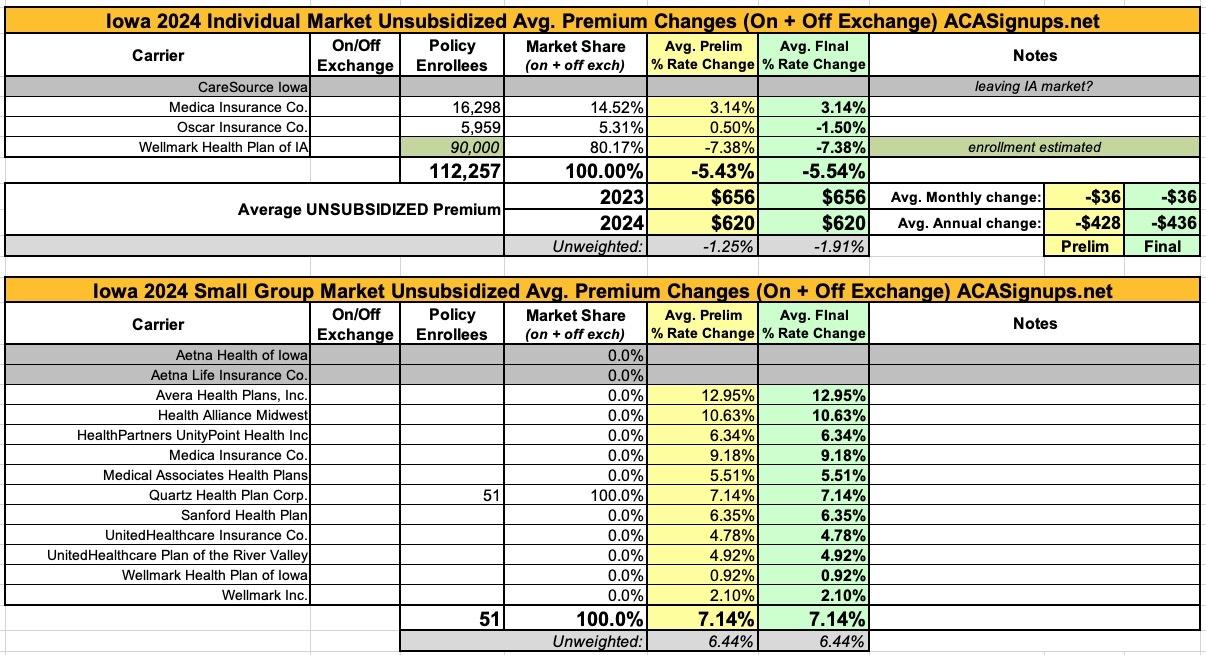

Iowa: *Final* avg. unsubsidized 2024 #ACA rate changes: -5.5%

Fri, 11/03/2023 - 3:07pm

Originally posted 8/08/23; updated 11/03/23

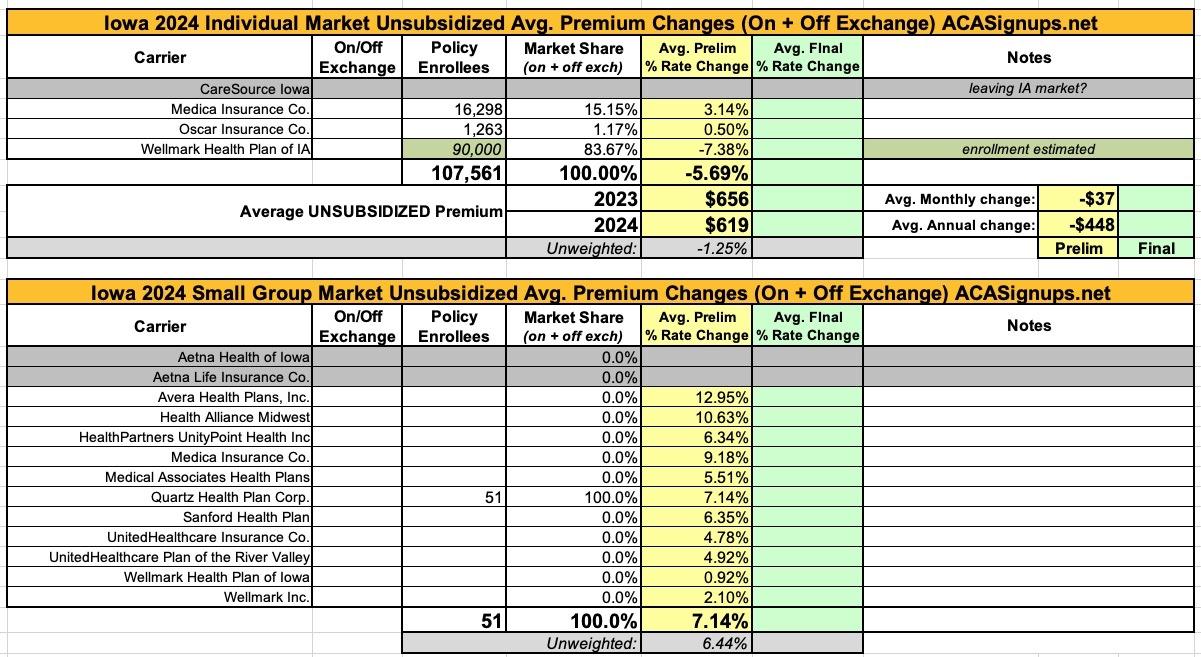

Here's the preliminary 2024 rate filings for Iowa's individual & small-group markets. Unfortunately, I only have the enrollment data for the two smaller carriers on the individual market (and for only one carrier on the small group market). Oddly, while the Iowa Insurance Dept. has detailed rate filings for Medica and Oscar, it doesn't have one for Wellmark posted...and on the small group market, they only have publicly-available filing documentation for two of the eleven carriers.

Interestingly, CareSource Iowa, which only joined the state's individual market this year, appears to be dropping out of it again in 2024...or at least they don't have a listing showing up at RateReview.HealthCare.Gov as of this writing. Similarly, Aetna seems to be dropping out of the small group market as well.

In any event, based on my estimate of Iowa's total ACA-compliant individual market, I can make an educated guess as to the former's weighted average, which should be roughly a 5.7% drop in premiums.

Unfortunately I can't do the same for the small group market; for that, the unweighted average rate increase is around a 6.4% increase.

UPDATE 11/03/23: The final/approved rates have been posted to the federal rate review database; not much has changed beyond Oscar's indy market premiums being cut by 1.5% instead of 0.5%.

{kind=link}

1) Scope and Range of Rate Increase

Medica Insurance Company (Medica) is requesting a rate change for its individual market business in Iowa. The rate change will take effect on January 1, 2024 and will impact an estimated 16,298 members. The average rate change by product will range from 2.0% to 7.1% and will result in rate changes that vary across plan designs, with zero plans that will be higher than 15% rate changes.

2) Financial Experience of the Product

Medica’s loss ratio has improved in 2022, allowing Medica to request a smaller rate increase than for 2023. The requested rate increase is meant to reset Medica’s revenue to a sustainable level and also to moderate future rate increases.

3) Changes in Medical Service Costs

Medical inflation, in both utilization and costs of services, is the main driver of Medica’s rate increase. Annual increases in medical services and drug costs both contribute significantly to medical inflation.

4) Changes in Benefits

Medica continues to try to maintain a competitive portfolio of plans, and the majority of changes to the plan designs are due to federal regulations around plan richness, i.e. metal levels. This caused a few plan designs to have higher rate increases than others.

5) Administrative Costs and Anticipated Margins

The main drivers of Medica’s administrative expenses are employee salaries and benefits, agent commissions, claim processing, premium taxes, licenses and fees, and taxes and fees required by the ACA. Medica strives to lower its administrative expenses as well as underlying cost of care to improve its ability to keep rates as low as possible.

1. Scope and Range of Rate Increase

The purpose of this document is to present rate change justification for Oscar Insurance Company’s (Oscar’s) Individual Affordable Care Act (ACA) products, with an effective date of January 1, 2024, and to comply with the requirements of Section 2794 of the Public Health Service Act as added by Section 1003 of the Patient Protection and Affordable Care Act (ACA). Using in-force business as of May 31th, 2023 , the proposed average rate increase for renewing plans is -1.5%. Rate increases vary by plan and range from -7.0% to 10.0% due to a combination of factors including shifts in benefit leveraging, cost-sharing modifications, and geographic rating factors. This rate increase is absent of rate changes due to attained age. There are 1,263 current members impacted by a rate increase greater than 5.1%.

2. Financial Experience of the Product

To rate 2024 premiums, Oscar used a blend of 2022 Iowa experience and our Manual rating rating methodology. Oscar’s projected loss ratio for 2024 is 84.5%, which is above the federally mandated loss ratio of 80%.

3. Reason for Rate Increase(s)

- Medicaid Redetermination Oscar anticipates increases to the market morbidity in Iowa due to the ending of the Public Health Emergency Emergency and a proportion of Medicaid Redeterminations enrolling in the ACA Marketplace in the 2023 and 2024 plan years.

- Changes in Medical Service Costs The projected premium rates reflect the most recent emerging experience which was trended for anticipated changes due to medical and prescription drug inflation and utilization. Oscar assumed an annual medical trend of 4.7%.

- Administrative Expenses, Taxes and Fees, and Risk Margin Changes to the overall premium level are needed because of required changes in federal and state taxes and fees. In addition, there are anticipated changes in both administrative expenses and targeted risk margin.

- Prospective Benefit Changes Plan benefits have been revised as a result of changes in the Center for Medicare and Medicaid Services (CMS) Actuarial Value Calculator and state requirements, as well as for strategic product considerations.

- COVID-19 Pandemic Changes to the overall premium level are needed because of the unwinding of the Public Health Emergency, a proportion of Medicaid Redeterminations enrolling in the ACA Marketplace, and the change in expected costs attributed to COVID-19.

Advertisement