OPEN ENROLLMENT EXTENDED UNTIL DEC. 22

ONE WEEK ADDED TO ENROLL IN 2018 HEALTH, DENTAL COVERAGE

BALTIMORE (DEC. 13, 2017) – Open enrollment through Maryland Health Connection has been extended until Friday, Dec. 22 to choose a plan for health coverage to begin Jan. 1, 2018, with expanded call center hours through next week.

Individuals can apply at MarylandHealthConnection.gov or through the “Enroll MHC” mobile app available free in the App Store (iOS) and the Google Play Store (Android).

Also, hundreds of insurance brokers and navigators around the state can help Marylanders apply for financial help and enroll in a plan. Their locations and contact information are available at MarylandHealthConnection.gov or through a GPS-enabled locator tool on the app.

UPDATE: Minor updates out of New York and Washington State added later today have nudged the official national QHP selection tally over the 7.0 million mark. All numbers below have been updated to include these additions.

UPDATE 12/14/17: With the latest update from California, the confirmed national QHP selection total has now officially broken 7.1 million.

Week 6, Dec 3- Dec 9, 2017

In week six of Open Enrollment for 2018, 1,073,921 people selected plans using the HealthCare.gov platform. As in past years, enrollment weeks are measured Sunday through Saturday.

At week six of Open Enrollment nearly 29,000 Rhode Islanders have enrolled in coverage, which is about five percent more than last year. HealthSource RI continues to see an increase in new customers. We have more than three times the number of new enrollees this Open Enrollment period compared to the previous. HealthSource RI is pleased to see an increase in customers age 18-34, often known as “young invincibles.” While 25 percent of our renewing customers are age 18-34, 34 percent of our new customers fall into this age group.

Rhode Island is a tiny state, of course, so this doesn't necessarily mean much nationally, but it's great news across the board nonetheless.

According to the CMS Public Use File, Rhode Island's official tally as of 12/10/16 was 27,555 enrollees; 29,000 is indeed 5.2% higher. In fact, they only need 500 more people to beat their OE4 numbers, though they'd have to add another 5,700 to reach the all-time Rhode Island record of 34,670 set in OE3.

This is a really minor update, but every person counts; as of December 10th...

260,391 plans selected and enrollments (reminder, we did auto renewal last month, so this includes current members)

29,115 plans selected and enrollments by people who currently don’t have coverage through the Exchange (these are part of the 260,391)

This is a mere 576 higher than MA's tally from four days earlier, but considering auto-renewals are included, it makes sense: The odds are that a couple thousand of those auto-renewed went back in and cancelled their renewals, partly cancelling out some of the new enrollment numbers.

Anyway, the CMS Public Use File lists Massachusetts as officially enrolling 247,121 people as of December 10th last year, so they're still running 5.3% ahead of that. They need 6,300 more enrollees (net) to break last year's record...but keep in mind that MA is one of the states with an extended deadline: Baystaters can still enroll as late as January 23rd.

A few days ago I noted that based on a rather cryptic press release from Connect for Health Colorado, I deduced that C4HCO had enrolled a minimum of 53,000 people in 2018 ACA exchange policies as of December 7th. Today, however, Louise Norris has clarified that the actual 12/07 tally in CO was 59,590...and that this does not include auto-renewals, as some of the other state-based exchanges have already done:

