I posted Montana's preliminary/requested 2019 ACA indiividual market rate change requests back in late June. At the time, they were seeking average rate increases of 6.0% statewide, and I estimated that the GOP's repeal of the ACA's individual mandate penalty, combined with the Trump Administration's expansion of #ShortAssPlans, accounted for about 9.9 percentage points of that.

More recently, the state insurance commissioner's website published approved 2019 rate changes. The average increases have been sliced down slightly (from 6.0% to 5.7% on average), and I've lowered my estimate of #ACASabotage impact from 9.9% to 6% based on the lack of either factor being prominently mentioned in the actual carrier rate filings. If accurate that means rates would have been flat year over year on average in 2019 if not for those factors.

Unsubsidized Montana enrollees are paying an average of $637/month this year, so that's roughly a $38/month difference, or around $460 for the full year.

As I just noted earlier this afternoon, Massachusetts is NOT expecting the repeal of the ACA's individual mandate to impact their 2019 individual market enrollment or premiums for a simple reason: The Bay State never formally repealed their own, pre-ACA mandate penalty. They basically mothballed it once the ACA's version went into effect, and are simply dusting it off for 2019 and beyond now that the federal mandate has been formally repealed.

However, the two mandate penalties don't work quite the same way. For the federal mandate, unless you qualify for an exemption (and there's a whole bunch of those), the penalty for not having ACA-compliant healthcare coverage is (or has been up until now) as follows:

Ready for Open Enrollment, Health Connector sets 2019 plans with lower premium increases, selects community organizations to provide in-person support to residents

Boston – September 13, 2018 – The Massachusetts Health Connector Board of Directors today approved 57 Qualified Health Plans from nine carriers for individuals and families, with new plan designs that create better value for members and premium increases that average under 5 percent from 2018.

Unfortunately, the press release doesn't specify what "under 5%" means, nor does it break that out by carrier/market share. I've put in a request for those details and will update this as soon as I hear back from them. They sent me the following chart, but this only includes enrollees earning between 300-400% of the Federal Poverty Level, which means the marketshare across the entire individual market is likely somewhat different. I'm assuming the 4.4% overall average applies to the entire market but could be wrong about that as well:

For months now, I've been trying to get people to understand that when it comes to sabotage of the Affordable Care Act, especially in terms of individual market premium increases, you have to include the impact of actions taken by Donald Trump and Congressional Republicans in BOTH 2017 and 2018, not just 2018 alone.

In 2017, the single largest factor in the ~28% average national unsubsidized premium increase for ACA plans was Donald Trump's cutting off of Cost Sharing Reduction (CSR) reimbursement payments to carriers. This alone accounted for fully half of the 2018 increase. However, there were other, smaller actions taken which added up to another 3% or so: Slashing the Open Enrollment Period in half, CMS slashing the marketing budget for the federal exchange down 90%, slashing the outreach/navigator budget down 40% and so on.

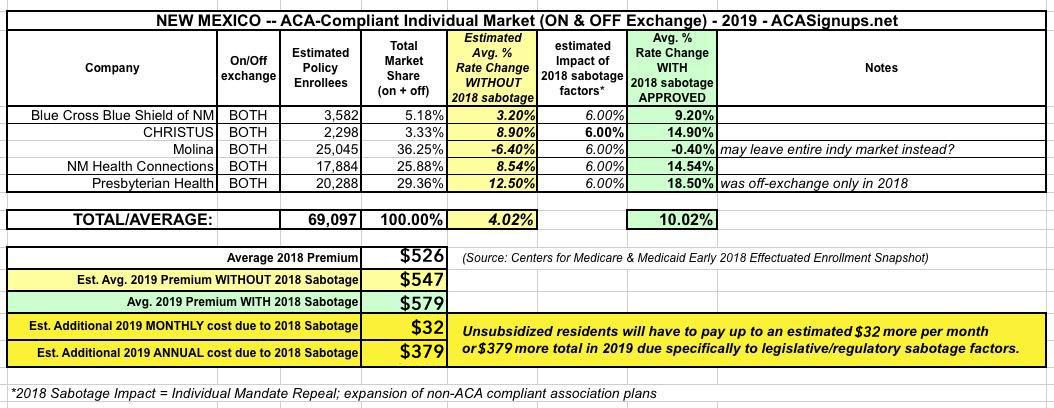

New Mexico was one of the earlier states to post their initial, requested 2019 ACA individual market premium hikes back in June. At the time, the five carriers asked for rate increases ranging from a slight drop (-0.4% for Molina) to as high as an 18.5% increase for Presbyterian Health, which is currently only offering off-exchange policies this year. Based on their preliminary filings, New Mexico was looking at a weighted average increase of around 10.0% next year, which would have been more like 4% if not for this years sabotage efforts by Trump and the GOP (mandate repeal & expansion of #ShortAssPlans):

A few weeks ago, I posted about New Jersey's preliminary 2019 ACA-compliant individual market rate filings. At the time, the official New Jersey Dept. of Banking & Insurance specifically stated that:

Normally at this point in the year I only do full rate hike write-ups for states when their approved rate changes are made public by insurance regulators. I'm making an exception for Texas, however, because my preliminary analysis of the statewide average premium changes back in June was missing a huge portion of the market--I only had around half the ACA individual market accounted for, and I repeatedly warned that the missing enrollment and rate change data could easily skew the statewide average higher or lower.

Well, it's early September now, and not only do I have access to pretty much all of the missing data now, some of the rate filings have changed significantly as well. At the time, I estimated Texas carriers as requesting average rate increases of just 1.5% overall, with them dropping around 10.6% if not for the ACA's individual mandate being repealed and Trump's expansion of #ShortAssPlans.

Back in April, I started an ambitious project which set out to track every legislative or regulatory measure taken by every state to counter, cancel out or mitigate sabotage of the Affordable Care Act by the Trump Administration and Congressional Republicans. It resulted in this color-coded spreadsheet, which lists dozens of bills, proposals, amendments and so on at various stages of completion.

The bad news is that project has proven to be too large for me to keep up with--there's simply too many bills, too many stages and too much other stuff going on for me to keep track of it all.

{kind=link}