Back in August, I posted a rough analysis of the requested rate increase situation for Wisconsin's individual market carriers. However, I cautioned at the time that I was missing the enrollment market share numbers for four of the carriers (Aspirus, Compcare, Wisconsin Physician Service and WPS), and therefore had to guess at how the rate hikes for those carriers would impact the statewide average. I estimated the numbers assuming CSR payments are made at 21.7%, and from that assumed the impact of CSR reimbursements not being made would be around 7.8 additional points being tacked onto the average.

A couple of weeks ago, the state insurance commissioner announced the approved rate increases. The good news is that I overestimated on the "CSRs paid" front. The bad news is that I underestimated on the "CSRs not paid" front: It's actually 20% and 36% respectively:

On November 10, 2016, at 4:30 in the morning, I was still in a bit of a dazed state trying to absorb the reality that a racist, misogynistic, xenophobic con-artist sexual predator moron was about to become the next President of the United States. We were 9 days into the 2017 Open Enrollment Period, and I realized that there was absolutely no way of knowing what sort of impact the election results might end up having on how many people would sign up for coverage.

Up until a week ago, the possibility of Donald Trump pulling the plug on Cost Sharing Reduction reimbursement payments was a looming threat every day. While it hadn't actually happened yet, most of the state insurance commissioners and/or insurance carriers themselves saw the potential writing on the wall and priced their 2018 premiums accordingly (or at the very least prepared two different sets of rate filings to cover either contingency).

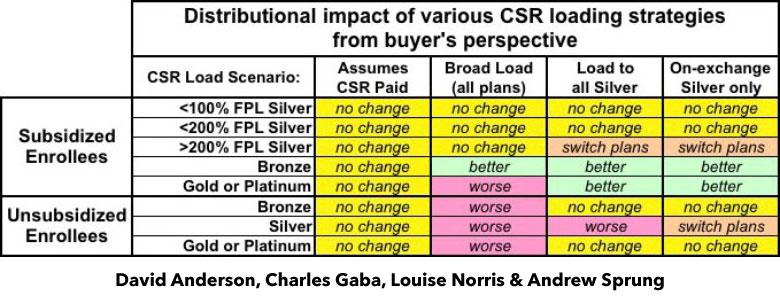

A few spread the extra CSR load across all policies, both on and off the exchange. This seems like the "fairest" way of handling things on the surface, but is actually the worst way to do so, because it hurts all unsubsidized enrollees no matter what they choose for 2018 and can even make things slightly worse for some subsidized enrollees in Gold or Platinum plans.

The approved rate increases for NJ were just released, and the numbers appear to be pretty close to that, if a bit higher: 9.9% and 22.0% respectively.

Truth be told, I only have the hard numbers for the exchange-based carriers...and even those aren't technically official; they come from this NJ.com article:

TRENTON -- New Jersey residents who bought their own health coverage from Horizon Blue Cross Blue Shield through the Affordable Care Act could pay an average of 24 percent more next year, according to state-approved rates released on Tuesday.

Horizon is one of three insurance companies in New Jersey participating in the Obamacare marketplace in 2018. But it is the most dominant, insuring 72 percent of the 244,000 individual policy holders this year.

I first looked at Rhode Island's proposed rate hikes back in early July. At the time, the average increase for the two carriers participating in RI's individual market was 10.5% assuming CSR reimbursement payments are guaranteed for 2018. If they weren't guaranteed, however, I estimated at the time that an additional 19 percentage points would be added into the mix, based on an estimate by the Kaiser Family Foundation.

However, I realized a little later on that I was misinterpreting KFF's analysis; they were referring to how much they estimated silver plans would go up due to the lost CSR funds, not all metal levels. Furthermore, for Medicaid expansion states (which includes Rhode Island) they estimated the average was only 15%.. Based on these factors, the impact across the board on Rhode Island should have only been around 10.3%.

Way back in May, Blue Cross Blue Shield of North Carolina submitted their initial 2018 rate requests to the state insurance department, and noted at the time that they'd normally only be requesting an 8.8% average rate increase...but that due specifically to Donald Trump's threat to cut off CSR reimbursement payments, they were asking for a 23.3% increase instead. I noted that this meant that about 60% of their increase request was caused by Trump's CSR threat.

Then, in August, they gave a somewhat more positive news update: They were lowering their requested rate hike to 14.1%. Basically, their latest numbers had come in and the balance sheet was doing quite a bit better than they had previously thought:

Blue Cross said May 25 that the 22.9 percent rate increase was based on the subsidies ending, along with claims data from the first quarter of 2017. It projected an 8.8 percent rate increase with the subsidies remaining in place.

OK, I was in on the Breaking News a few hours ago; unfortunately a) I had to pick my kid up from school and b) our power went out. (I'm currently online via our generator). As a result, I haven't actually posted anything here at the site about the just-announced Alexander-Murray deal until now.

Sen. Lamar Alexander says he and Sen. Patty Murray have reached a deal to fund the Affordable Care Act's cost-sharing subsidies in exchange for giving states more regulatory flexibility with the law. Shortly after Alexander announced the deal to reporters, President Trump called it a "good short term solution."

OK, right off the bat: I guarantee you that Donald Trump (who just yesterday ranted about how "Obamacare is 'dead' and 'gone') doesn't have the slightest friggin' clue whether this (or any other deal) is "good" or "bad". He hasn't read it and he wouldn't understand any of it if he tried to anyway.

Medica Leaving North Dakota Individual Health Insurance Exchange in 2018

Post date: Sep 28, 2017

BISMARCK, N.D. – Insurance Commissioner Jon Godfread today confirmed that the Insurance Department was informed late Wednesday, Sept. 27, that Medica does not intend to sign an agreement with the federal government to offer coverage on the Affordable Care Act (ACA) Exchange for their individual health insurance in North Dakota for 2018.

“We have had numerous conversations with Medica over the course of the past few months, and given the uncertainty that currently exists around cost sharing reductions, they are unable to move forward in the Federal Exchange,” Godfread said.

Things were looking pretty dicey for two of Montana's three insurance carriers participating on the individual market the past few days. One of the three, Blue Cross Blue Shield, saw the writing on the wall regarding Cost Sharing Reductions (CSR) likely being cut off and filed a hefty 23% rate hike request with the state insurance department. The other two, however (PacificSource and the Montana Health Co-Op, one of a handful of ACA-created cooperatives stll around, assumed that the CSR payments would still be around next year and only filed single-digit rate increases.

I'm not going to speculate as to the reasons why they both did so when it was patently obvious that having the CSRs cut off was a distinct possibility, although I seem to recall the CEO of the Montana Co-Op said something about their hands being tied since CSR reimbursement payments are legally required, after all. Basically, it sounds like he was genuinely trying to avoid passing on any more additional costs to their enrollees than they had to.

As in most states, the Michigan Dept. of Financial Services, seeing the potential writing on the wall, sent out a memo to all individual market insurance carriers instructing them to submit two different sets of rate filings for 2018: One assuming CSR payments would continue, the other assuming they won't: