In a year when every state's 2018 Open Enrollment situation is messy to say the least, Minnesota's is far more so:

Last year they were facing massive rate hikes, especially for unsubsidized enrollees (yeah, I know, I know, don't say it), and came very close to having all of their carriers bail

In response, they agreed to let most of them put a maximum enrollment cap on a First Come First Serve, with Blue Plus (BCBSMN) agreeing to take the "overflow".

However, the unsubsidized individual market enrollees were royally screwed, so the state legislature and governor slapped together a special, one-time 25% premium rebate specifically for them. The money came directly out of other portions of the state general fund, I believe. MNsure, the state exchange, also added an extra 8-day special enrollment period for these folks to jump in and get in on the rebate.

This got them over the 2017 hump, but clearly it was a sloppy, stopgap measure only, so earlier this year Minnesota decided to take advantage of the ACA's 1332 Waiver provision, which allows states to make significant changes to how they implement the ACA as long as the changes can be proven to provide at least as many people with similarly comprehensive coverage without increasing the federal deficit in the process...a provision which (former) HHS Secretary Tom Price encouraged states to do.

As for CSR payments not being made, however, the press release accompanying the rate tables was more vague; it stated that they would be "up to" 14 points higher, but didn't clarify whether that would apply to every individual plan or only the Silver policies, which is how most other states appear to be handling it. I assumed the "no-CSR" average would be roughly 32.9% if the load is only dumped on Silver plans, but 40.7% if spread across all metal levels.

Now that we've passed the 9/27 contract signing deadline for 2018 carrier participation on the ACA exchanges, the state insurance departments are posting their approved final rates pretty quickly. Arkansas has done a fantastic job of clearly laying out not just what the rate changes will be, but is explicitly stating how much of those increases are due to the GOP's refusal to formally appropriate CSR reimbursement payments next year:

Insurance companies offering individual and small group health insurance plans are required to file proposed rates with the Arkansas Insurance Department for review and approval before plans can be sold to consumers. The Department reviews rates to ensure that the plans are priced appropriately. Under Arkansas Law (Ark. Code Ann. § 23-79-110), the Commissioner shall disapprove a rate filing if he/she finds that the rate is not actuarially sound, is excessive, is inadequate, or is unfairly discriminatory. The Department relies on outside actuarial analysis by a member of the American Academy of Actuaries to help determine whether a rate filing is sound.

Insurance Commissioner approves rates insurers filed for 2018; Cost to cover CSRs has been added to silver plan premiums

On September 20, the Tennessee Department of Insurance and Commerce (TDIC) announced that the state had approved the rates that insurers had filed for 2018. However, the announcement indicated that Cigna’s approved average rate increase was 42.1 percent, which was based on the filing Cigna submitted in June 2017. An updated filing, with an average rate increase of 36.5 percent, was submitted in August, and TDIC confirmed by phone on September 21 that the updated filing was approved. The slightly smaller rate increase is due to Cigna’s decision to terminate some existing plans and replace them with new plans).

The following average rate increases were approved for 2018 individual market coverage:

In August I wrote that the situation in North Dakota was pretty straightforward: Three carriers on the individual exchange (BCBS, Medica and Sanford), requesting average rate hikes of around 24%, 19% and 12% respectively for an average increase of 23% assuming CSR payments are made, or a bit higher (28%) if they aren't.

Yesterday, however, with the final contract signing deadline having passed on the 27th, Louise Norris reports that one of the three carriers, Medica, was forced to drop out of the market at the last moment...not because they wanted to, but because the ND insurance dept. insisted on carriers pricing 2018 premiums on the assumption CSRs will be paid for the full year.

Medica understandably refused to take that risk (the odds of CSRs being guaranteed are virtually nil, and the odds of them being paid each and every month, as they're supposed to, is only so-so), so they dropped out instead.

Back in August, I reported that thanks to their just-approved federal reinsurance program, Alaska (which has only a single individual market carrier with the most expensive premiums in the country) is looking at an impressive 22% average decrease in their indy market premiums next year. However, that was based on the assumption that CSR reimbursement payments would not be made (or at least not guaranteed).

Alaskans buying health insurance on the individual market will see a decrease of 26.5 percent in rates next year, the sole insurer in the state announced Tuesday.

Alaskans had been paying some of the highest premiums in the nation.

More to the point, however: What other significance does not including CSR funding have?

Well, first of all, is it possible that they'll slip CSRs in before the vote? I suppose so, but consider this:

The final deadline for the insurance carriers to actually sign their contracts for 2018 is Sept. 27th, just 8 days from now.

The end of the 2017 fiscal year (i.e., the deadline for the GOP to try and cram through Graham-Cassidy with only 50 Senate votes) is Sept. 30th.

The CBO is "aiming" to provide a "preliminary assessment" of Graham-Cassidy "early next week" which I presume means Monday the 25th or Tuesday the 26th.

I assume the other steps (parlimentary ruling, vote-a-rama, etc) would take place on Wednesday the 27th, the same day the contracts have to be signed.

Yom Kippur is the evening of the 29th, running through Saturday the 30th. I can't imagine even McConnell would be that much of a dick to schedule the vote then.

That leaves Thursday the 28th or Friday the 29th for the actual vote itself.

That's a day or two after the carrier contracts have been signed.

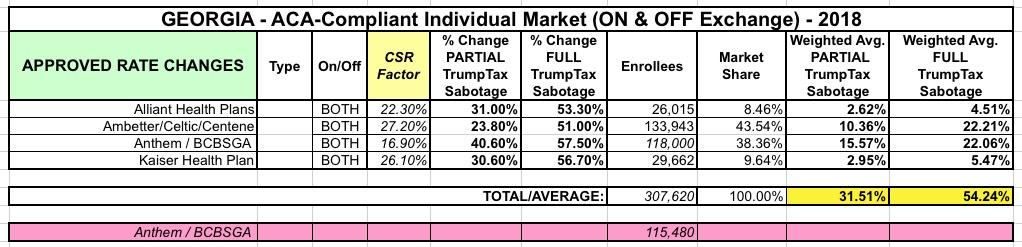

INSURANCE DEPARTMENT RELEASES PROPOSED RATES FOR 2018 HEALTHCARE EXCHANGE

Atlanta – Insurance Commissioner Ralph Hudgens announced today that his office had submitted proposed 2018 health insurance rates to the Centers for Medicare and Medicaid Services (CMS) for the federally-facilitated Healthcare Exchange for final federal approval.

“Today my office submitted 2018 Obamacare rates to Washington D.C. for approval,” Hudgens said. “In its fifth year, Obamacare has become even more unaffordable for Georgia’s middle class with potential premium increases up to 57.5 percent. I am disappointed by reports that the latest Obamacare repeal has stalled once again and urge Congress to take action to end this failed health insurance experiment.”

More to the point, however: What other significance does not including CSR funding have?

...That means that even if there's a last minute change to the bill, at this point, CSR payments are virtually certain not be guaranteed next year.

...I wouldn't be at all surprised to see more 11th-hour drop-outs next week. Donald Trump and the Republican Party's open sabotage of the ACA will likely bear even more fruit.

Anthem leaving Maine ACA marketplace, citing uncertainty

Anthem Blue Cross Blue Shield has withdrawn nearly all of its offerings from Maine’s Affordable Care Act health insurance marketplace, and the insurer is citing market uncertainty and volatility as the reasons.

{kind=link}