Once again, I'm afraid the actuarial memos for Kansas' 2021 individual and small group market carriers are either absent or redacted, so I have to run unweighted average rate changes, which are likely off significantly (for instance, the individual market is +7.8% unweighted, but if it turns out that, say, Oscar Insurance has 95% of the market share, the weighted average would be more like a 7% decrease).

Unfortuantely, without knowing the actual enrollment data for each carrier, this is the best I can do for now. The small group market's unweighted average increase is 8.2%.

TOPEKA, Kan. (KWCH) Gov. Laura Kelly and Republican leadership announce an agreement on Medicaid expansion in Kansas.

During a press conference on Thursday, the governor said the program would be funded by the hospital administrative fee. At this time, it's unknown if that fee would be passed on to patients.

Kelly said the hospitals have endorsed the program.

Kansas Senate GOP Majority Leader Jim Denning said the bill would be pre-filed on Thursday with 22 co-sponsors.

If passed in the Kansas Senate and House, the full expansion would go into effect no later than Jan. 1.

(Obviously that's January 1st of 2021 at this point, of course)

Here's some live tweeting of the event by a Kansas-based political reporter:

I didn't have the actual enrollment data for the individual carriers when I ran the numbers for Kansas in August, so I had to go with an unweighted average unsubsidized 2020 premium rate change. At the time, that came in at a 3.1% reduction.

Since then, I've dug up the hard enrollment numbers, and just this morning CMS finally posted the final, approved 2020 rate changes. The weighted average comes in at a slight increase o 0.3% statewide:

Cigna extended its individual healthcare exchange products for the 2020 plan year, the insurer said Sept. 18.

For 2020, individuals can purchase individual health plans in 19 markets across 10 states. The expansions will take place in counties in Kansas, South Florida, Utah, Tennessee and Virginia. The other states include Arizona, Colorado, Illinois and North Carolina.

The plans will be available for purchase on the individual marketplace during the 2020 open enrollment period, which begins Nov. 1. Plans will take effect Jan. 1.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

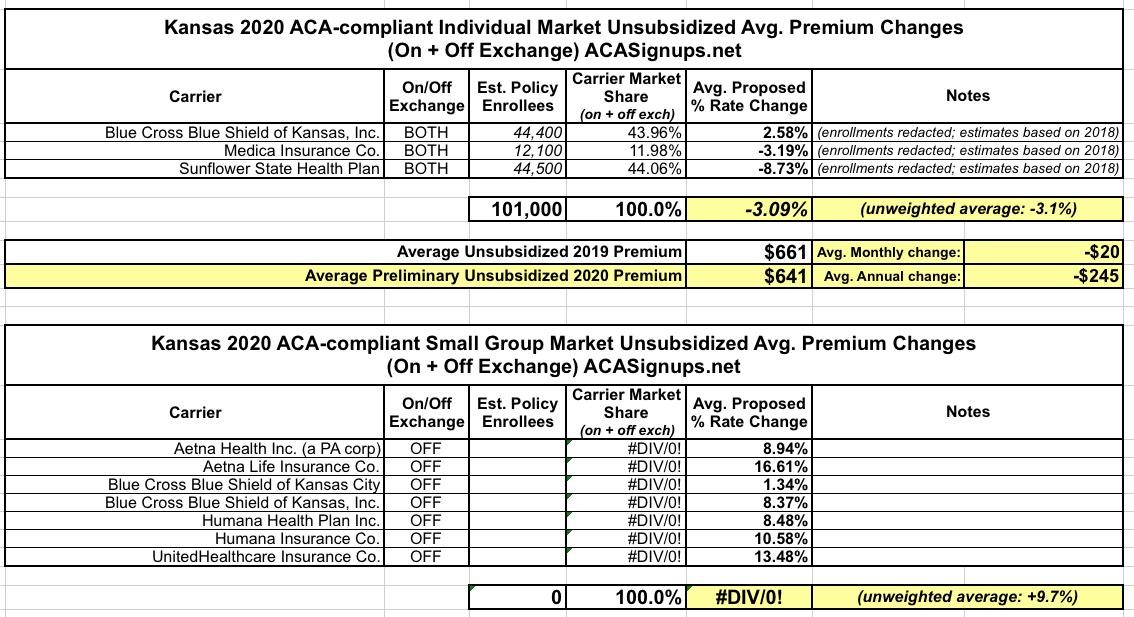

(sigh) Kansas is yet another state where the enrollment data for each of the carriers is redacted on the filing forms this year. To run the weighted average, I'm using last year's estimated enrollment numbers for each, which may have shifted around this year.

Assuming things haven't shfited around too much, unsubsidized Kansans will likely be looking at roughly a 3.1% average premium reduction in 2020...which also happens to be the same as the unweighted average change.

Meanwhile, the small group market is looking at an unweighted average increase of 9.7% statewide.

(sigh) I wrote about "Farm Bureau Plans" several times last year. They've been widespread in Tennessee for a long time, and are a big part of the reason for the state's high ACA premiums (TN doesn't have the highest premiums, but they're definitely near the top of the list). Here's the description of typical Tennessee "Farm Bureau" plans:

Traditional plans require medical underwriting that may affect eligibility and rates. Medical information will be requested for any person over the age of 40 and children 25 months and under; medical records may also be requested if any health condition on the application is marked “yes.” Any fees for obtaining medical information will be at the applicant’s expense.

Underwriting guidelines regarding particular conditions may necessitate a benefit exclusion rider, a member exclusion rider or an adjusted rate for coverage. There will be a 6-month or 12-month waiting period for pre-existing conditions, depending upon the plan chosen.

Kansas House fails to override Brownback Medicaid expansion veto

The effort to expand Medicaid in Kansas fell apart Monday as the House failed to override Gov. Sam Brownback’s veto of a bill that would have expanded the health care program to thousands of low-income people in the state.

The 81-44 vote, three shy of the 84 needed to overcome the governor’s opposition, effectively ends the Medicaid expansion push in Kansas after it successfully passed both chambers with bipartisan support earlier this year.

That was then. This is now. Kansas now has a Democratic governor who supports Medicaid expansion, and yesterday this happened (via Jim McLean of the Kansas News Service):

Premium Rates for Individual and Small Group Markets Individual plan premium rates may vary by age, rating area, family composition and tobacco usage. For example, a person living in Manhattan, KS (rating area 3) may pay a different rate than someone living in Pittsburg, KS (rating area 7) based on the claims data by rating area. A map of the counties included in each rating area is provided on the next page. Kansas is an effective rate review state, which means the actuarial review is conducted by the Kansas Insurance Department. KHIIS (Kansas Health Insurance Information System) claims data is utilized during the rate review process to verify the claims experience submitted by the companies. The following table provides details regarding the average requested rate revisions for companies writing individual policies in Kansas. Rate increases will be partially offset for individuals receiving a premium tax credit.

Kansas is pretty frustrating. There's only three carriers offering ACA individual market policies, but two of the three have heavily redacted actuarial memos, so I don't know what their market share is...and the same two were new (or "semi-new") to the exchange this year so I can't even use last year's effectuated enrollment as a guideline. In light of that, I had to split the estimate right down the middle to get an estimated overall market share.

In addition, Medica is the only one of the three to specifally mention mandate repeal and/or #ShortAssPlans as a contributing factor; that's also redacted in the filings for the other two. Therefore, instead of assuming 2/3 of the Urban Institute's sabotage projection, I'm being extra-cautious and assuming just half (9.6% instead of 19.2%). This gives a rough statewide average increase of around 6.1%, which would likely be closer to a 3.5% premium reduction without mandate repeal and short-term plan expansion.