BISMARCK, N.D. – Insurance Commissioner Jon Godfread today released the approved health insurance rates for both individual and small group plans for 2021, and encourages consumers to start early, stay informed and shop around.

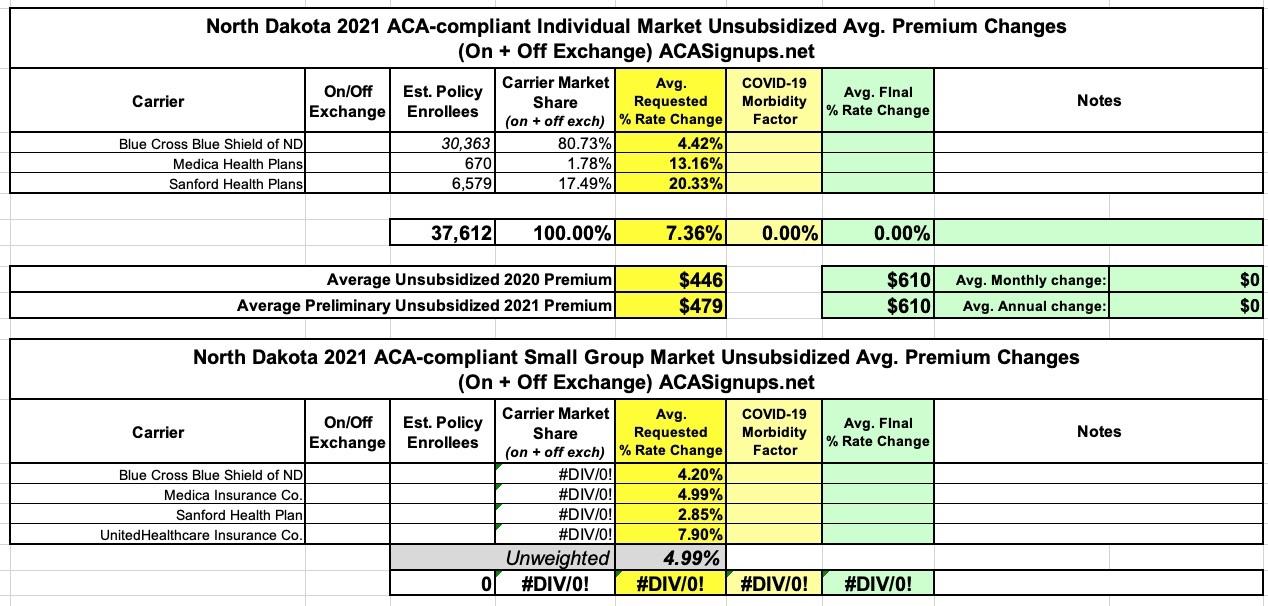

Here's North Dakota's 2021 individual & small group market rate change filings. Note that all of the small group filings are heavily redacted and the memos aren't available in the SERFF database for any of them, so I can't run a weighted average and had to go with the unweighted 5.0% increase.

For the individual market, Blue Cross Blue Shield's memo isn't available, so I had to plug in an estimate based on the average 2019 enrollment; I'm assuming it's fairly close to that this year as well. Weighted average on the indy market is a 7.4% increase.

Last month I noted that North Dakota had posted their requested 2020 premium rate change requests, including two different filings: One assuming the states' ACA Section 1332 Reinsurance Waiver didn't get approved, the other assuming it did. It was pretty unlikely that their waiver would be denied, however, so the general assumption was that they'd be looking at a significant rate reduction, especially compared with the rate increase if the waiver didn't go through.

At the time, I didn't have access to the actual enrollment figures for the three carriers on North Dakota's individual market, so I had to go with an unweighted average rate change, and came up with a drop of 7.9%.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

Unfortunately, North Dakota is another state where the carriers have redacted their rate filings. I was able to garner some info about one of the three carriers participating in the Individual Market next year: Medica's filing redaction wasn't done properly, so I was able to extract that they're looking at medical trend of 7.7%, a morbidity reduction of 1.5%, a 2.3% increase due to the reinstatement of the ACA's insurer fee...and a 20% reduction due to the implementation of the state's reinsurance program, which I first reported on last fall and followed up with this spring.

Last September I noted that North Dakota was considering going one of two ways when it comes to making a major change in their individual insurance market: EIther joining over a half-dozen other states in pushing for a reinsurance program (which I strongly support doing), or going the other way and starting to offer weaker policies without some ACA protections the way states like Idaho, Tennessee, Iowa and Kansas either already do or are in the process of doing.

A few minutes ago I posted about North Dakota'sapproved 2019 rate hikes, which are coming in at a mere 3.2% on average (but which would likely be dropping nearly 20 points without both last and this year's #ACASabotage factors).

As I noted last month when I first analyzed the requested 2019 rates for North Dakota insurers, ND was somewhat unique last year in that it was one of only two states (the other was Vermont) which didn't tack on any extra premium increases for 2018 to account for the lost Cost Sharing Reduction reimbursement revenue after Donald Trump cut off those payments last October.

This led to one of North Dakota's three carriers, Medica, dropping off the ACA exchange altogether, though they still ended up enrolling a few hundred people directly via the off-exchange market.

In direct response to this, Medica Health Plans dropped out of the ND on-exchange individual market this year to avoid taking the CSR hit. They hung around the off-exchange market, however, and therefore still have about 600 enrollees in the state.

20 states went the full #SilverSwitcharoo route (the best option, since it maximizes tax credits for those eligible for them while minimizing the number of unsubsidized enrollees who get hit with the extra CSR load);

16 states went with partial #SilverLoading (the second best option: Subsidized enrollees get bonus assistance, though not as much as in Switch states; more unsubsidized enrollees take the hit, but they aren't hit quite as hard);

6 states went with "Broad Loading", the worst option because everyone gets hit with at least part of the CSR load except for subsidized Silver enrollees;

6 states took a "Mixed" strategy...which is to say, no particular strategy whatsover. The state insurance dept. left it up to each carrier to decide how to handle the CSR issue, and ended up with a hodge podge of the other three

3 states (well, 2 states + DC, anyway) didn't allow CSR costs to be loaded at all. Their carriers have to eat the loss, which makes little sense, but what're ya gonna do?