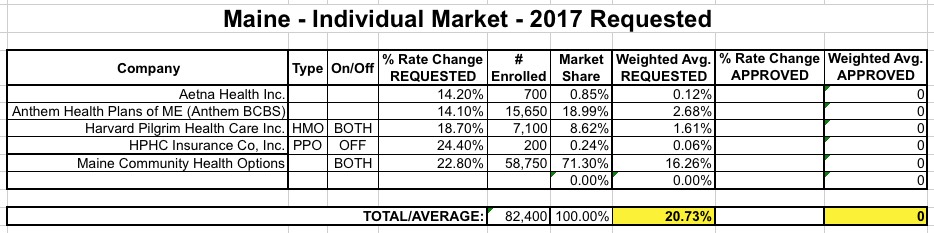

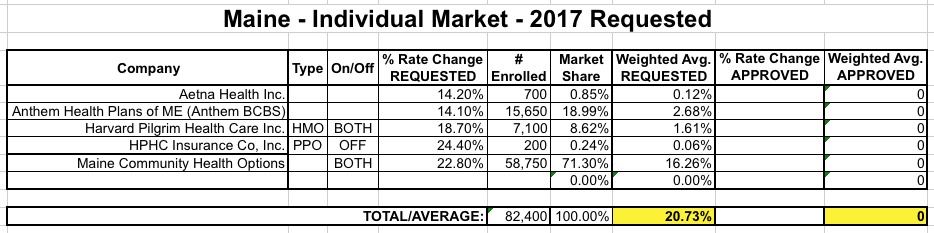

The good news for me out of Maine is that they've released the filings for all three individual market carriers for 2018 (Aetna has around 1,000 enrollees but they're leaving the individual market entirely), and all three include the exact number of current enrollees, making the average rate hike request simple enough on the surface: 21.2% for Anthem, 39.7% for Harvard Pilgrim (HPHC) and 19.6% for Maine Community Health Options (one of the few remaining ACA-created CO-OPs*), for a weighted average unsubsidized increase request of 25.2%.

*UPDATE: My mistake! I accidentally confused MCHO with Evergreen Heatlh of Maryland, which is in the process of converting itself from a Co-Op into a private carrier! Thanks to Louise Norris for the catch!

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

Normally I post screenshots from the revised/updated SERFF filings and/or updates at RateReview.HealthCare.Gov, but it takes forever and I think I've more than established my credibility on this sort of thing, so forgive me for not doing so here. Besides, #OE4 is approaching so rapidly now that this entire project will become moot soon enough, as people start actually shopping around and finding out just what their premium changes will be for 2017.

The other reason I'm not too concerned about documenting the latest batch of updates/additional data is because in the end none of it is making much of a difference to the larger national average anyway; no matter how the individual carrier rates jump around in various states, the overall, national weighted average still seems to hover right around the 25% level.

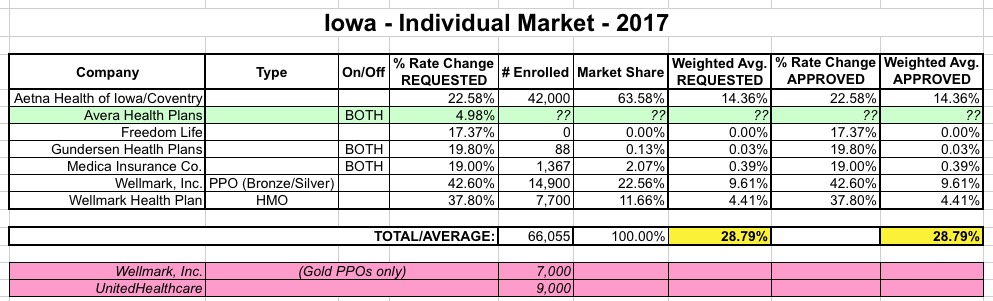

Still, for the record, here's the latest...in four states (Iowa, Indiana, Maine & Tennessee) I've just updated the requested and/or approved average increases. In the other four (Massachusetts, Montana, North & South Dakota) I've added the approved rate hikes as well.

Since then there have been two major changes: First, Aetna, which had been planning on entering the Maine ACA exchange, infamously pulled a complete 180 and not only decided not to expand, but actually pulled out of the exchange in most of the states they're already in. This doesn't really impact Maine since they were only available off-exchange anyway. The second change does, however: Several of the carriers submitted revised requests, pushing the average up higher, to 23.9%.

As numerous sources have already indicated, after 2 years of (relatively) low average premium rate increases on the individual market (around 5.6% in 2015 and 8.0% in 2016...compared with the 10-12% average rate hikes over the previous decade), it looks like 2017 will finally see the higher rate hikes that ACA critics have been screaming about every year.

So far, Virginia and Oregon have reported requested rate increases of 17.9% and 27.5% respectively, while California may be looking at 8.0% increases (which is high for them).

A couple of days ago I noted that after two years of nothing but doom & gloom (and coming just a week after UnitedHealthcare pulled the plug on the individual market in over two dozen states) there seems to finally be some positive developments, with companies like Centene and Anthem reporting better-than-expected results. They may not be making a profit yet, but at least they aren't losing money hand over fist the way they did the first couple of years.

I also made a brief mention of the Maryland Co-Op, Evergreen Health, which reported their first quarterly profit since launching 2 1/2 years ago.

Consumer operated and oriented health plans in Maryland, New Mexico and Massachusetts will report profits in the first quarter, in a sign that some of the remaining Affordable Care Act-created nonprofits could be finding their footing on the state exchanges.

(sigh) OK, this one is not related to the Risk Corridor Massacre, since Community Health Options was actually profitable in 2014 and therefore never qualified for any RC payments anyway. Also, unlike the dozen ACA-created co-ops which are in the process of winding down operations by the end of the year, CHO is not going out of business, and in fact is remaining fully operational for 2016.

Maine's Community Health Options said Dec. 9 that it will cut short its sales of individual policies for 2016, in a sign that it is the latest Affordable Care Act-funded consumer operated and oriented plan to encounter financial difficulties.

I admit that given the carnage of the past couple of weeks, I'm almost afraid to post this entry...but I had to write something positive about the CO-OP situation.

With the ACA-created CO-OPs seemingly dropping like flies due to the #RiskCorridorMassacre, I thought this would be a good time to flip things around and look at which CO-OPs are doing well (or at least not badly).

This isn't much, but it'll do for now:

Wisconsin's insurance department says it has no intention of shutting down its #ACA co-op, which appears it will remain solvent next year.

Most Mainers buying Affordable Care Act insurance will see modest increases in their premiums for 2016, below the national average and much lower than the double-digit increases projected in some cities by a recent study of initial rate filings.

About 80 percent of the 75,000 Mainers purchasing ACA marketplace insurance have a plan through Lewiston-based Community Health Options – formerly Maine Community Health Options. The ACA marketplace, operated on the Web as healthcare.gov, is where those without insurance – often part-time or self-employed workers – can obtain subsidized benefits.