With only 5 days to go before the launch of the 2018 Open Enrollment Period, time is rapidly running out for me to wrap up my 2018 Rate Hike Project. I started this, as I have for 3 years now, back in late early May with the very first requested rate changes out of Virginia, and have been tracking all 50 states as the summer and fall have passed, following every twist and turn of the insane repeal/replace circus in Congress, Trump's bloviating and blathering about "blowing things up" and "letting Obamacare explode", the last-ditch "Graham-Cassidy" sideshow and everything else, right up to and through Trump lowering the boom on cutting off CSR reimbursement payments.

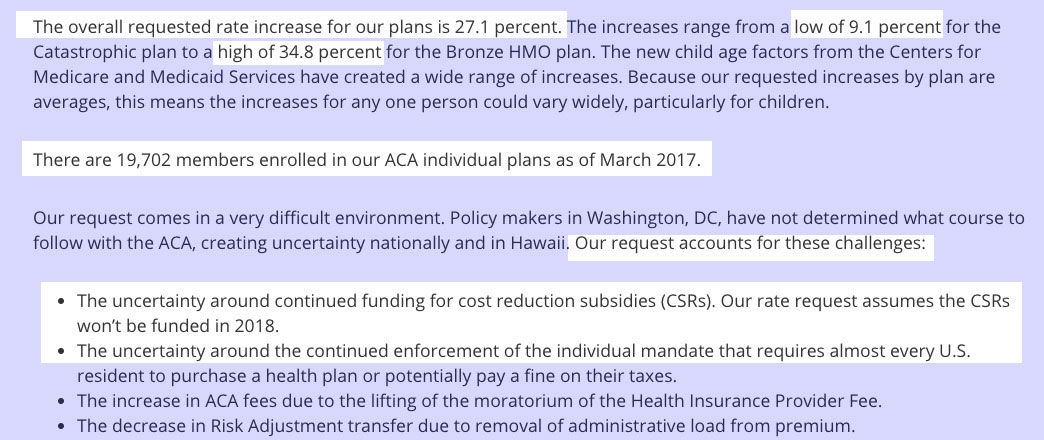

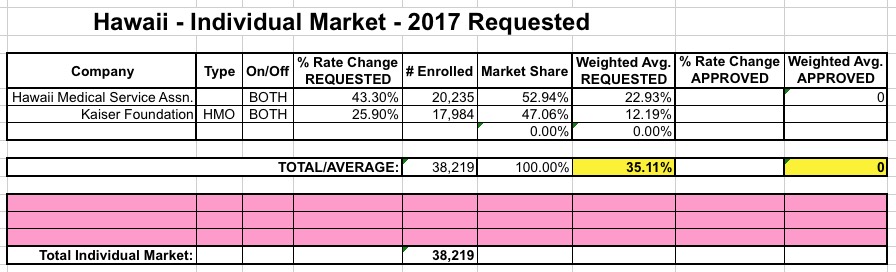

Hawaii only has two carriers on the individual market (and in fact doesn't even have much of an individual market due to a state law mandating that nearly every business provide coverage anyway). HMSA's filing letter is very specific about calling out both the CSR and mandate enforcement sabotage factors as being part of their request. Kaiser doesn't really mention either issue at all, and the only CSR reference in the filing seemed to assume it would be paid, so I have one in each category. Kaiser Family Foundation assumes a 21% Silver CSR rate hike, and 71% of Hawaii's exchange enrollees are on Silver plans, so that amounts to roughly a 15% overall CSR factor.

Here's what it looks like...15.2% w/partial sabotage, 30.2% with full sabotage:

While I've been embroiled in the sturm und drang at the national level, Louise Norris of healthinsurance.org has been reporting on some important stuff happening at the state level:

As of 2017, Hawaii no longer has a SHOP exchange for small businesses. The State Department of Labor and Industrial Relations has an FAQ page about this.

...Hawaii’s waiver aligns the ACA with the state’s existing Prepaid Health Care Act. Under the Prepaid Healthcare Act, employees who work at least 20 hours a week have to be offered employer-sponsored health insurance, and can’t be asked to pay more than 1.5 percent of their wages for employee-only coverage (as opposed to 9.69 percent under the ACA in 2017).

