Under the RSC Health Care Task Force plan, protections pertaining to guaranteed issue and the prohibition on coverage exclusions would be retailored to reward continuous coverage and promote portability in the individual marketplace.

"RETAILORED." DANGER WILL ROBINSON.

Scratch Guaranteed Issue.

Additionally, to provide Americans with options that fit their individualized needs, each state would again be allowed to determine the minimum attributes and cost-sharing parameters of plans to best meet the needs of their own citizens. In no case, however, would carriers be able to rescind, increase rates, or refuse to renew one’s health insurance simply because a person developed a condition after enrollment.

Since Donald Trump was defeated in the 2020 Presidential election, most people seemed to be under the impression that the Republican Party's decade-long obsession with tearing down President Obama's signature legislative accomplishment, the Patient Protection & Affordable Care Act, was finally over.

Healthcare journalist extraordinaire Jonathan Cohn even pulled the trigger on publishing his definitive history of the ACA, The Ten Year War...although honestly, there was still one remaining major legal loose end to tie up which wouldn't happen until about eight months later.

While the Census found the percentage of Americans without insurance fell, even as a supplemental poverty measure increased following the end of pandemic-era assistance, ranking House Ways & Means Committee Democrat Richard Neal (MA) is highlighting the need to extend the enhanced Affordable Care Act credits that are set to expire at the end of 2025.

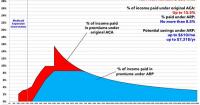

A new Covered California analysis describes the potential impact to consumers if the increased health insurance subsidies that were part of the American Rescue Plan are allowed to expire at the end of 2022.

In California, all consumers would face premium increases, including 1 million lower-income consumers (individuals earning less than $32,200 per year), who would see their premiums more than double.

In addition, middle-income individuals and families (for individuals, those earning more than $51,520 per year), would no longer be eligible for any financial help and would face higher monthly premium costs that for many will mean annual cost increases in the thousands of dollars.

The increase in costs could force more than 150,000 people in California and more than 1.7 million nationally to drop their health insurance.

Several fellow health wonks have chimed in. I spitballed perhaps 95%. Fann puts it at 96-97%. Cynthia Cox of the Kaiser Family Foundation thinks it could be even higher:

The Trends in Subsidized and Unsubsidized Enrollment Report

The report shows that people who do not qualify for APTC continue to be priced out of the market. Following a decline of 1.3 million unsubsidized people in 2017, another 1.2 million unsubsidized people left the market in 2018. These enrollment declines among unsubsidized enrollees coincided with increases in average monthly premiums of 21 percent in 2017 and 26 percent in 2018.

Provide a 20 Percent Health Insurance Premium Subsidy

The Governor will take immediate action by creating a subsidy program to reduce by 20 percent the monthly premiums for Minnesotans who receive their insurance through MNSure. This subsidy will be applied directly against a consumer’s premiums. This proposal provides relief to Minnesotans with incomes over 400 percent of the federal poverty level do not qualify for the federal premium tax credit which helps lower the costs of health insurance premiums. Up to 80,000 people could participate in the program, reducing the out-of-pocket costs of their health insurance premiums.

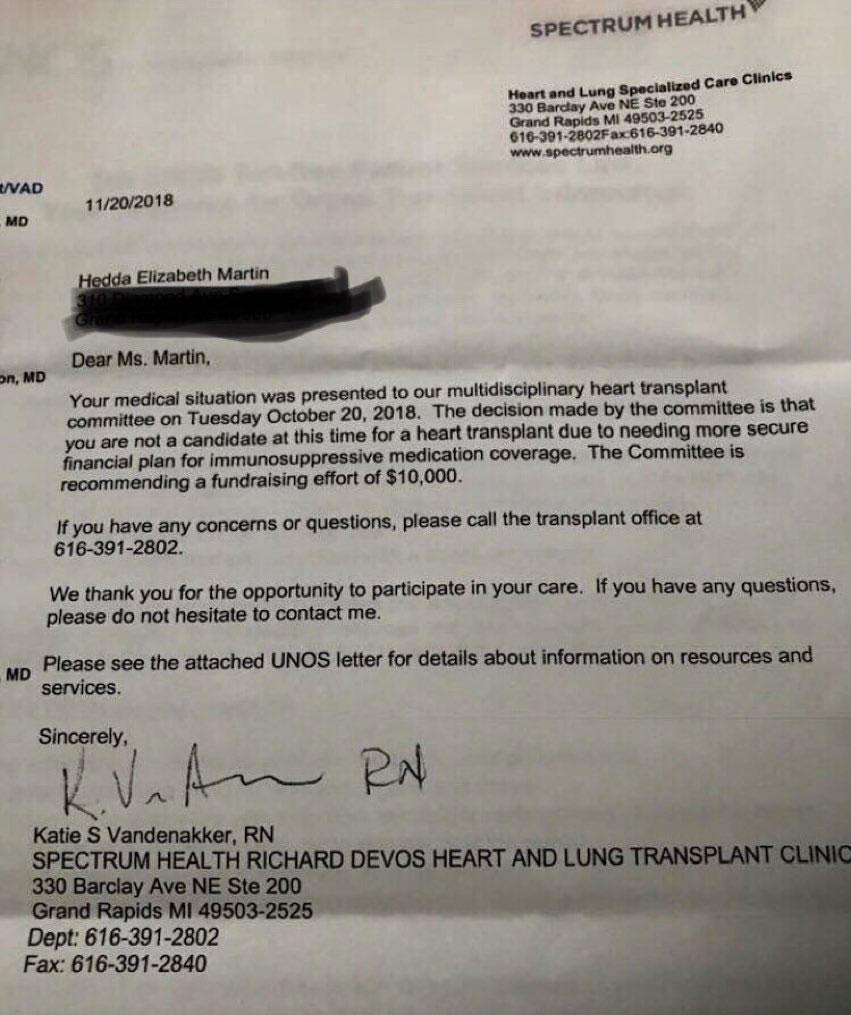

Earlier this week, a picture of a letter sent to a patient needing a heart transplant recommending that they find a way to raise $10,000 to cover some costs went viral on Twitter and Facebook, with various celebrities, politicians etc. reposting it.

I'm sure you've seen it already, but just for the record, here's one of the most viral variants, from freshman Congresswoman-elect Alexandra Ocasio-Cortz. It's important to clarify that the letter was not sent by the insurance carrier, and the $10K in question would not be going to pay an insurance company...or, in fact, even "Spectrum Health" aka the "Heart & Lung Specialized Care Clinics" noted in the letterhead.

Insurance groups are recommending GoFundMe as official policy - where customers can die if they can’t raise the goal in time - but sure, single payer healthcare is unreasonable.

Given how much I've been shouting from the rooftops about the importance of everyone #GettingCovered the past month or so, I'm fully aware of the irony of what I'm about to say:

My wife and I finally #GotCovered this morning at HealthCare.Gov.

We logged into our current account, reviewed our options and in the end settled on...pretty much the same Gold HMO we already have today. It's actually a slightly different policy--Blue Care Network of MIchigan elimiated the "HMO Select" option and replaced it with the "HMO Preferred" option. As far as we can tell, the only differences are the (unsubsidized) premium price, which shot up by about $300/month (ouch.) and the deductible, when went up from $500 to $1,000.

For us, we had two major decisions to make: Gold vs. Silver...and (assuming we had gone with Silver), On-Exchange vs. Off-Exchange.