With the 2019 Open Enrollment Period quickly approaching, I'm spending a lot of time swapping out the requested carrier rate changes from earlier this summer with the approved rate changes from state regulators.

Hawaii only has two carriers participating in the ACA-compliant individual market: HMSA and Kaiser, which requested rate increases of 2.72% and 28.6% respectively back in August. With a roughly 57/42 market share split, this resulted in a weighted average rate increase of 13.8%, which would likely have been closer to 3.8% if the ACA's individual mandate penalty hadn't been repealed.

With just 3 weeks to go before the 2019 Open Enrollment Period begins, the dust has mostly settled on my 2019 Rate Hike Project. Over half the states have provided their final, approved individual market premium changes, and while I haven't found the final rates for the other half yet, their preliminary rates are all on record, so I don't anticipate the needle moving too much at this point.

New Hampshire is among the states which I haven't found final rate changes for yet. The three carriers in the state have requested average price reductions of around 13.5% on average, which is well below the 3.2% increase which is the average nationally, but I still don't know what the state regulators are going to approve.

This makes the following press release rather surprising:

NH Insurance Department to Hold Oct. 30 Annual Public Hearing on Health Insurance Premiums

U.S. SENATOR TAMMY BALDWIN AIMS TO BLOCK PRESIDENT TRUMP’S PLAN TO ALLOW INSURERS TO SELL JUNK PLANS WITH LEGISLATION TO GUARANTEE PROTECTIONS FOR PRE-EXISTING CONDITIONS

“The Fair Care Act is an opportunity for lawmakers to keep their word on guaranteed protections for pre-existing conditions.”

WASHINGTON, D.C. – Following the Trump Administration’s recent proposed rule allowing insurance companies to once again sell ‘junk’ health care plans, U.S. Senator Tammy Baldwin today announced new legislation to block the rule and guarantee protections for people with pre-existing conditions.

*(OK, that's hyperbole...unsubsidized enrollees are still left holding the bag for thousands of dollars in unnecessary premium payments for at least another year or so, and there's still no guarantee of the final ruling...see below...)

Almost exactly a year ago, Donald Trump, after 9 months of bluster about doing so so, finally pulled the trigger on his threat to cut off Cost Sharing Reduction reimbursement payments to insurance carriers for the deductibles, co-pays and other out-of-pocket expenses which they agree to cover every month for around 7 million low-income ACA exchange policy enrollees.

Trumps stated goal in doing so was, of course, to "blow up" the ACA, to cause it to "implode" (which is actually the opposite of blowing something up, but that's a different discussion) and ultimately fail in the process.

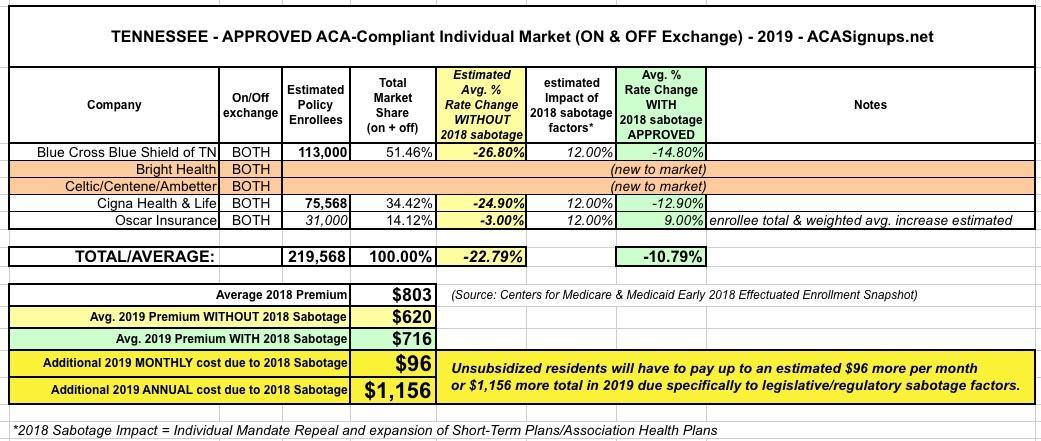

When I last posted about 2019 ACA-compliant individual market premium changes in Tennessee back in August, I noted that premiums statewide had gone from dropping 5.7% to dropping 10.8% on average after the Trump Administration first stated that they were going to unnecessarily "freeze" the ACA's Risk Adjustment fund transfers in response to a lawsuit ruling only to reverse themselves a week or so later and state that they were going to go ahead and process RA fund transfers after all.

