less than a tenth as much as it did for 2018.

Medica raised its Iowa health insurance premiums by a staggering average of 57 percent for 2018. It was the steepest such health insurance increase in Iowa history. Company leaders said last summer they needed the higher premiums to stay in the market. But this time around, the Minnesota-based carrier is planning to raise Iowa premiums by an average of less than 5.6 percent, state regulators disclosed Wednesday.

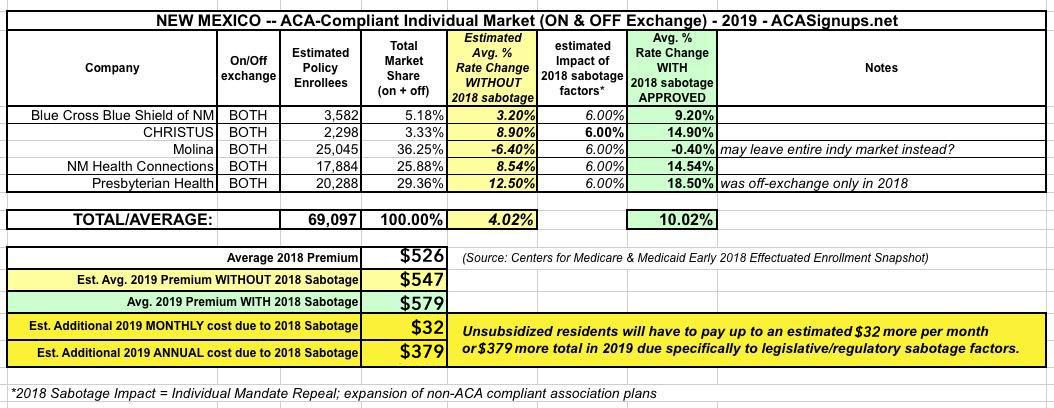

New Mexico was one of the earlier states to post their initial, requested 2019 ACA individual market premium hikes back in June. At the time, the five carriers asked for rate increases ranging from a slight drop (-0.4% for Molina) to as high as an 18.5% increase for Presbyterian Health, which is currently only offering off-exchange policies this year. Based on their preliminary filings, New Mexico was looking at a weighted average increase of around 10.0% next year, which would have been more like 4% if not for this years sabotage efforts by Trump and the GOP (mandate repeal & expansion of #ShortAssPlans):

A few weeks ago, I posted about New Jersey's preliminary 2019 ACA-compliant individual market rate filings. At the time, the official New Jersey Dept. of Banking & Insurance specifically stated that:

AP Exclusive: Modest premium hikes as 'Obamacare' stabilizes

Millions of people covered under the Affordable Care Act will see only modest premium increases next year, and some will get price cuts. That's the conclusion from an exclusive analysis of the besieged but resilient program, which still sparks deep divisions heading into this year's midterm elections.

The Associated Press and the consulting firm Avalere Health crunched available state data and found that "Obamacare's" health insurance marketplaces seem to be stabilizing after two years of sharp premium hikes. And the exodus of insurers from the program has halted, even reversed somewhat, with more consumer choices for 2019.

{kind=link}