As I'm sure some readers have noticed, I haven't posted any updates since Friday, which is highly unusual for me, especially with open enrollment rapidly approaching. I'm afraid that due to an unfortunate coincidence of timing, I have an outside personal commitment which will be eating up a lot of my time for the next 4 weeks; as a result, expect posts to be lighter than usual.

Kaiser's 25.9% request was approved as is; HMSA's 43.3% was shot down originally; they later resubmitted it at 35%, which was then approved.

You may also notice that I've started making sure to include UNSUBSIDIZED in the headlines for all of these rate hikes. This is vitally important to remember, even if it's only relevant to around 50% of individual market enrollees.

Lots of stuff happening fast & furious these days as #OE4 approaches. Instead of individual posts, I'm gonna cram 7 state updates into a single one...and am also cheating a bit by cribbing off of excellent work by Louise Norris over at healthinsurance.org (which is fair, since she also gets some of her data from me as well):

ALABAMA: Here's what my requested rate hike table looked like for Alabama on August 1st:

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

There are only two insurance carriers participating in Hawaii's individual market next year: The Hawaii Medical Service Association (HMSA) and the Kaiser Foundation Health Plan.

But actually, he thought as he re-adjusted the Ministry of Plenty’s figures, it was not even forgery. It was merely the substitution of one piece of nonsense for another. Most of the material that you were dealing with had no connexion with anything in the real world, not even the kind of connexion that is contained in a direct lie. Statistics were just as much a fantasy in their original version as in their rectified version. A great deal of the time you were expected to make them up out of your head. For example, the Ministry of Plenty’s forecast had estimated the output of boots for the quarter at 145 million pairs. The actual output was given as sixty-two millions. Winston, however, in rewriting the forecast, marked the figure down to fifty-seven millions, so as to allow for the usual claim that the quota had been overfulfilled. In any case, sixty-two millions was no nearer the truth than fifty-seven millions, or than 145 millions. Very likely no boots had been produced at all. Likelier still, nobody knew how many had been produced, much less cared. All one knew was that every quarter astronomical numbers of boots were produced on paper, while perhaps half the population of Oceania went barefoot.

As anyone who's been following the ACA exchange saga over the past few years knows, the original idea was that all 50 states (+DC) would establish their own, individual healthcare exchange, including their own website/technology platform for enrolling residents in private policies (QHPs), Medicaid (supplementing or replacing whatever existing Medicaid system they already had) and small business policies (the ACA's SHOP program). In addition, each state exchange would also have their own board of directors, marketing department, support call center, fee structure for covering the cost of operations and so on.

If things had worked out that way, there would have been 51 different websites where people would enroll in ACA policies, each one independently branded.

For 2016, HMSA has proposed a 45.5 percent rate increase for their individual HMO plan, and nearly a 50 percent rate hike for their individual PPO plan (49.1 percent overall). The carrier justified their rate hikes based on claims costs, explaining that while virtually everyone in Hawaii was already insured, the uninsured pool – many of whom purchased new ACA-compliant plans – had significant medical needs.

Ouch. Yup, that's a pretty ugly requested increase, no way around it.

The following day, Kaiser proposed an 8.7 percent rate increase for their individual market policies.

If approved as is, this would have resulted in a 33.7% average rate increase, when weighted by market share between the two companies.

Hawaii Health Connector offers individual plans from two carriers: BCBS’s Hawaii Medical Service Association (HMSA), and Kaiser Permanente.

For 2016, HMSA has proposed a 45.5 percent rate increase for their individual HMO plan, and nearly a 50 percent rate hike for their individual PPO plan (49.1 percent overall). The carrier justified their rate hikes based on claims costs, explaining that while virtually everyone in Hawaii was already insured, the uninsured pool – many of whom purchased new ACA-compliant plans – had significant medical needs.

Ouch. Yup, that's a pretty ugly requested increase, no way around it.

The following day, Kaiser proposed an 8.7 percent rate increase for their individual market policies.