Iowa's chief insurance regulator has approved double-digit premium rate increases affecting thousands of Iowans.

The Iowa Insurance Division said Wednesday that Insurance Commissioner Nick Gerhart has approved increases requested by Wellmark Blue Cross & Blue Shield, Coventry Health Care and Gundersen Health Insurance.

All of the rate increases are for policyholders holding individual health insurance plans. They will go into effect Jan. 1.

The new rates will affect about 300,000 people who buy health insurance on their own or work for small businesses with 50 or fewer employees and will renew plans in January.

...The rate hikes approved by the state mean that premiums for individuals and small businesses will rise 6.3 percent next year, on average, but the costs for some plans will rise more, and others less. This year, rates for individuals and small employers rose an average of 3.1 percent in January, after increasing 1.9 percent in 2014.

Blue Cross of Idaho’s rates for individuals buying their own plans will go up an average of 23 percent. Company officials say the increase is needed after Blue Cross lost millions of dollars because current customer premiums are not keeping up with claims paid.

Last year, the company’s average rate increase for individual policies was about 15 percent. That year, the company paid nearly $221.1 million in claims while receiving $188.7 in premiums.

Other average rate changes for 2016, including for plans sold off the Idaho health insurance exchange:

Mountain Health COOP: 26 percent

SelectHealth: 15 percent

Regence BlueShield of Idaho: 10 percent

BridgeSpan Health, a sister company of Regence: 7 percent

PacificSource Health Plans: -8 percent

State Insurance Director Dean Cameron said he did not find any proposed rate changes to be unreasonable.

JUNEAU — The state Division of Insurance has approved average rate increases for next year of nearly 40 percent for the two companies providing individual health insurance plans through the federally run online marketplace.

Division director Lori Wing-Heier says Premera Blue Cross Blue Shield and Moda Health cited the high cost of medical services as one of the factors in requesting rate increases.

She also said Alaska has a relatively small market and very small group of individuals with high-cost claims.

She said the average rate increase approved for Premera was 38.7 percent and 39.6 percent for Moda. She said that applies to individual plans on and off the online marketplace.

Wing-Heier says the cost of health care in Alaska has been a long-standing concern, with no clear answers for addressing it.

Well I'll be damned. Given all the tea leaf/entrail-reading that I've had to do in some states to try and piece together the weighted average rate increases for 2016 (usually due to missing enrollment/market share data for the companies participating), it's a pleasant surprise to see that my own state of Michigan has posted the approved rate hikes without any gobbledygook:

Individual market to increase on average 6.5%, small group 1.0%

FOR IMMEDIATE RELEASE - August 18, 2015

LANSING - Michigan consumers and small businesses will experience lower increases in the cost of their 2016 health insurance plan than those in many other states, according to the Michigan Department of Insurance and Financial Services (DIFS). DIFS reports that the average approved rate changes on a premium weighted basis increased by 6.5 percent for the individual market and 1 percent for the small group market.

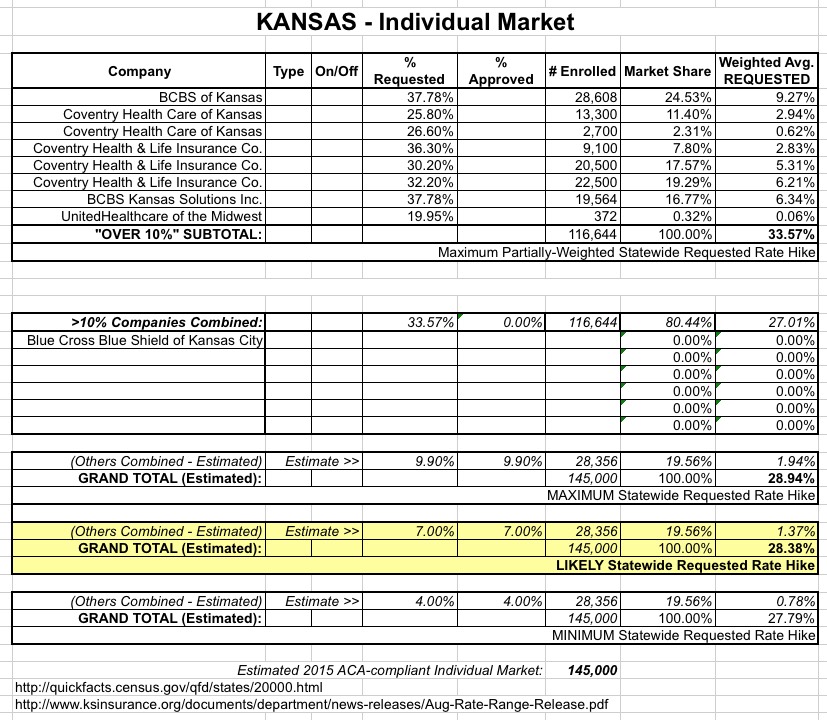

OK, the bad news is that the requested 2016 individual market rate increases in Kansas were somewhere around 28%, with some as high as 38%. This would have looked something like this:

Ouch. The good news (well...relatively good, anyway), is that in the end, the approved rate hikes are considerably less...although still not pretty:

Premiums for Kansas health insurance plans offered in the federal marketplace won’t increase as much as originally proposed, state Insurance Commissioner Ken Selzer said Tuesday.

Kansas Insurance Commissioner Ken Selzer said Tuesday that premiums for health insurance plans offered in the federal marketplace won’t increase as much as originally proposed.

OLYMPIA, Wash. –The Office of the Insurance Commissioner has approved 136 individual health plans from 12 insurers who will offer them to the Exchange, Wahealthplanfinder, for sale in 2016. The Washington Health Benefit Exchange Board is scheduled to certify the approved insurers and their plans at its board meeting later today.

The companies requested an average rate change of 5.4 percent, but 4.2 percent was approved.

Yes, I'm back. From what I can tell, the major Obamacare/health insurance-related stories while I was out were a) Scott Walker/Marco Rubio finally releasing their proposed "replacement plans" (such as they are) for the ACA, and b) the approved 2016 rate changes for ACA-compliant individual/small group policies across a whole mess of states (technically all 50 states +DC had to be finalized as of 2 days ago, but it'll still take awhile to dig up all of them, since many news stories & reports may leave out off-exchange plans, increases of less than 10% and/or actual market share for weighting purposes).

I'm ignoring the Walker/Rubio story for the moment, mainly because they're both complete jokes, but will write up something about that later. For now, let's dive into the approved 2016 rate change story, starting with Arkansas.

Vermont was one of the earliest states to report their requested rate hikes back in mid-May. Due to Vermont's small size (both in total population as well as insurance providers...there's only two of them even operating on the individual markets), as well as their unique law requiring that all individual policies be purchased through the ACA exchange, they were also one of the easiest to calculate.

In addition, as far as I can tell, in Vermont, both the individual and small group markets are considered part of the same rate pool, although the market share differences between the two still resulted in slightly different weighted averages: 7.8% for the individual market, 8.1% for the small group market. These were slightly revised to 8.0% and 8.3% just prior to the review/approval process.