“But the plans were on display…”

“On display? I eventually had to go down to the cellar to find them.”

“That’s the display department.”

“With a flashlight.”

“Ah, well, the lights had probably gone.”

“So had the stairs.”

“But look, you found the notice, didn’t you?”

“Yes,” said Arthur, “yes I did. It was on display in the bottom of a locked filing cabinet stuck in a disused lavatory with a sign on the door saying ‘Beware of the Leopard.”

--Douglas Adams, The Hitchhiker's Guide to the Galaxy

Yesterday CMS Administrator Seema Verma posted this on Twitter...

I’m excited by the partnerships that Arkansas has fostered to connect Medicaid beneficiaries to work and educational opportunities, and I look forward to our continued collaboration as we thoroughly evaluate the results of their innovative reforms. #TransformingMedicaid

Iowa has only a single insurance carrier offering ACA-compliant individual market policies this year. Next year they'll have two, as Wellmark has decided to Hokey Pokey their way back onto the exchange again in 2019...but since they weren't around this year, there's no current policy premiums to measure any increase (or decrease) against.

Medica, the sole carrier now selling individual health insurance policies in Iowa, plans to raise its 2019 premiums by less than a tenth as much as it did for 2018.

Medica raised its Iowa health insurance premiums by a staggering average of 57 percent for 2018. It was the steepest such health insurance increase in Iowa history. Company leaders said last summer they needed the higher premiums to stay in the market. But this time around, the Minnesota-based carrier is planning to raise Iowa premiums by an average of less than 5.6 percent, state regulators disclosed Wednesday.

To enter the Fort Worth Courtroom of Judge Reed O’Connor on September 5, 2018, was to leave the real world. The Affordable Care Act was once again on trial. At stake was access to health care for the 20 million Americans who have gained coverage through the ACA, affordable coverage for 133 million Americans with preexisting conditions, and preventive services coverage for 44 million Medicare beneficiaries.

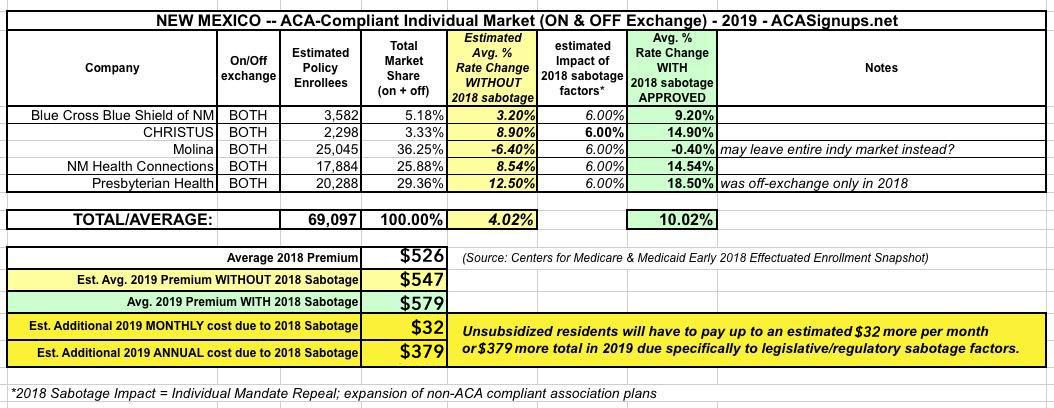

New Mexico was one of the earlier states to post their initial, requested 2019 ACA individual market premium hikes back in June. At the time, the five carriers asked for rate increases ranging from a slight drop (-0.4% for Molina) to as high as an 18.5% increase for Presbyterian Health, which is currently only offering off-exchange policies this year. Based on their preliminary filings, New Mexico was looking at a weighted average increase of around 10.0% next year, which would have been more like 4% if not for this years sabotage efforts by Trump and the GOP (mandate repeal & expansion of #ShortAssPlans):

A few weeks ago, I posted about New Jersey's preliminary 2019 ACA-compliant individual market rate filings. At the time, the official New Jersey Dept. of Banking & Insurance specifically stated that:

Normally at this point in the year I only do full rate hike write-ups for states when their approved rate changes are made public by insurance regulators. I'm making an exception for Texas, however, because my preliminary analysis of the statewide average premium changes back in June was missing a huge portion of the market--I only had around half the ACA individual market accounted for, and I repeatedly warned that the missing enrollment and rate change data could easily skew the statewide average higher or lower.

Well, it's early September now, and not only do I have access to pretty much all of the missing data now, some of the rate filings have changed significantly as well. At the time, I estimated Texas carriers as requesting average rate increases of just 1.5% overall, with them dropping around 10.6% if not for the ACA's individual mandate being repealed and Trump's expansion of #ShortAssPlans.

I received a tip about this early this morning...which, unfortunately, I was unable to scoop anyone with due to being bogged down/caught up with the #TexasFoldEm drama.

Montana insurer wins lawsuit against feds over unpaid cost-sharing reduction payments

Several health insurers have sued the U.S. government over its failure to make cost-sharing reduction payments that help lower healthcare costs for certain consumers. One just scored the first victory. The U.S. Court of Federal Claims ruled in favor of Montana Health Co-op, which sued the federal government for $5.3 million in unpaid cost-sharing reduction payments, finding that the government violated its obligation under the Affordable Care Act when it stopped paying the CSRs in October 2017."

The rest of the article is behind a paywall, but the gist of it is as follows:

U.S. District Court Judge Reed O'Connor, a George W. Bush appointee, vigorously questioned attorneys during the three-hour hearing but gave no indication when he would rule.

Lawyers for the Trump administration partially agreed with the red states' argument, concluding that the removal of Obamacare's individual mandate requires striking down the law's insurance provisions, including protections for people with preexisting medical conditions.

But the administration disagreed on the need for immediate action, arguing that any remedies should not be applied until next year.

{kind=link}