In other words, the Trump Administration once again deliberately caused a panic across the industry only to "save" the industry from the very threat which they had posed in the first place.

In any event, here's what I thought the Tennessee's premium situation looked like when the dust settled:

Back in August, Blue Cross Blue Shield of South Carolina, the only carrier offering policies on SC's individual insurance market, asked for a 9.2% average premium rate increase for 2019 statewide. This consisted of 9.3% for their most popular plans (which cover over 200,000 South Carolinans) and 6.9% for 6,800 BlueChoice plan enrollees (BlueChoice is only available off-exchange).

2019 PRELIMINARY HEALTH INSURANCE PLANS RATE CHANGES FOR INDIVIDUAL MARKET COVERAGE

The SCDOI has approved the rates and forms for health insurance issuers that are planning to offer ACAcompliant products in the individual market in 2019.

Most Connect for Health Colorado® Customers Will See Decrease in Premiums for 2019 as Marketplace Stabilizes

DENVER — With rate increases lower than the state has seen in years, Connect for Health Colorado® customers who qualify for financial help are looking at an average decrease in their net (after tax credit) premium of 24 percent next year.

The Colorado Division of Insurance today issued final approval for individual health insurance plans that will increase by an average of 5.6% in 2019. The relatively small increase in monthly premiums and the return of all seven health insurance companies to the Connect for Health Colorado, the state’s health insurance Marketplace, are signs of a stabilizing market for Coloradans who buy their own health insurance coverage.

Minnesota, currently entering their second year of their official reinsurance waiver program to help keep unsubsidized premiums down, announced their preliminary 2019 rate hikes way back in June. At the time, the carriers were looking at roughly an 8% average reduction in rates next year...although they would be dropping prices by more like 15% if not for the ACA's individual mandate being repealed and the expansion of #ShortAssPlans.

Today the Minnesota Dept. of Commerce posted the approved 2019 premium changes, and there's been some dramatic reductionsfor three of the five carriers offering policies in the state. Group Health and Medica were approved as is, but Blue Plus was told to drop their rates a whopping 27.7% instead of the 11.8% they were planning on. Ucare was shaved down from a 7 point reduction to 10 points, and PreferredOne (which only sells individual market policies off-exchange and only has 300 enrollees anyway) was knocked down from a 3-point reduction to 11 points.

Tomorrow, HHS Secretary Azar will join Governor Haslam in Nashville, Tennessee to deliver remarks at an event hosted by the Nashville Health Care Council.

Secretary Azar will share news regarding the Affordable Care Act marketplace and reflect on lessons for healthcare reform.

In advance of tomorrow, here are a few excerpts of Secretary Azar’s remarks (as prepared for delivery):

“The previous administration’s major healthcare achievement, the Affordable Care Act, was an attempt to use more government regulation and intervention to improve American healthcare.

“As we all know, the results were disastrous, with skyrocketing costs and disappearing choices.

“But today, I am here to share with you some good news.

Later Wednesday, [Democratic Governor Gina] Raimondo held her own news conference to sign an executive order that, among other steps, directs the state to seek to codify in state law protections for people with preexisting conditions, dependents up to age 26, prescription drug benefits and maternity coverage in case federal action is taken to weaken the Affordable Care Act.

Rhode Island has one of the highest insured rates in the country, and Raimondo said she was defending "Rhode Islanders' access to high-quality, affordable health coverage."

I'm not quite sure what an executive order has to do with codifying ACA protections into law, since that's really up to the state legislature to do, but I guess it at least kicks their butts into gear?

This is also refreshing to hear from a Republican challenger: