Kaiser: YAY: 90% of ACA enrollees will stick around post-mandate! BOO: But about the 7% who won't...

Tue, 04/03/2018 - 12:24pm

The Kaiser Family Foundation runs a widely-respected monthly natonal tracking poll about healthcare issues. The questions they ask sometimes change from month to month, and this month they asked a whole bunch of questions about...the Individual Market and the ACA exchanges. In other words, pretty much a bonanza of data-nuggety goodness for this site:

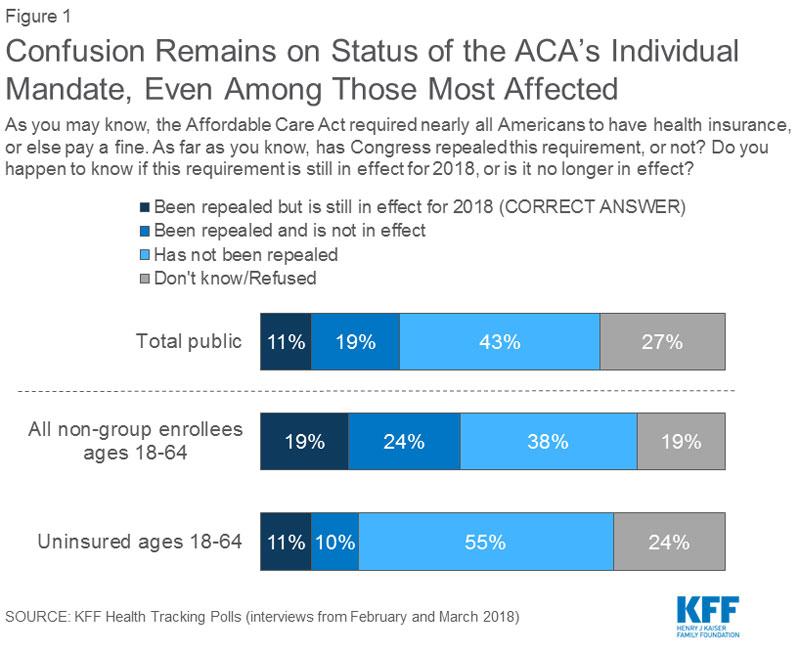

- As part of the Republican tax reform plan signed into law at the end of 2017, lawmakers eliminated the ACA’s individual mandate penalty starting in 2019. About one-fifth of non-group enrollees (19 percent) are aware the mandate penalty has been repealed but is still in effect for this year. Regardless of the lack of awareness, nine in ten non-group enrollees say they intend to continue to buy their own insurance even with the repeal of the individual mandate. About one-third (34 percent) say the mandate was a “major reason” why they chose to buy insurance.

- About half the public overall believes the ACA marketplaces are “collapsing,” including six in ten of those with coverage purchased through these marketplaces. In fact, across party identification and insurance type, more say the marketplaces are “collapsing” than say the marketplaces are not collapsing.

- Overall, the population who buy their insurance through the ACA marketplace report being satisfied with the insurance options available to them during the most recent open enrollment period and more than half give the value of their insurance a positive rating. Yet, some (32 percent) experienced problems while trying to renew or buy their coverage and six in ten marketplace enrollees say they are worried about the possible lack of health insurance coverage in their areas.

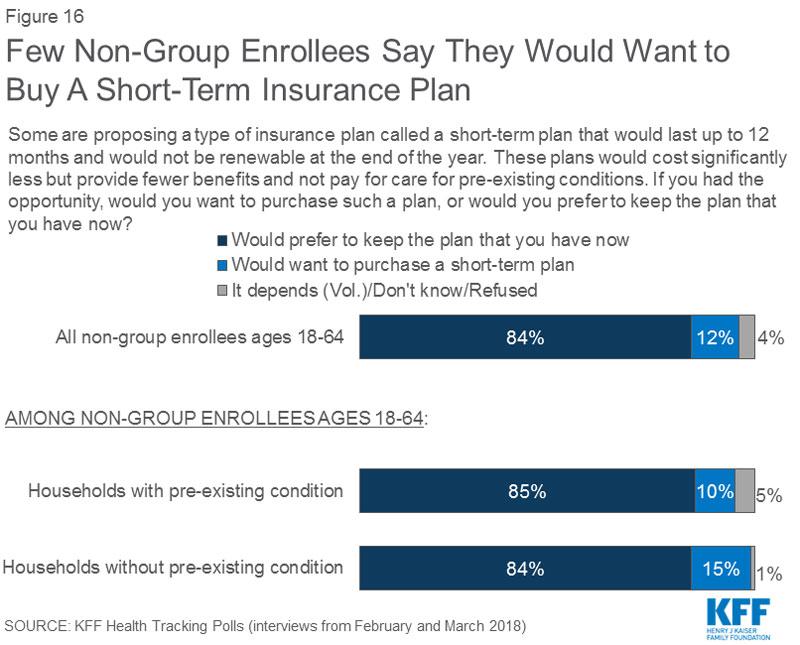

- In 2017, President Trump issued an executive order directing his administration to expand the availability of non-renewable short-term insurance plans, and regulations have been proposed to implement the order. When asked whether non-group enrollees would prefer to purchase such a plan or prefer to keep the plan they have now, the vast majority (84 percent) say they would keep the plan they have now while 12 percent say they would want to purchase a short-term plan.

- The most common response offered by people who are uninsured when asked the reason why they don’t have health insurance is that it is too expensive and they can’t afford it (36 percent), followed by job-related issues such as unemployment or their employer doesn’t offer health insurance (20 percent).

The first thing I looked at, before even checking out the questions and responses, was the methodology. KFF is very, very good at this sort of thing, so I wasn't disappointed:

This survey was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). Interviews were conducted by telephone from February 15th -20th and March 8th -13th, 2018, among a nationally representative random digit dial telephone sample of 2,534 adult U.S. residents.

Note that children aren't included because (I presume) they can't be legally included in telephone surveys. This is important to keep in mind with Gallup surveys as well: When they report on the uninsured rate, it doesn't include about ~24% of the population. Since children always have a much higher healthcare coverage rate than adults, it skews the results quite a bit.

One important thing to keep in mind: The total sample is quite large (over 2,500 people) and thus has a very low margin of error (+/- 2 points), but the individual market is such a tiny slice of the population (perhaps 5% or so...around 16 million, give or take), the sub-category sample has a much larger margin of error (+/- 7 points)...and that's after basically doubling the individual market sample size:

Sixty-six percent of non-group enrollees in this survey are marketplace enrollees.

The numbers above actually show it as 63%, but the larger point is that the off-exchange market is included in roughly the correct proportions: Around 10 million exchange-based enrollees and around 6 million in off-exchange plans. This is really important...but also sets up the missing question, which I'll get to below.

OK, into the weeds:

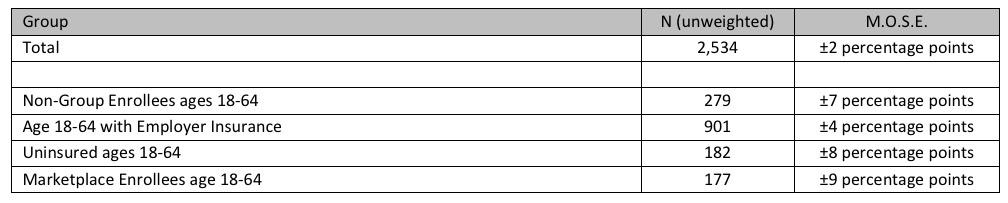

Yup. Sure enough, only 11% of the population understands exactly what happened with the individual mandate back in December. To be honest, 43% not knowing that the mandate has been repealed is actually a good thing, since the point of the mandate in the first place wasn't to punish people but to encourage them to actually get covered (not just for their sake but also to help keep the risk pool healthier). The ones who are are in for a rude awakening right about now are the 19% who think that the ACA individual mandate has already become null and void. Many of them are in the middle of filing their federal income tax forms for 2017 thinking that they're off the hook only to discover that nope, they still have to pay the penalty for not being covered last year. This same scenario will play itself out again a year from now (presumably for a smaller number of people) when those who didn't #GetCovered for 2018 file their taxes in spring 2019.

Now that Kaiser has explained the mandate repeal situation, how will that impact people's decision about whether to enroll in ACA-compliant coverage next year (which is the critical point)?

On the surface, this doesn't sound too bad. Fully 90% of those currently enrolled in the individual market plan on sticking around, while only 7% say they'd drop coverage (the other 3% either hadn't decided or refused the question)...that amounts to perhaps 1.1 million people dropping coverage nationally. Not good, but not horrible, right? Llet's suppose this is representative and no one changes their answer this fall: Around 14.5 million indy market enrollees renew their ACA coverage, with only about 1.1 million dropping out of the market. Why is that worse than it sounds?

Here's why: The odds are extremely high that just about all of those ~1.1 million are not only gonna be unsubsidized (no financial assistance to cushion the blow)...but they're extremely likely to be fairly healthy, because anyone with an expensive ailment/condition is gonna think twice before going without coverage.

That means the remaining risk pool isn't just gonna be 7% smaller...it's likely to be a whole lot sicker on average. Which, again, means more premium hikes, which make the remaining healthy people that much more likely to drop out and so on.

