In Part 2, I go into more detail about the different types of NON-ACA plans available on the individual market, why they mostly stink, and how the repeal of the Individual Mandate Penalty, especially when combined with Trump's yanking away restrictions on "short-term" and "association" plans, will take an existing problem and make it far worse.

Oh, yeah: It involves Dabney Coleman and Morgan Freeman.

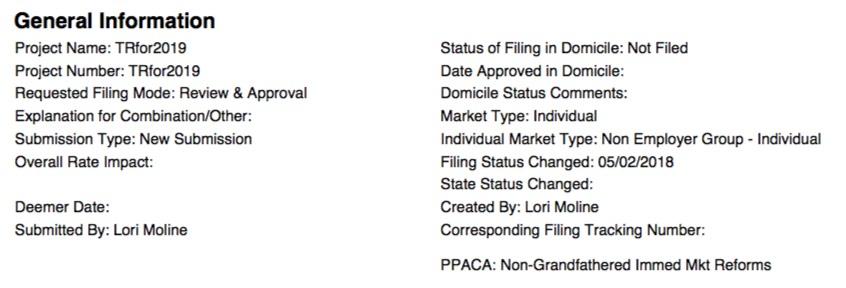

Aside from Virginia, it's likely going to be another month or so before the 2019 ACA policy rate filings start trickling in, since the deadline for initial rate requests isn't until late June in most states. However, there's some interesting non-ACA policy filing stuff which is available as well. Given all the concern about non-ACA compliant policies siphoning healthy people away from the ACA market, I figured I should take a look at a few of these.

Here in Michigan, I've found three such filings: One is for "transitional" plans from Golden Rule (a subsidiary of Unitedhealthcare, I believe). The other two are for "short-term" plans (the type which Donald Trump is basically removing any regulation on).

I've repeatedly written about how Donald Trump is still deperately trying to sabotage the ACA by any means necessary. Last year it was all about a combination of regulatory and legislative attacks, but aside from repealing the ACA's individual mandate (which was, admittedly, a pretty ugly blow), the GOP-held Congress was unsuccessful at tearing it down legislatively.

Therefore, for 2018, Trump has decided to double down on the regulatory side...and one of the main ways he hopes to achieve this is by opening up the floodgates on so-called "Short-Term, Limited Duration" policies, which aren't subject to most ACA requirements and therefore are a) free to siphon off healthy ACA-compliant enrollees into b) substandard healthcare plans which can leave thousands of people in dire straits.

Over at the Kaiser Family Foundation, Karen Pollitz and Gary Claxton have published a handy explainer which goes over the basics of the various types of NON-ACA individual market policies...specifically, the "Short Term" and "Association" plans which Donald Trump is attempting to flood the market with by essentially removing any restrictions or regulations on them, but also the "Idaho Style" plans which were rejected by HHS for being flat-out illegal as well as the "Farm Bureau" junk plans which Iowa recently decided to open the floodgates on (Tennessee already had a similar setup, and sure enough, it has proven pretty devastating to Tennessee's ACA market since 2014 as a result). The whole thing is worth a read, but in the early part of their explainer, however, they also happened to neatly lend support to my estimates from last week regarding the unsubsidized market:

I've obviously already written a bunch of stuff about this, including links to a few impact projection analyses, but this one was put together by Avalere Health on behalf of America's Health Insurance Plans (AHIP), which is one of the two major insurance carrier lobbying groups (the other one is BCBSA). On the surface you may expect a whitewash: "Oh, look at that, a report commissioned by Big Insurance is releasing a report claiming that these policies would be awesomesauce, big surprise!"

For some time now, I've been railing against Donald Trump's executive order pushing for the expansion of both "Short Term, Limited Duration" plans as well as "Association Plans". I've scornfully referred to his EO with the hashtag #ShortAssPlans.

Something which has gotten lost in the shuffle, however, is that I don't think short-term plans should necessarily be scrapped altogether, at least until we're able to achieve a comprehensive, universal coverage system in the future. Under our current patchwork heatlhcare system, I do think they serve a purpose for certain people in certain circumstances. I just think they need to be strongly regulated and limited in scope, partly to prevent siphoning off healthy people from the individual market risk pool...but partly to prevent people from being hit with financial catastrophe in the event of unexpected high medical expenses.

The problem is that Trump's executive order--which would effectively open the floodgates for them to be mutated into year-round plans, completely destroying one of the major points of the ACA in the first place.

Former CMS representative and current healthcare policy advisor for Sen. Brian Schatz, Aisling McDonough, made an important point last night:

If you have a pre-existing condition and live in a rural area, especially in VA, TN, OH, IN, MO, IA, or NV, then I'm worried there might not be a plan available for you next year.

People should be worried about bare ACA counties in 2019 b/c of GOP sabotage.

Between mandate repeal, short-term plans, health ministries, farm bureaus, etc, the guaranteed $ for the lone ACA insurer is getting smaller. It's not the same calculus as it was in 2017 & 2018.

Five weeks ago, when Idaho Governor "Butch" Otter announced that Idaho had decided to basically just blow off federal law altogether and start offering non-ACA compliant health insurance policies on the individual market alongside the compliant versions, I wrote:

To be honest, I'm not entirely sure I understand why Idaho would do this. Yes, of course the deep red state government opposes the ACA in general and sure, they want to "lower premiums" on the individual market, but Trump's recent "ShortAss Plan" executive order would do pretty much the same thing(allowing non-ACA compliant off-exchange "Short Term/Association Plans" which amount to the same thing...without putting GOP Gov. Butch Otter's fingerprints all over the ugly stories which would soon follow if/when people started actually enrolling in these types of policies. Besides, as much as Idaho claims to hate the ACA, they seem to be quite proud (and rightly so) of their own state-based ACA exchange, Your Health Idaho.

Well, it sounds like CMS Administrator Seema Verma was thinking along the same lines, because this unexpected story broke a few hours ago: Verma sent a letter to Otter and his state Insurance Commissioner shooting down their "state-based plans" idea as being flat-out illegal.