Massachusetts: Preliminary unsubsidized avg. 2024 #ACA rate changes: +3.7% (fully weighted, merged market)

Wed, 08/09/2023 - 8:34pm

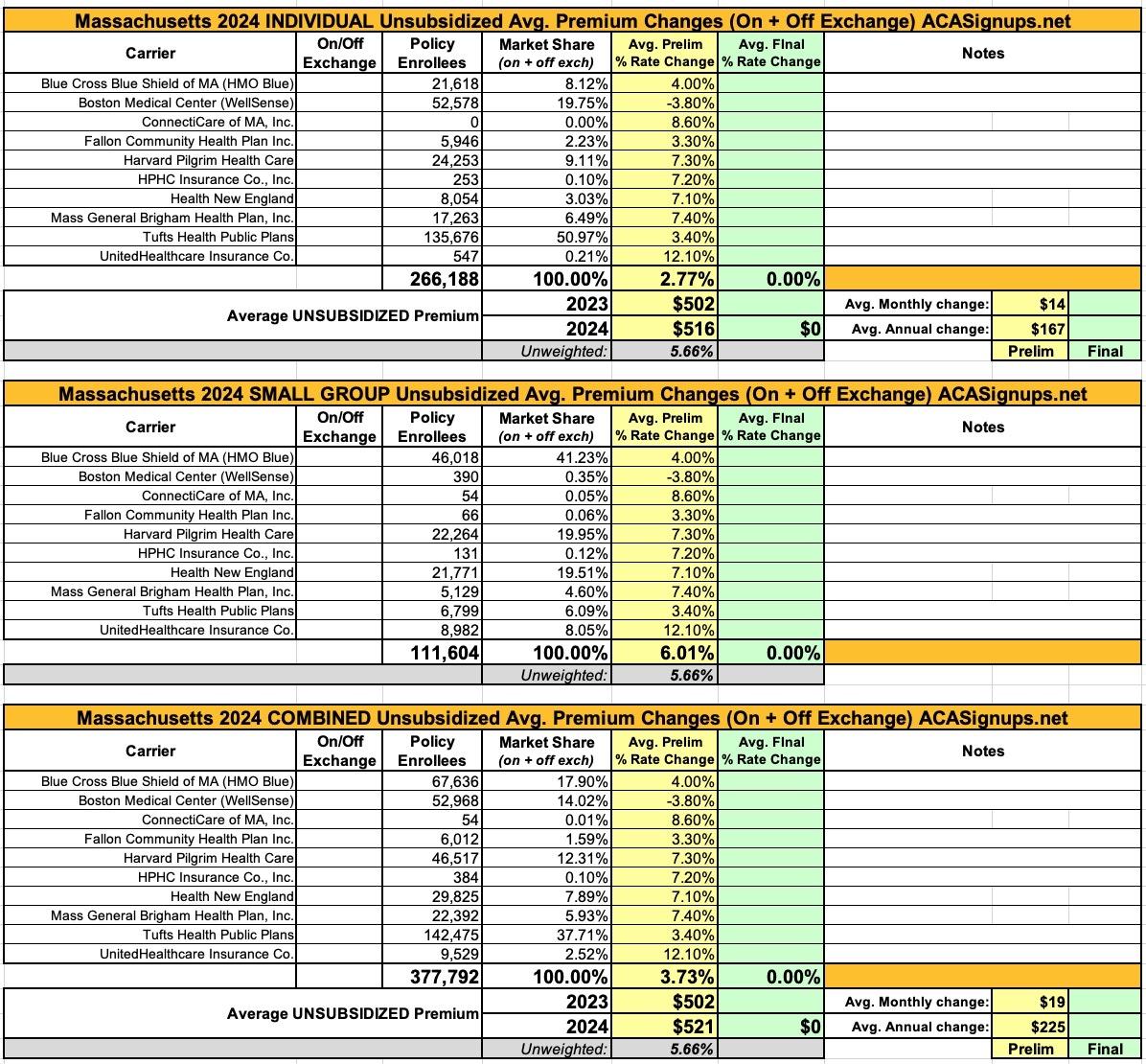

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has 10 different carriers participating in the individual market.

One thing which sets Massachusetts (along with Vermont) apart from every other state is that their Individual and Small Group risk pools are merged for premium setting purposes.

Normally you would think this would make my job easier, since I only have to run one set of analysis instead of two...but until recently, it was surprisingly difficult to get ahold of exact enrollment data for each carrier on the merged Massachusetts market (and even more difficult to break out how many are enrolled in each market since they're merged...not that that's relevant to the actual rate changes).

