(sigh) When I last checked in on Virginia, things were looking up a bit (relatively speaking), as Anthem Blue Cross Blue Shield (aka "HealthKeepers") had announced that they were jumping back into the state in order to cover the 60-odd counties which would otherwise be left bare by Optima Health Insurance dropping out of half the state a week or so earlier.

As many see their options for health plans dwindle down to one insurer, premiums are simultaneously set to rise by an average of 57.7 percent next year in Virginia’s individual marketplace.

The increase is “unquestionably the highest we’ve ever seen,” David Shea, health actuary with Virginia’s Bureau of Insurance, told lawmakers Monday.

Regular readers know that one of the issues I've spent the better part of the past year yammering on about endlessly is the importance of Congress formally appropriating Cost Sharing Reduction reimbursement payments to the insurance carriers on the individual market exchanges.

Thanks to the ongoing/pending ruling in the federal House vs. Burwell Price lawsuit, Donald Trump has the ability to pull the plug on CSR payments pretty much whenever he wants to (and he's threatened to cut them off every month since around March or April so far). CSR payments hang like a Sword of Damocles over the heads of every exchange-based insurance carrier each month, with them never knowing whether they'll get reimbursed or not.

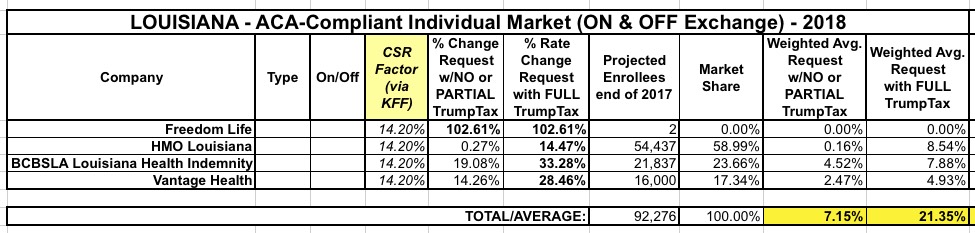

Louisiana was one of the last states I ran rate hike analysis on just a month ago: Three carriers on the exchange (plus the "Freedom Life" phantom carrier), averaging around 21.4% rate increases on the assumption that CSR payments won't be made. According to the Kaiser Family Foundation, loading CSRs onto Silver plans only would bump them up by an additional 20 points; this translates into roughly 14.2 points if spread across all metal levels on & off the exchange. Based on that, I estimated LA's rate increases at 21.4% without CSRs but only 7.2% if they actually are paid.

I've written not one, not two, but three different blog entries in the past 24 hours about Bernie Sanders' just-announced "Medicare for All" proposal...but the reality is, I shouldn't have. Frankly, while it's a discussion/debate that we do need to have, making a big thing about it right this moment is, the more I think about it, terrible timing, because the Affordable Care Act is still in being attacked and at risk in several ways:

FIRST: The CSR issue still hasn't been resolved, although at this point it's extremely unlikely that Patty Murray and Lamar Alexander are going to pull a CSR/reinsurance rabbit out of their hats after all. Last week things looked somewhat promising, but this week it appears to have gone off the rails again...and with just 17 days left in the fiscal year (and, I believe, only 14 days before the contracts have to be signed by carriers for 2018 exchange participation), there's almost no time left to get even a minor stabilization bill pushed through.

SECOND: On a related note, Bill "so much for the Jimmy Kimmel test!" Cassidy and Lindsey Graham are still trying to cram through their pile-of-garbage Hal Mary Trumpcare bill, which is at least as bad as the GOP's failed AHCA/BCRAP bills were earlier this year and even worse in some ways. Again, there's only 17 days left to pull it off, but remember what happened with AHCA last spring...anything's possible. Here's a summary of the impact of the Cassidy-Graham bill via Andy Slavitt and the Centers for Budget & Policy:

Anthem on Wednesday continued reducing its Obamacare business, as the big insurer said it will cut in half the number of counties in Kentucky where it sells individual health plans next year.

As I noted last month with my "Silver Switcharoo" explainer, for carriers which remain in the ACA exchanges next year, there's three potential scenarios which could happen (well, four, actually, if you include "Congress manages to sneak a full CSR appropriation bill into law just under the wire", although that seems pretty unlikely at this point given the time crunch and the fact that it'd need a 2/3 majority in both the House and Senate to avoid being vetoed by Trump anyway):

Back in early June, the New York Dept. of Financial Services posted the requested 2018 rate hikes for the individual and small group markets. In most states, the CSR reimbursement issue is a much bigger factor than whether or not the Trump Administration enforces the individual mandate, but in New York it's the exact opposite: According to the NY DFS, loss of CSR payments would only tack on 1.3 points to the total, while "a full repeal of the federal individual mandate would increase rates by an additional 32.6%".

The reason for the fairly nominal CSR factor is that the vast majority of NY's CSR-eligible population (those earning 138-200% FPL) is instead enrolled in the state's Basic Health Program. As a result, only 26% of New York's exchange enrollees receive CSR assistance, and the 200-250% FPL recipients only receive a fairly skimpy amount of CSR help anyway. At the opposite end of the spectrum, the 32-point mandate factor is far higher than most carriers are indicating (more like 4-5 points), but there's a big difference between the administration "not enforcing" the penalty and outright repealing it, which NY DFS is talking about.

In any event, this means that NY's requested average increases boiled down to: 15.0% if CSRs are paid/mandate enforced, 16.6% if CSRs aren't paid/mandate is enforced, or a whopping 50.5% if CSRs aren't paid and the mandate was repealed.

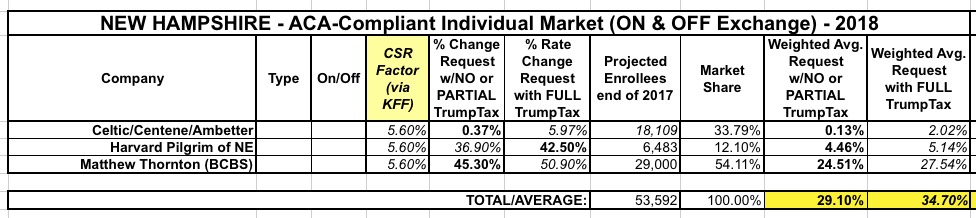

New Hampshire's a bit of a head-scratcher this year: Of the three carriers on the individual exchange next year (each of whcih has a significant chunk of the market), Centene is requesting virtually no rate increases whatsoever...while the other two are asking to raise their rates by over 40% apiece.

Even more odd: Harvard Pilgrim's 42.5% seems to assume the worst regarding CSRs/mandate enforcement...yet Matthew Thornton (BCBS) is asking for 45.3% while assuming CSRs will be paid.

Finally, Kaiser assumes around a 10% Silver rate increase in NH if CSRs aren't paid, which translates into about 5.6% spread across the entire membership. Result: 29.1% if CSRs are paid, 34.7% if they aren't.

Massachusetts has one of the stablest statewide insurance markets, no doubt in large part due to their having instituted the precursor to the ACA, "RomneyCare", 4 years earlier. Massachusetts also merged their small business and individual market risk pools, which helps stabilize things. As a result, they have a high number of carriers participating in their ACA exchange and are among the few states with single-digit average rate hikes...assuming CSR payments are forthcoming and the individual mandate is properly enforced.

Assuming CSR payments aren't made, I used the Kaiser Family Foundation's 19% average estimate for Silver plan hikes due to the CSR factor. Since a whopping 92% of MA's exchange enrollees chose Silver plans (it looks like MA's unique "ConnectorCare" plans are considered Silver as well), that means an average CSR factor of around 17.5 points across the entire individual market.

Louisiana has 3 individual market carriers for 2018 (technically there's 4, but "Freedom Life" is basically just a shell company with a placeholder filing). Officially, they're requesting average rate increases averaging around 21.4%...but all three carriers state point-blank in their filing letters that a huge chunk of their request is due specifically to the CSR reimbursement and mandate enforcement issues. The Kaiser Family Foundation estimates the CSR issue alone adds around 20 points to Silver plans, and 71% of Louisiana exchange enrollees chose Silver, so that translatest into roughly 14.2 points across the whole market. This results in just a 7.2% average rate hike if CSR payments are made vs. 21.4% if they aren't: