The database at the link above doesn't include the enrollee market share numbers; for that I had to dig up the actual filings at the SERFF database. Blue Cross Blue Shield and Presbyterian seem to be assuming no significant TrumpTax next year (which makes sense, since both will be off-exchange only, thus not subject to CSR payment concerns). Molina's filing is kind of odd--they seem to assume that CSR payments will be made...but that the individual mandate won't be enforced, which seems rather backwards to me (most TrumpTax filings assume neither will be enforced, or that the mandate will but CSR payments won't).

A shout-out to Jeremy Johnson for the heads up: The Montana Commissioner of Securities & Insurance has released their preliminary 2018 rate requests for the individual and small group markets...and it's pretty darned straightforward. As a nice bonus, they even saved me the trouble of digging up the effected enrollee numbers. In fact, the only critical data missing are the "Part II Justification" files, which hopefully clarify how the CSR payment/mandate enforcement situation plays into these requests.

Judging by the requests, it looks like at least 2 of the 3 on the individual market are assuming that CSR payments will continue and the mandate penalty will be enforced. As for the third (BCBSMT), they're asking for a 23.1% rate hike, so I honestly don't know whether that includes the TrumpTax or not. For the moment I'll assume it doesn't, but will change this later if I'm wrong about that.

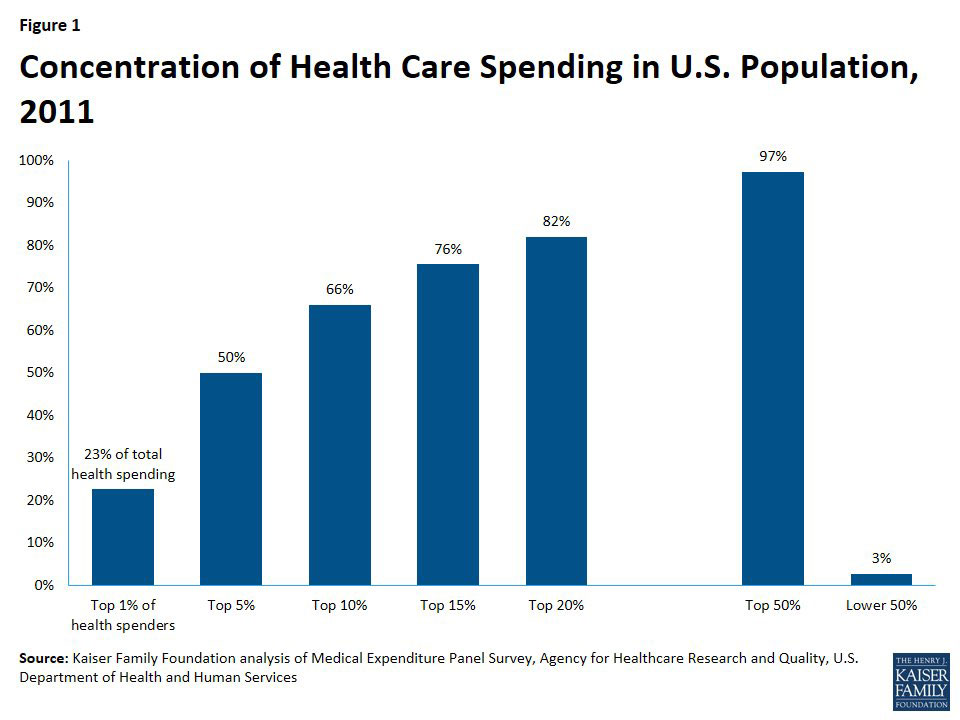

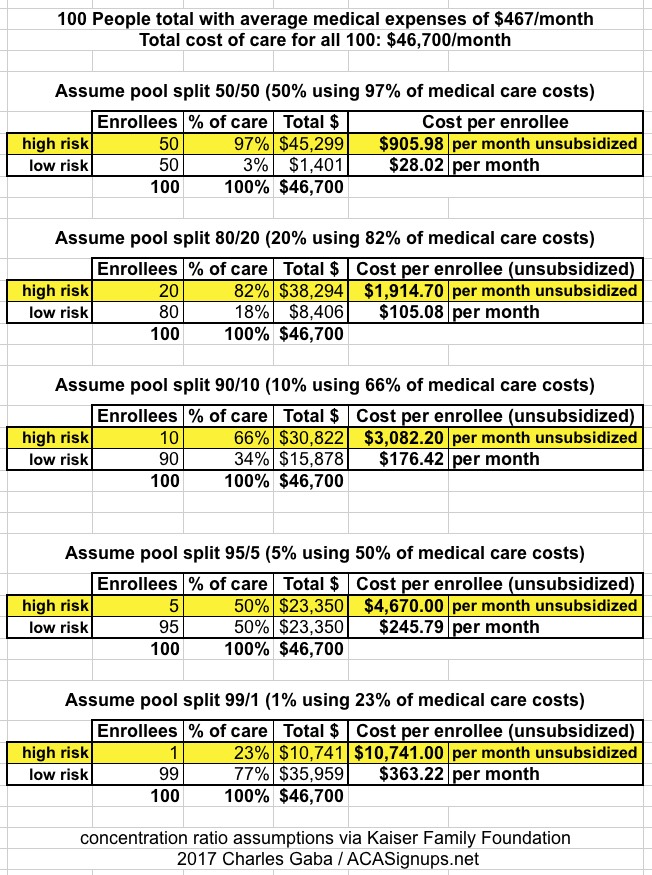

Last week I noted that Ted Cruz's proposed amendment to the GOP Senate's BCRAP bill is a big pile of crap all by itself, since it would effectively turn the ACA-compliant market into a massively underfunded High Risk Pool, while likely turning the non-compliant individual market into a wasteland of subprime junk insurance (or at best, plans which are reasonable right up until you get truly sick, in which case you're screwed).