This is precisely why the CBO is projecting a ~10% unsubsidized rate increase on the individual market next year: Without the premium revenue from those 7% who cost so little to cover, carriers will have far less revenue to spread out across the 90% who stick around and will have to raise rates accordingly.

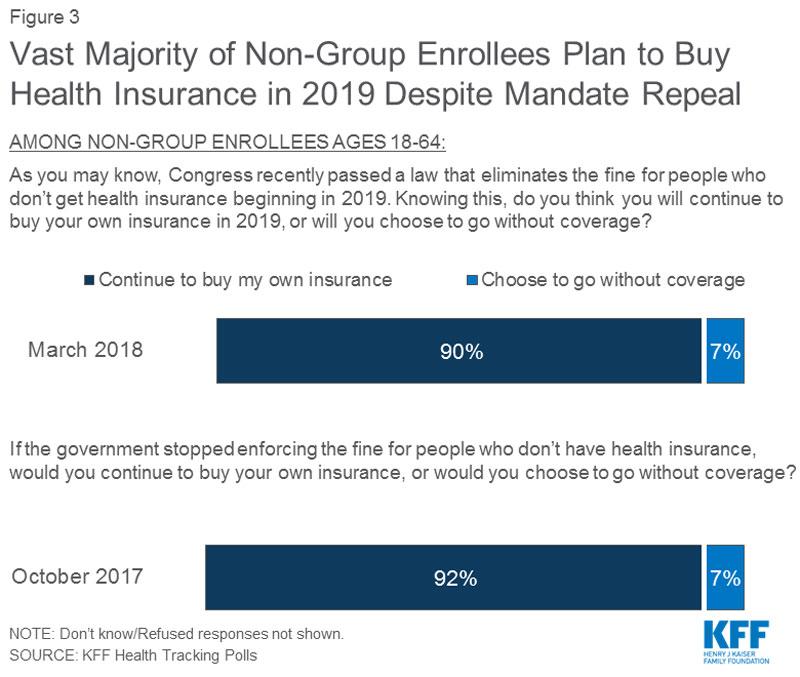

I'm skipping over a bunch of questions to this one, about net premiums. This is where the ACA's tax credits, CSR assistance, the 400% FPL cut-off for tax credits and last fall's Silver Loading/Silver Switching come into play:

The good news is that 3/4 of marketplace enrollees (that is, exchange-based enrollees) saw their net premiums either stay the same, only go up slightly or even drop (thanks to Silver Loading, Silver Switching and--in Alaska and Minnesota--a state-based reinsurance program). By a similar token, fully 78% of exchange-based enrollees saw their deductibles stay around the same or even drop. Awesome.

UNFORTUNATELY, the other 25% of exchange enrollees saw their premiums jump quite a bit, and 21% saw significantly higher deductibles. And remember, these are for the exchange-based population only. It's likely that these percentages are much higher for the off-exchange population.

Assuming nearly all off-exchange enrollees saw both premiums and deductibles jump, that would mean around 50% of individual market enrollees saw big jumps in both premiums and deductibles. THAT'S where the problem has been for years. It was made far worse this year due to various deliberate sabotage moves by the Trump Administration (CSR cut-off, half-length enrollment period, 90% marketing cuts, etc), and is gonna be far worse still in 2019 due to the mandate cut-off, #ShortAssPlans and so on.

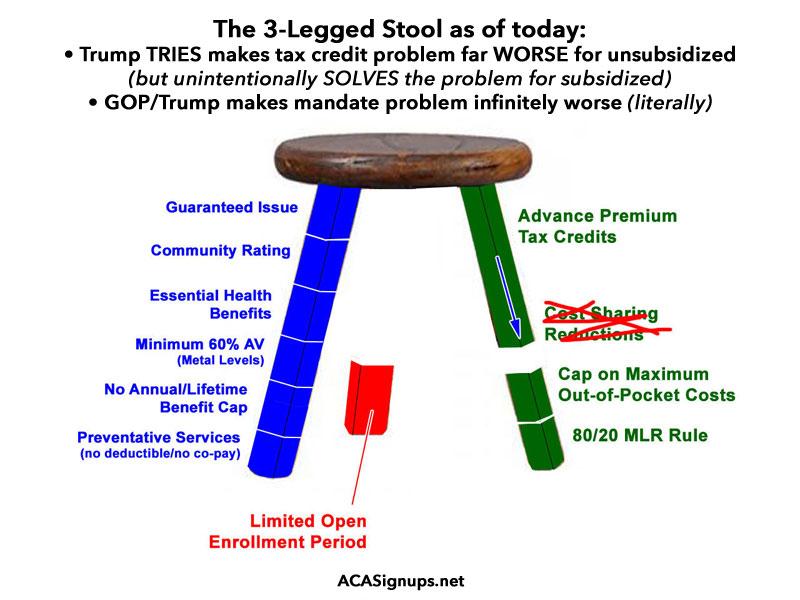

Here's an interesting question which cuts to the heart of the "3-Legged Stool" model of the ACA, and raises the spectre of the classic saying, "Everyone wants to go to heave but no one wants to die"...

The ACA mandates that insurance carriers include all of the stuff in the blue leg below--guaranteed issue, community rating, essential benefits and so on. Since requiring all that stuff raises the cost of the policy considerably, it also provides financial assistance and other cost-limiting provisions (the green leg) to ensure most people can afford the policies. Finally, it added a mandate penalty to help urge people to actually sign up, to keep the risk pool from getting worse and spiraling costs out of control (the red leg). The GOP, of course, tore away the red leg last December, effective starting in 2019.

The GOP "solution" to a problem which was already real for some people and which they've deliberately made far, far worse over the past year or so is to "cut costs" by simply hacking away at the blue leg as well. That was the centerpiece of nearly every "repeal/replace" bill they tried to push through last year, and is also at the heart of every type of regulatory garbage Trump is pushing this year--"Short-Term Plans", "Association Plans", expansion of "Health Sharing Ministries", as well as the state-initiated stunts being pulled by Idaho (which was thankfully stopped) and Iowa (which unfortunately appears to be going through).

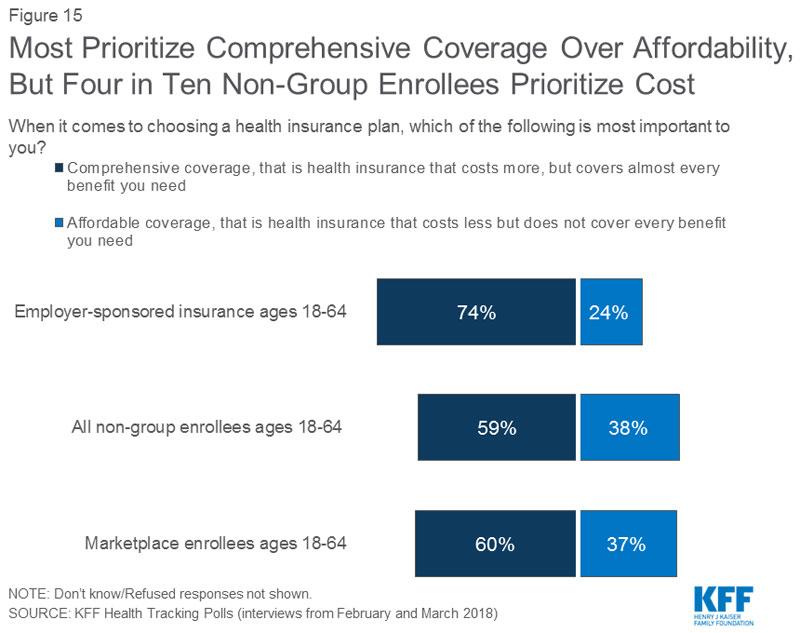

In all of these cases, the whole point is to once again start offering policies which remove some or all of the blue leg to "keep costs down"...except the Kaiser poll clearly shows that 3/4 of those on employer plans value comprehensive coverage over cost savings (easier for them to say...most of their premium is paid for by their employers anyway), while 60% of individual market enrollees do.

I'm willing to bet that the 60% who value coverage over cost line up pretty closely with the 60% who...receive federal tax credit subsidies.

And therein lies the problem: If you're subsidized, cost isn't nearly as much of a problem, so you're not gonna want to lose any of the benefits. If you're unsubsidized, you have to pay the full amount, so you're gonna want to try and cut costs wherever possible...except that doing so a) leaves you vulnerable to economic catastrophe and b) damages the risk pool overall. That's what you're seeing play out at the state level right now.

Speaking of which, finally, how much of a threat is Trump's #ShortAssPlan sabotage? Well, they didn't ask about "Association" plans, but they did ask about Short-Term Plans:

Again, on the surface this looks like relatively good news: The vast majority of individual market enrollees would not be enticed to drop their exchange plans and move to a year-round "short-term" (complete oxymoron at 364 days per year) non-ACA compliant policy.

The problem, once again, is that around 12% of them--perhaps 1.9 million people--would strongly consider doing exactly that...and guess who those 1.9 million would be? That's right: For the most part they'd be unsubsidized, currently healthy enrollees. Basically the same 7% mentioned above plus another 5%, give or take.

No matter how you slice it, without the right type of significant legislative action at either the federal or state levels (that is, action which strengthens the ACA-compliant market as opposed to tearing it down as Trump/GOP actions have been), the 2019 Open Enrollment Period ain't gonna be pretty.

Advertisement