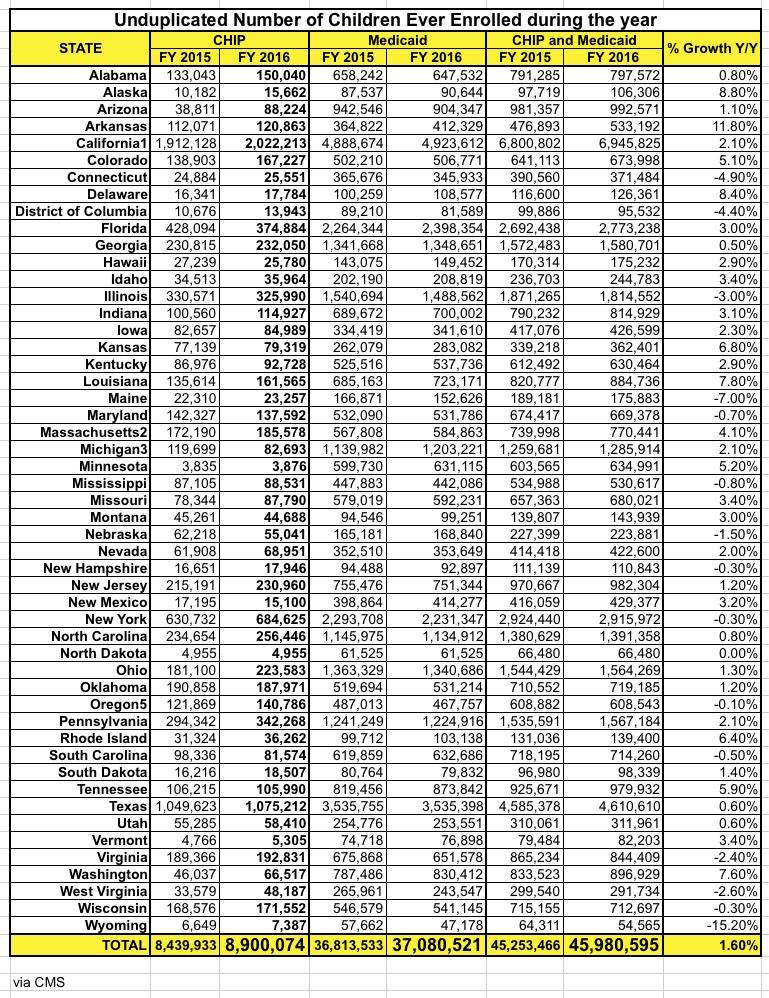

Not much to add to this. Here's the state-level breakout of how many children were enrolled in the CHIP program in 2016; it inched slightly upwards this year:

(sigh) An anonymous emailer just gave me this heads' up:

New Jersey has no local TV stations. It all comes out of NYC for the most part with the south getting Philly.

Commercials from insurance companies in NY give the enrollment end date at Jan 31. Fidelis Care appears to be the most active at the moment but the real activity will come at the end of next month.

I think many people in NJ will think they have till Jan 31 to enroll.

I do not know if the issue exists between other borders between states with different cutoffs.

This is an excellent point. New York runs their own ACA exchange, NY State of Health...and their 2018 Open Enrollment Period runs all the way through January 31st (although you do have to enroll by Friday in order to have coverage starting on January 1st).

New Jersey, on the other hand, is run through the federal exchange, HealthCare.Gov, and for NJ residents the final deadline for all of 2018 is Friday.

Given how much I've been shouting from the rooftops about the importance of everyone #GettingCovered the past month or so, I'm fully aware of the irony of what I'm about to say:

My wife and I finally #GotCovered this morning at HealthCare.Gov.

We logged into our current account, reviewed our options and in the end settled on...pretty much the same Gold HMO we already have today. It's actually a slightly different policy--Blue Care Network of MIchigan elimiated the "HMO Select" option and replaced it with the "HMO Preferred" option. As far as we can tell, the only differences are the (unsubsidized) premium price, which shot up by about $300/month (ouch.) and the deductible, when went up from $500 to $1,000.

For us, we had two major decisions to make: Gold vs. Silver...and (assuming we had gone with Silver), On-Exchange vs. Off-Exchange.

As I have said, the pace of plan selections continues to run ahead of all previous years but there are plenty of people yet to act to avoid a gap in coverage. Our message remains: Don’t leave money on the table. We know from our own survey that too often Coloradans who are eligible for financial help assume that they make too much to get an Advance Premium Tax Credit.

OK. Last year (OE4) was Colorado's best year so far, with 161,568 QHP selections as of 1/31/17. According to the CMS Public Use File, they hit 42,796 as of 12/03/16 and 59,407 as of 12/10/16. That's an average of 2,373 per day between 12/04 - 12/10, which means they should have reached a minimum of 52,288 QHPs as of 12/07/16.