I've spent the past two weeks posting about almost nothing besides the Graham-Cassidy debacle, so haven't had a chance to keep on top of the approved 2018 rate changes as I usually do. Fortunately, Louise Norris of healthinsurance.org has stayed on the rate hike job, and reports the final numbers out of Washington State:

2018 rates: 24% approved rate increase, due in large part to federal uncertainty — and higher backup rates will be implemented if CSR funding is cut mid-year

Insurers in Washington had to file rates and plans for 2018 by June 7, 2017. On June 8, Kreidler’s office published a summary of what had been filed (rate filings are available here, and that page will show final rate changes for the individual market once they’re approved), and publicized the filing details on June 19. The average proposed rate increase in Washington, before any subsidies are applied, was 22.3 percent.

Back in August it looked as though Florida carriers were looking at either 15.5% unsubsidized rate increases on the individual market if CSR reimbursement payments were guaranteed next year, or around 35.5% if they weren't. Well, the official rates have been released by the Florida Dept. of Insurance, and it's even uglier than that for unsubsidized enrollees:

Office Announces Submission of Proposed Rates for 2018 Federal PPACA Health Insurance Plans

Republican leaders have decided not to vote on Obamacare repeal legislation this week, effectively ending the party’s latest effort to wipe away the 2010 health care law.

When, and whether, they will try again remains to be seen. But for now, a defining cause of the Republican Party, including President Donald Trump, lies in tatters.

And at least for the moment, insurance coverage for many millions of Americans who rely on Medicaid or the Affordable Care Act’s federal subsidies remains intact ― although insurance markets in some states remain unstable, and the Trump administration’s willingness to manage the program remains unclear.

(sigh) When I last checked in on Virginia, things were looking up a bit (relatively speaking), as Anthem Blue Cross Blue Shield (aka "HealthKeepers") had announced that they were jumping back into the state in order to cover the 60-odd counties which would otherwise be left bare by Optima Health Insurance dropping out of half the state a week or so earlier.

As many see their options for health plans dwindle down to one insurer, premiums are simultaneously set to rise by an average of 57.7 percent next year in Virginia’s individual marketplace.

The increase is “unquestionably the highest we’ve ever seen,” David Shea, health actuary with Virginia’s Bureau of Insurance, told lawmakers Monday.

Yesterday was a Graham-Cassidy (or "Grassidy", as former CMS Administrator Andy Slavitt keeps trying to push) Fest, with all sorts of Grassidy-centric happenings, including the one-and-only Senate hearing on the bill; the Congressional Budget Office releasing their preliminary/partial score of G-C (the prior version, not the later version); Senator Susan Collins releasing her statement opposing the bill; and last night's CNN healthcare debate between Senators Graham & Cassidy vs. Senators Sanders and Klobucher. I might write something about these items later today, but right now I want to look at another development.

Last week I broke the story (later picked up by Axios, NY Magazine and Vox.com) that the Graham-Cassidy bill would make thousands of current insurance policies illegal starting on January 1, 2018...just 98 days from now.

Why? Because, as noted at the link, while the current ACA structure (exchanges, tax credits, etc) would stay mostly in place for 2 more years, some provisions would be repealed immediately...including a nationwide ban on any exchange policy offering abortion coverage.

This morning JP Massar (who called my attention to the 1/1/18 effective date the first time) inquired as to whether that had changed with the new version of G-C. As you can see on pages 2 & 3 of the new bill...nope. It’s still in place.

Here's direct links to the bill itself and to the GOP's table showing what they claim would be the net federal funding changes from 2020-2026 for each state relative to current law...but they pulled one hell of a fast one.

it's pretty rare for the entire medical, hospital and insurance industry to agree on just about anything...and yet here we are (emphasis in the original):

The following statement was jointly released on September 23, 2017 by the American Medical Association, American Academy of Family Physicians, American Hospital Association, Federation of American Hospitals, America's Health Insurance Plans and the BlueCross BlueShield Association regarding the Graham-Cassidy-Heller-Johnson legislation.

We represent the nation's doctors, hospitals and health plans. Collectively, our organizations include hundreds of thousands of individual physicians, thousands of hospitals, and hundreds of health plans that serve tens of millions of American patients, consumers and employers every day across the United States.

Anyone who's followed me either here at ACASignups.net or over at Twitter over the past eight months knows that no one has been sounding the alarm louder or more frequently than me about both the real and potential sabotage of the ACA being carried out (or at least attempted) by the GOP in general and Donald Trump/Tom Price specifically. Hell, back in July, I even warned of a half-dozen things to look out for, several of which have since already been proven true:

This brings me to the main point of this entry: This is likely just the beginning. I'm not going to say that any or all of the following will happen--it's possible that Trump/Price/Verma will show some level of restraint--but I wouldn't be at all surprised to see any or all of these happen during this fall's Open Enrollment Period (which runs from Nov. 1st - Dec. 15th, by the way):

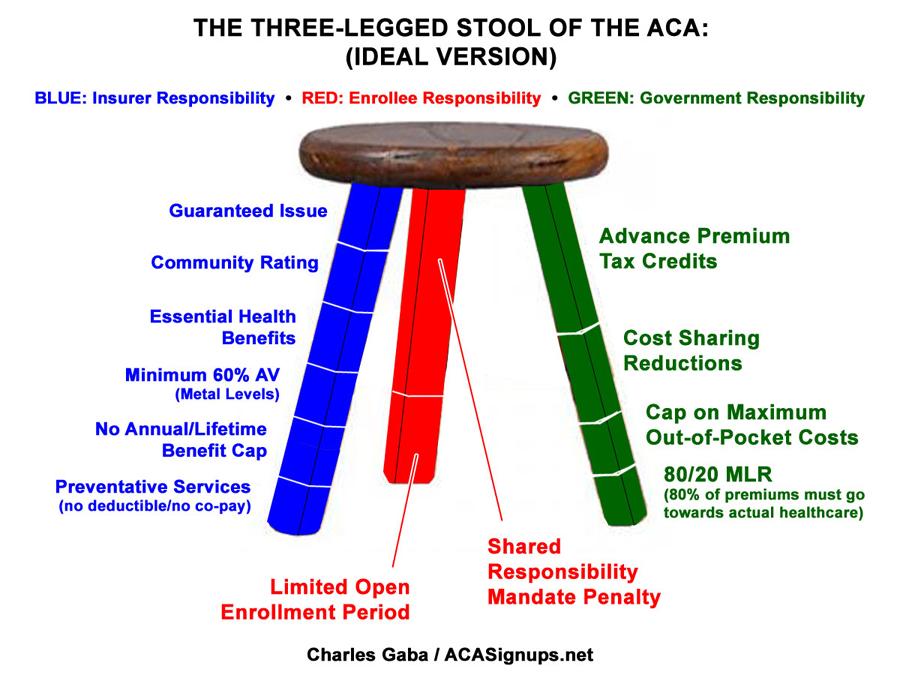

It's time to once again dust off the Three-Legged Stool visual aid to help explain just what the Graham-Cassidy bill would do to the individual insurance market. It's important to note that none of this has anything to do with Medicaid (expansion or traditional), the group market, Medicare and so forth; just the individual market.

Once again, here's what the "3-Legged Stool" was supposed to look like under the Affordable Care Act:

Here's what it actually looks like today, with some rather obvious gaps in the red (enrollee responsibility) and green (government responsibility) legs: