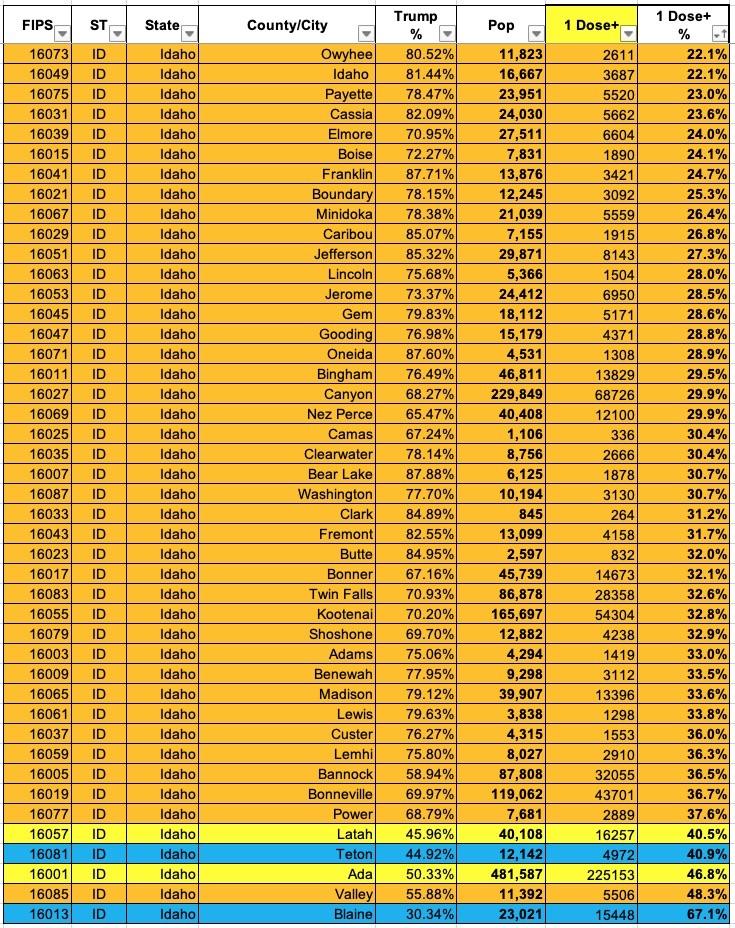

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

The ACA's language didn't account for the possibility that some states might not expand Medicaid, which is why the lower-end range of exchange plan subsidy eligibility starts off at 100% FPL...

Unfortunately, those earning less than 100% FPL are still stuck without any viable options besides either "going bare" and praying they don't get sick or injured or possibly buying a junk plan of some sort. According to the Kaiser Family Foundation, there's around 2.2 million Americans still caught in the "Medicaid Gap", where they don't qualify for Medicaid but don't earn enough to be eligible for subsidized ACA exchange policies (Kaiser estimates another 1.8 million uninsured adults in these states in the 100 - 138% "overlap" cateogory, plus around 356,000 who are eligible for Medicaid but still haven't enrolled for one reason or another).

Tennessee has also posted their preliminary 2021 rate filings for both the individual and small group markets. Aside from being one of the few states where a significant number of carriers are including any COVID-19 pandemic factor at all (in both markets), Tennessee has several new entrants and one significant withdrawl (I think).

On the individual market, UnitedHealthcare is newly entering, while Cigna is expanding their coverage areas as noted here. Cigna is also newly entering Tennessee's small group market, as is Bright Health Insurance.

Overall, Tennessee carriers are asking for a 10.3% increase on the indy market (the second highest so far after New York's 11.7% average), mostly driven by Blue Cross Blue Shield, which holds a whopping 83% of the market. On the small group market, the average increase is 5.5%.

COVID-19 accounts for 1.7 points of the increase on average in the indy market and 2.6 points in the small group market. This, again, is the highest statewide average COVID impact I've seen after New York state so far.

Cigna extended its individual healthcare exchange products for the 2020 plan year, the insurer said Sept. 18.

For 2020, individuals can purchase individual health plans in 19 markets across 10 states. The expansions will take place in counties in Kansas, South Florida, Utah, Tennessee and Virginia. The other states include Arizona, Colorado, Illinois and North Carolina.

The plans will be available for purchase on the individual marketplace during the 2020 open enrollment period, which begins Nov. 1. Plans will take effect Jan. 1.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

TDCI Approves Carriers’ 2020 Rates on the Federally Facilitated Marketplace

More Choices, Rate Decrease Highlight Rating Filing Season

The Tennessee Department of Commerce and Insurance (TDCI) announces the approval of insurance rates requested by the five carriers offering coverage on the Federally Facilitated Marketplace (FFM) in 2020.

A new set of proposals provide some of the strongest evidence yet that Obamacare -- once on the verge of collapse in Tennessee -- has stabilized.

The state’s largest insurance company, BlueCross BlueShield of Tennessee, plans to reenter the Affordable Care Act marketplace in Nashville, Memphis and surrounding counties next year, providing another option for residents on Obamacare. Additionally, two other insurance companies that already offer Obamacare in these cities, Cigna and Oscar Health, are planning to significantly reduce the cost of their coverage plans.

Although the proposals are not final, it appears Tennesseans will have more options and competitive prices in the coming year, said Kevin Walters, a spokesman for the Department of Commerce and Insurance.

The Tennessee House of Representatives passed a bill on Thursday that would ban abortion after a fetal heartbeat is detected, mimicking laws in other states that have been struck down by the courts and drawing the criticism of both advocates and opponents of abortion rights.

The measure, House Bill 77, would tightly restrict the window of time within which a woman could seek an abortion, because a fetal heartbeat can be detected as early as six weeks into a pregnancy. That is before many women even realize they are pregnant.

When I last posted about 2019 ACA-compliant individual market premium changes in Tennessee back in August, I noted that premiums statewide had gone from dropping 5.7% to dropping 10.8% on average after the Trump Administration first stated that they were going to unnecessarily "freeze" the ACA's Risk Adjustment fund transfers in response to a lawsuit ruling only to reverse themselves a week or so later and state that they were going to go ahead and process RA fund transfers after all.

In other words, the Trump Administration once again deliberately caused a panic across the industry only to "save" the industry from the very threat which they had posed in the first place.

In any event, here's what I thought the Tennessee's premium situation looked like when the dust settled:

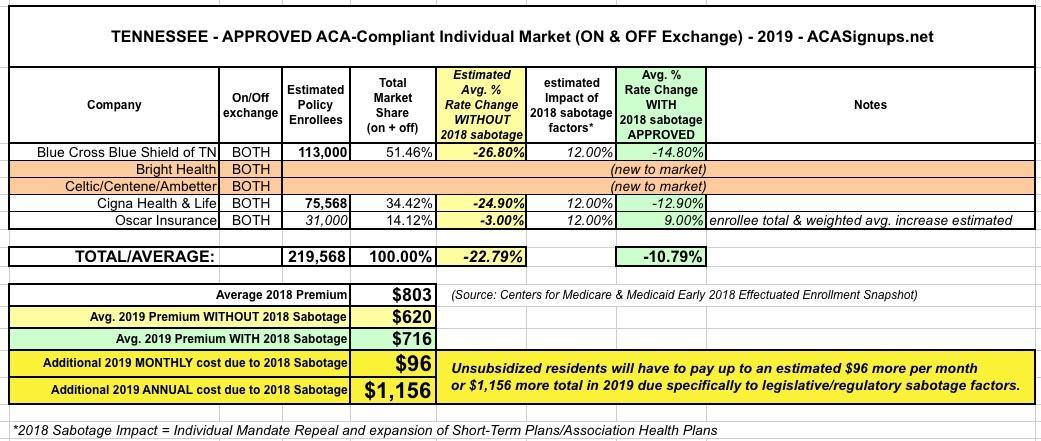

The good news was that average unsubsidized 2019 ACA individual market premiums were expected to drop by about 5.7% after years of double-digit rate hikes.

The bad news was that due specifically to various types of deliberate sabotage by the Trump Administration and Congressional Republicans (primarily repeal of the individual mandate and expansion of #ShortAssPlans), that 5.7% drop was still a good 12 points or so higher than it otherwise would have been.

The ugly news was that due specifically to the Trump Administration's utterly unnecessary decision to freeze Risk Adjustment fund transfers in response to a lawsuit out of New Mexico, 2019 premiums would be hundreds of dollars higher still than they should have been for Blue Cross Blue Shield of Tennessee's 113,000 enrollees:

{kind=link}