Vermont: Final avg. unsubsidized 2024 #ACA rate change: +13.0%

Mon, 08/28/2023 - 3:49pm

Every year, I spend months painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need. The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier:

- How many effectuated enrollees they have in ACA-compliant individual market policies;

- The average projected premium rate change for those enrollees (assuming 100% of them renew their existing policies, of course); and

- Ideally, a breakout of the reasons behind those rate changes, since there's usually more than one.

Unfortunately, there are numerous states where due to the carriers and/or the state insurance departments heavily redacting the rate filing documentation, I've been unable to fill in the actual number of people enrolled by some or all of the insurance carriers within that state's individual market. In these cases, the average premium rate changes listed (shown in grey) are unweighted averages, not weighted.

This can make a big difference in some cases: Let's say you have 2 carriers in a state, one raising rates by 10% and the other raising them by 1%. The unweighted average increase would be 5.5%. However, what if it turns out that the first carrier has 90% of the market share while the second only has 10%? That would mean a weighted average increase 9.1%. The unweighted average is the best I can do for these states without knowing the market share breakout, however.

With that in mind...

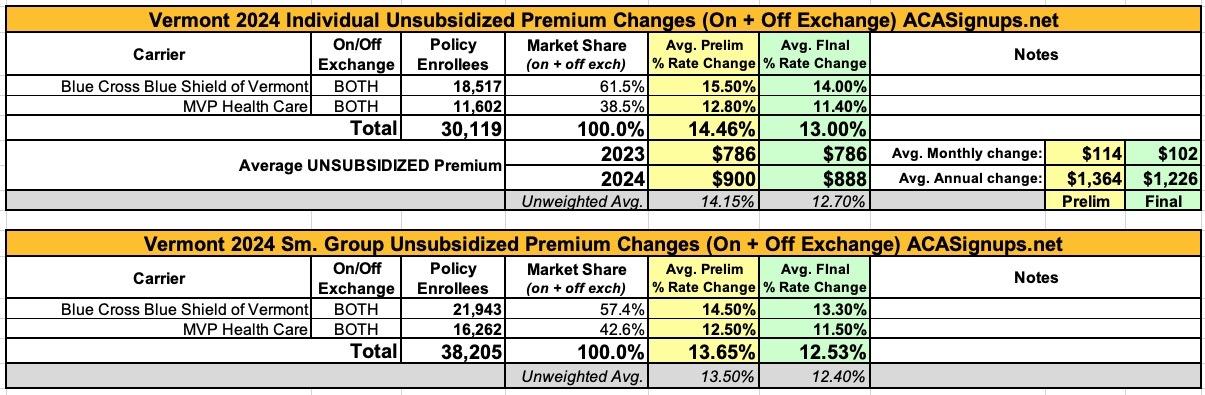

Back in May, Vermont was the first state to publicly post their preliminary annual rate filings for the individual & small group markets. Vermont's filings are pretty easy to average because a) they don't redact any of their filing data; b) they make the forms easy to access; and c) they only have two insurance carriers operating in the individual or small group markets anyway (in fact, it's the same two carriers in both markets).

Here's what VT's final, approved 2024 filings look like. On average, the two carriers (Blue Cross Blue Shield and MVP) will be seeing rate increases of 13.0% increases for individual market premiums and 12.5% for small group plans:

GREEN MOUNTAIN CARE BOARD CUTS 2024 HEALTH INSURANCE RATE REQUESTS FOR SMALL GROUP AND INDIVIDUAL & FAMILY PLANS

Montpelier, VT – The Green Mountain Care Board (GMCB) issued decisions requiring Blue Cross Blue Shield of Vermont (BCBSVT) and MVP Health Plan, Inc. (MVP) to modify the premiums they wanted to charge individuals and small businesses for health insurance plans in 2024. In 2023, these plans covered just over 68,000 Vermonters.

The premium increases requested by BCBSVT and MVP were driven by a number of factors, including increases in hospital and prescription drug costs. During GMCB’s review of the requests, BCBSVT and MVP raised their proposed rates in response to new information. In evaluating the requests, GMCB reviewed and considered a variety of data, including the opinions of its actuaries and the Department of Financial Regulation and data presented by the insurers and the Office of the Health Care Advocate. GMCB also received 147 written public comments and heard from Vermonters at a public comment forum on July 24.

“While we were able to reduce these rate requests, we know that Vermonters will still struggle to pay for their health care. The GMCB is currently reviewing hospital budgets, a key driver in health care cost increases. We will continue to use every tool we have to improve affordability and increase access to high quality health care for Vermonters.” Owen Foster, GMCB Chair

It's important to note that 88% of exchange-based individual market enrollees are subsidized in Vermont (around 73% of the total individual market). It's also worth noting that while a 13% rate increase isn't pretty, at least state regulators shaved it down a bit from the 14.5% requested by the carriers.

Advertisement