To help explain how this would happen, I used this bar graph from the Kaiser Family Foundation to show how medical expenses are actually split up by different subsets of the population:

Based on these averages, I put together several scenarios showing what typical premiums might be for "ACA Enrollees" and "Cruz Enrollees" depending on how the market was split up:

Senate Majority Leader Mitch McConnell (R-KY) announced Tuesday that he is canceling half of Congress’ annual month-long August recess, keeping lawmakers in town to finish their drawn-out and so far unsuccessful effort to repeal the Affordable Care Act and tackle other pressing matters.

“Once the Senate completes its work on health care reform, we will turn to other important issues including the National Defense Authorization Act and the backlog of critical nominations,” he wrote.

Tensions are rising between Senate Majority Leader Mitch McConnell’s leadership team and his party’s ideological factions, with a renewed sense of pessimism creeping into the Senate GOP’s efforts to repeal Obamacare.

Fewer issuers apply to participate in Health Insurance Exchanges for 2018

Fewer issuers apply to participate in Health Insurance Exchanges for 2018

Less choice for consumers as issuer health plan applications drop 38 percent from last year

The Centers for Medicare & Medicaid Services (CMS) today announced 141 individual market qualified health plan (QHP) issuers submitted initial applications to offer coverage using the Federally-facilitated Exchange eligibility and enrollment platform in 2018. At the initial filing deadline last year, 227 issuers submitted an application compared to 141 this year, a 38 percent drop in filings.

Rhode Island just released their 2018 Individual and Small Group market rate hike requests, and they're pretty straightforward. For the small group market, I don't have the weighted market share for each carrier, but overall it ranges from 5.8 - 12.8%, with an unweighted average of 8.8%.

On the individual market, as with 2017, there's only two carriers participating in 2018: BCBS of RI and Neighborhood Health Plan. They're asking for a 13.8% and 5.0% increase respectively, with a weighted average of 10.5%.

BCBS gave their enrollment as around 27,000; for Neighborhood, I estimated theirs based on dividing their projected total member months by 12 to get 16,345. RI's on-exchange enrolment was 29,456 during Open Enrollment this year, so that would leave roughly 12,800 off-exhange enrollees, for roughly a 2:1 on/off-exchange ratio, which sounds about right.

Including Georgia, I've now compiled initial 2018 unsubsidized individual market rate hike requests for 17 states...and Georgia's carriers are asking for by far the highest overall average increase, even assuming no Trump/GOP sabotage tax.

There appear to be four carriers which have filed to sell individual market plans in Georgia next year: Alliant, Ambetter (aka Celtic, aka Centene...for God's sake, pick one name, guys, willya??), Anthem Blue Cross Blue Shield and Kaiser Health Plan.

His proposal, which he’s circulating to his colleagues on typed handouts, wouldn’t explicitly create and fund the special insurance markets, as the House bill did. Instead, insurance experts said, it would create a sort of de facto high risk pool, by encouraging customers with health problems to buy insurance in one market and those without illnesses to buy it in another.

...There is no public legislative language yet, but here’s how Mr. Cruz’s plan appears to work, based on his handout and statements: Any company that wanted to sell health insurance would be required to offer one plan that adhered to all the Obamacare rules, including its requirement that every customer be charged the same price. People would be eligible for government subsidies to help buy such plans, up to a certain level of income. But the companies would also be free to offer any other type of insurance they wanted, freed from Obamacare’s rules.

As longtime readers know, I've often separated the problems with the ACA into several categories:

Some were inherent in the original bill as signed into law.

Yes, many of these only exist because of futile attempts to win over support from Republicans (or a handful of blue dog Dems), but the Democrats are still responsible for them. This includes things like the APTC tax credits being too skimpy, the "family glitch", the "skinny ESI glitch" and so forth. In these cases, the GOP can certainly be criticized for refusing to help resolve those issues, but that's a matter of "passive" obstruction as opposed to overtly doing so.

Several regular commenters here at ACA Signups have been wondering why the Congressional Budget Office keeps using March 2016 as the "baseline" for projecting the net impact on healthcare coverage numbers under the GOP's Trumpcare bills (the House's AHCA and the Senate's BCRAP), as opposed to the more recent January 2017 baseline. After all, according to the March 2016 baseline, the CBO was projecting that under the ACA, the total individual market would have 25 million people as of 2026 (18 million on the exchanges plus another 7 million off-exchange), whereas under the January 2017 baseline, their projections are for the individual market to only be 20 million as of 2027 (13 million on the exchanges plus 7 million off-exchange). Taken at face value, this would seem to suggest a 5 million enrollee discrepancy. This drumbeat has been taken up more recently by GOP Senators, particularly Wisconsin Senator Ron Johnson.