Now that it appears that the full list of states and counties eligible for hurricane (or windstorm, in the case of Maine) Special Enrollment Periods (SEP) has settled down, Huffington Post reporter Jonathan Cohn asked an interesting question:

How if at all do you allow for the extensions in FL, TX, etc.? Or, to put another way, how many post-Dec 15 signups through https://t.co/bhGNSognZK do you expect?

The closest parallel to this particular situation I can think of was the #ACATaxTime SEP back in spring 2015. In that case, it was the first year that the ACA's (defunct as of this morning) Individual Mandate was being enforced, and a lot of people either never got the message about being required to #GetCovered or at least pretended that they didn't.

INSURANCE DEPARTMENT RELEASES PROPOSED RATES FOR 2018 HEALTHCARE EXCHANGE

Atlanta – Insurance Commissioner Ralph Hudgens announced today that his office had submitted proposed 2018 health insurance rates to the Centers for Medicare and Medicaid Services (CMS) for the federally-facilitated Healthcare Exchange for final federal approval.

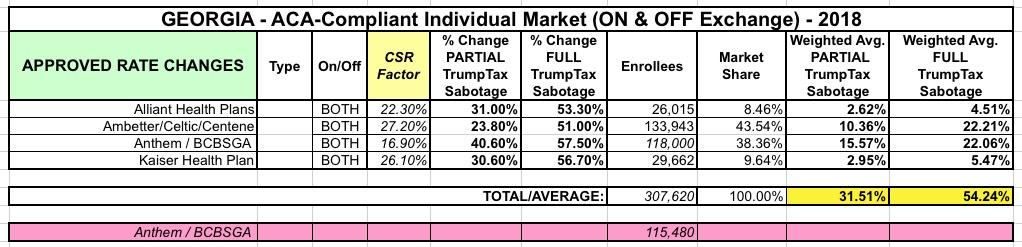

“Today my office submitted 2018 Obamacare rates to Washington D.C. for approval,” Hudgens said. “In its fifth year, Obamacare has become even more unaffordable for Georgia’s middle class with potential premium increases up to 57.5 percent. I am disappointed by reports that the latest Obamacare repeal has stalled once again and urge Congress to take action to end this failed health insurance experiment.”

Including Georgia, I've now compiled initial 2018 unsubsidized individual market rate hike requests for 17 states...and Georgia's carriers are asking for by far the highest overall average increase, even assuming no Trump/GOP sabotage tax.

There appear to be four carriers which have filed to sell individual market plans in Georgia next year: Alliant, Ambetter (aka Celtic, aka Centene...for God's sake, pick one name, guys, willya??), Anthem Blue Cross Blue Shield and Kaiser Health Plan.

Over the past few months, my Congressional District Breakdown tables estimating how many people would likely lose healthcare coverage if the ACA were to be "cleanly" repealed (with no replacement) have gotten a lot of attention. This was followed by the Center for American Progress (CAP) running their own estimates of how many would likely lose coverage if, instead of a "clean" repeal of the ACA as a whole, the ACA were to be partially left in place, with the GOP's AHCA (Trumpcare) bill, which dramatically changes the ACA, being signed into law instead.

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

My standard methodology applies:

Plug in the 2/01/16 QHP selections by county (hard numbers via CMS)

Project QHP selections as of 1/31/17 based on statewide signup estimates

Knock 10% off those numbers to account for those who never end up paying their premiums

Multiply the projected effectuated enrollees as of March by the percent expected to receive APTC subsidies

Then knock another 10% off of that number to account for those only receiving nominal subsidies

Whatever's left after that are the number of people in each county who wouldn't be able to afford their policy without tax credits.

In the case of Georgia, assuming 567,000 people enroll in exchange policies by the end of January, I estimate around 396,000 of them would be forced off of their policy upon an immediate-effect full ACA repeal.

UnitedHealth Group Inc., the biggest U.S. health insurer, is scaling back its experiment in Obamacare markets as its Harken Health Insurance Co. startup withdraws from the two exchanges where it was selling plans.

Harken will not offer individual plans through Obamacare exchanges in Georgia and Chicago in 2017, the company said Thursday in an e-mailed statement. It will continue to offer individual plans off the exchange, Harken said.

As commenter ME notes, there are currently around 22,800 Harken enrollees in Illinois and another 10,500 in Georgia. I have no idea what the on/off exchange ratio is, however, so the number of people who will actually have to shop around will be up to 33,300; assuming, say, 2/3 are on the exchange, that would be roughly 22,000 people.

About a month ago, when I first plugged in the average requested 2017 rate hikes for Georgia's ACA-compliant independent market, I came up with an overall weighted average of around 27.7%. However, there was one major gap in the data: I had trouble finding Ambetter/Peach State's enrollment numbers or even their average rate hike request, so I reluctantly left them out of the calculation completely.

When Aetna announced that they were dropping out of the Georgia exchange-based independent market, I went back and removed them from the mix. Since Aetna's request had been 15.5% on a substantial share of the market, this meant that the rest of the statewide average shot up to 32.0%.

Today I was able to track down the missing Ambetter/Peach State data--both the average requested rate hike (around 8.0%) as well as the number of current enrollees impacted...around 73,000:

IMPORTANT: This is really just a placeholder for Georgia's 2017 average rate hike requests, because it's extremely spotty and partial so far. I'll update it once I'm able to actually track down the bulk of Georgia's individual market enrollment and rate hike request numbers.

UPDATE 7/25/16: I've managed to acquire the additional filings; see update below

UnitedHealth Group will stop offering plans on Arkansas' health insurance exchange next year, a spokesman for the Arkansas Insurance Department said Thursday.

The Minnetonka, Minn.-based insurer offered plans this year for the first time, but it didn't submit plans to the department for 2017, department spokesman Ryan James said.

The deadline for insurers to submit such plans was April 1, he said.

This is hardly unexpected news for a couple of reasons. First, UHC made huge waves last November by making a big, dramatic announcement that they might very well drop out of the ACA exchanges altogether next year after taking large losses on exchange enrollees in 2015. As you may recall, this was a very oddly-timed announcement given that they had issued a glowing quarterly report just a month earlier which made it sound like everything was hunky-dory.

{kind=link}