Fortunately, for 2024 at least, there's a fully-detailed breakout of all of this, including the filings, public narrative/justifications, actuarial memos and so on...and even a breakout of how many enrollees are in the individual vs. small group market policies!

It's possible that this detailed breakout has been available all along and I just didn't find it until now, but regardless, it makes my data nerd heart sing to see it!

I've broken the data out into the three tables below. The list of carriers and requested rate changes are the same for all three, but the first only includes individual market enrollees, the second only includes small group market enrollees, and the third is the combined, fully weighted average (which is the key number to use for my purposes).

Overall, Massachusetts has around 266,000 indy market enrollees and another 111,000 residents in small group plans. The combined, weighted average rate increase the carriers are seeking is just 3.7%, which is pretty nominal compared to many other states this year.

It's also worth noting that ~225,000 Bay Staters signed up for exchange-based individual market plans during Open Enrollment last fall. Assuming a ~10% net attrition by March 2023, that means MA's off-exchange indy market is around 63,000 people.

From some of the consumer summaries:

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

- Health insurance premiums reflect the cost and usage of medical care and services. Health New England (HNE) has been impacted by increases in these areas due to higher costs for medical services and prescription drugs and costs related to the ongoing ripple effects of COVID-19. As a result, our medical and pharmacy trends, used in premium rate development to project costs for inpatient and outpatient hospital-based care, physician services, and prescription drug costs, continue to rise.

- The largest driver of HNE’s 2024 requested rate increase is a rise in the costs of medical services and drugs. Pharmacy costs are expected to increase by 8% in 2024. This increase is tied to a number of new high-cost therapies. Members are also expected to use 4% more prescription drugs in 2024.

- Physicians and hospitals are facing economic pressures caused by supply chain shortages, overall inflation and continued workforce challenges. As a result, providers are seeking higher reimbursement for their services. HNE is routinely required to increase service reimbursement rates at levels that exceed the 3.6% cost control benchmark, established by the MA Health Policy Commission, in order to maintain its robust provider network.

- Hospital services are expected to be 5.1% more expensive in 2024 and the use of those services is expected to grow 2-3%. Both the increase in cost and utilization are in part caused by members deferring care during the COVID-19 pandemic. The delay in care resulted in increased severity of conditions and a growing need for intense treatments.

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

Mass General Brigham Health Plan’s proposed rate filing for 2024 reflects anticipated, industry-wide increases in the cost and utilization of healthcare services, and investments in strategic initiatives that expand access to high-quality healthcare for our members. The market factors that impacted our rate filing include:

- A challenging operating environment for providers due to rising labor costs, capacity challenges and inflation, which are creating upward pressure on commercial reimbursement rates.

- An uptick in the utilization of services, especially for outpatient and specialty pharmacy services.

- Additional costs associated with changes in mix of services, new-to-market therapies and higher patient acuity due to the deferment of care during the COVID-19 pandemic.

- New government requirements for products and rating.

Additionally, our rate filing incorporates continued investments in mental healthcare with the launch of an innovative new network solution that has sped access to essential mental health services.

The rate change is being offset by efforts developed to manage costs. These include pharmacy and care management services initiatives, and product designs that improves affordability by encouraging care delivery in appropriate settings.

KEY DRIVERS FOR THE PROPOSED RATE CHANGE

- Trend: A key driver of health insurance premium increases year-over-year is medical trend, which is comprised of inpatient, outpatient, and physician services as well as pharmacy costs. Medical trend includes both increases in the cost of the services provided by hospitals and physician groups and increases in the utilization of these services by our members. In particular, increased pressure on unit cost trend and inflation, as well as continuing high pharmacy costs, drive year-over-year trend increases in medical expense.

- Morbidity: In addition to trend, Tufts Health has considered the expected cost change related to the migration of members from MassHealth to the Merged Market following the end of the Public Health Emergency in Massachusetts. In doing so, we have reviewed the average cost within the Tufts Health Direct population prior to the pandemic and subsequent exit of members into the MassHealth program, as well as other studies to determine the how the migration of members from MassHealth will impact the overall cost of the Tufts Health Direct market in 2023 and 2024.

- Risk adjustment: While there is expected to be a migration of members from MassHealth to the Merged Market due to redetermination, also taken into account were changes in the overall member mix within the merged market and expectations for Tufts Health member risk relative to the overall market for 2024. These changes are expected to decrease the Tuft Health Direct risk transfer payment as an offset to the morbidity adjustment as described above.

- Contribution to Surplus: THPP includes a surplus of 1.9% in order to maintain financial stability and ensure that Tufts Health Public Plans can continue to pay claims 2 and invest in its members, despite the significant uncertainty that is present in the market and healthcare industry.

Advertisement