State by state: The ~45 million Americans whose healthcare is threatened by the GOP's budget bill

Fri, 05/02/2025 - 11:17am

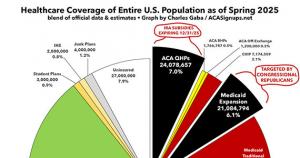

With all the understandable focus on Congressional Republicans efforts to effectively end Medicaid coverage for nearly 21 million Americans enrolled via ACA expansion, there's been much less attention paid to the other looming threat to healthcare coverage: The expiration of the upgraded financial subsidies for ~24 million ACA exchange enrollees, which are currently scheduled to end this New Year's Eve.

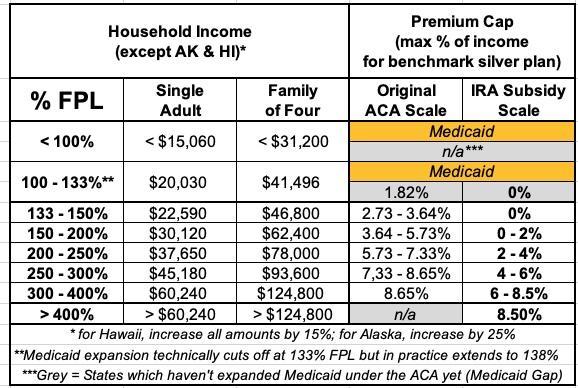

As I've explained numerous times before, the ACA's original premium subsidy formula was always far too stingy to make individual market policies affordable for many people...and worse yet, the subsidies cut off entirely for households making more than 4 times the Federal Poverty Level (FPL).

The sliding scale started with households earning between 100 - 133% FPL (roughly $20K/yr for a single adult) having to pay around 2% of their income in premiums and worked its way up to around 9-10% at higher incomes...ending at 400% FPL (around $60K/yr for a single adult). (The exact percent households have to pay varies slightly from year to year based on an obscure formula known as PAPI).

The good news is that the American Rescue Plan Act of 2021, followed by the Inflation Reduction Act of 2022, included provisions which dramatically improved the ACA's premium subsidy formula in two ways: First, it changed the sliding scale from a range of around 2 - 10% of income to a range of 0 - 8.5% of income. Secondly, it removed that hard cap at 400% FPL, meaning that middle-class families would still be eligible to receive at least some relief from high premiums.

Here (again) is a side by side comparison of the two formulas; the IRA scale is really what it should have been in the first place. In fact, if this had been the case back when the first ACA Open Enrollment Period launched, I'm pretty sure public approval of the new law would have been much higher and we would have avoided much of the drama which played out over the next few years:

The bad news is that these upgraded subsidies are set to expire on 12/31/25, which means that starting January 1, 2026, the formula will revert back to what it was as of 2020. The lowest income enrollees will have to go back to paying between 1.8 - 3.6% of their incomes in premiums; those earning 200 - 400% FPL will see significant bumps in what they have to pay; and anyone earning more than 400% FPL will once again fall into the "Subsidy Cliff" where they have to immediately pay full price.

Worse yet for the latter population, not only will they have to pay full price again, it will be full price plus six years of medical inflation. On top of that, the Congressional Budget Office (CBO) projects that average unsubsidized ACA premiums will increase another ~4.3% beyond "normal" increases next year due purely to the adverse selection caused by the IRA subsidies ending.

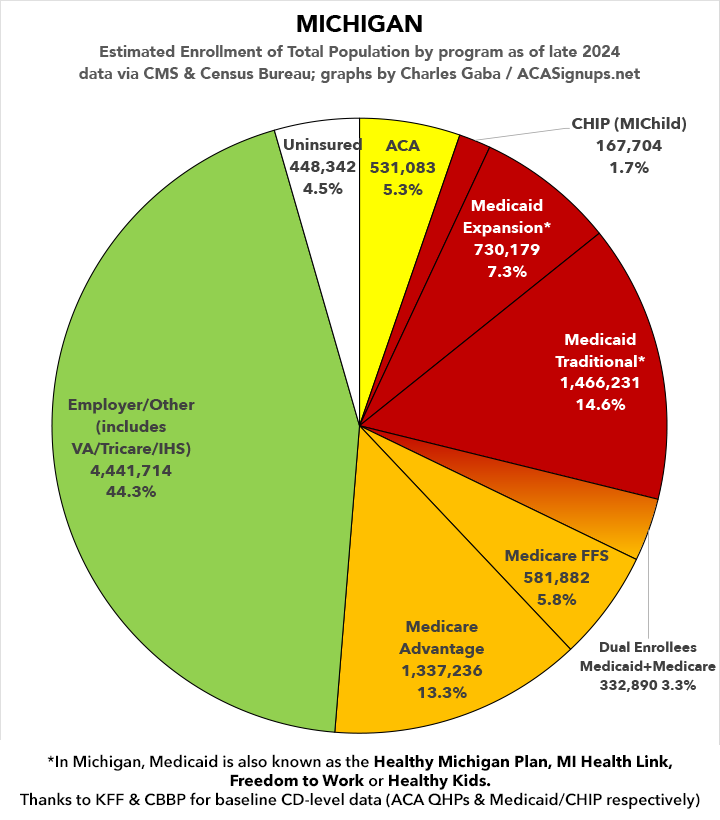

A major project of mine in recent months was to create state-by-state examples of what the real-world impact of these rate hikes will be for various households in every state at different income levels. For example, in my home state of Michigan:

- A single 50-yr old would see his net premiums jump by as much as 196%

- A single parent earning $30,000/year would go from paying nothing to $87/month...technically an infinite increase.

- A family of four earning $60,000/year would see their premiums jump from $84/month to $270/month...more than triple their 2025 premiums.

- A 64-yr old couple earning $90,000/yr would have to shell out over $20,000 MORE per year for the same coverage. In fact, their monthly premium would nearly quadruple to $2,380/month.

Use the drop-down menu here to get an idea of how ugly it could get in your state.

Unlike the Medicaid expansion population, where up to all 21 million enrollees could potentially lose their coverage, the impact of the IRA subsidies expiring probably won't be nearly as horrific, with the CBO projecting "only" around 2.2 million being forced to drop coverage next year (rising to around 3.8 million over the next few years).

HOWEVER, the remaining ~20 million or so ACA exchange enrollees would still be forced to either pay far more for the same coverage or drop down to a worse plan with higher deductibles & co-pays (or potentially both higher premiums for worse coverage in many cases).

UPDATE: I should also note that many exchange enrollees are also going to find themselves having to move to a different plan whether they want to or not due to insurance carriers bailing on the ACA exchanges entirely if the IRA subsidies aren't extended, as yesterday's announcement by Aetna proved.

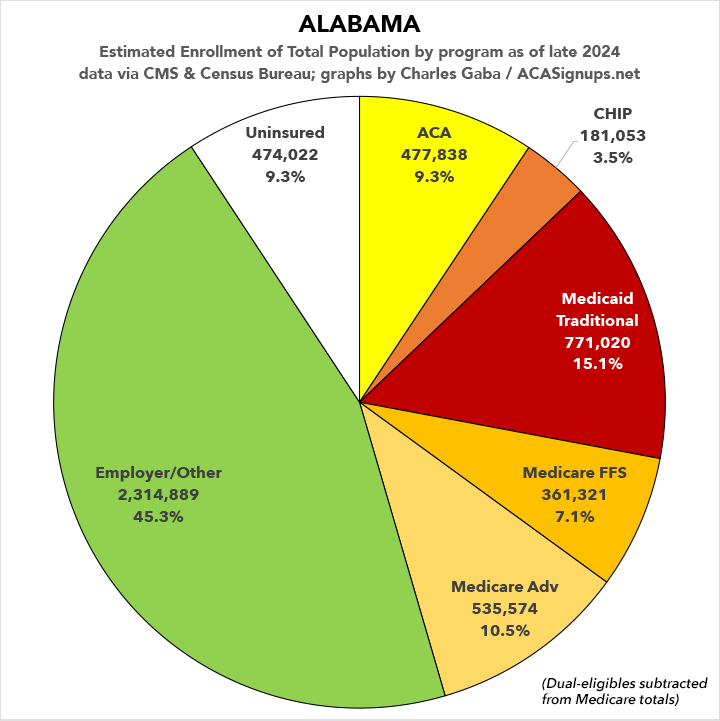

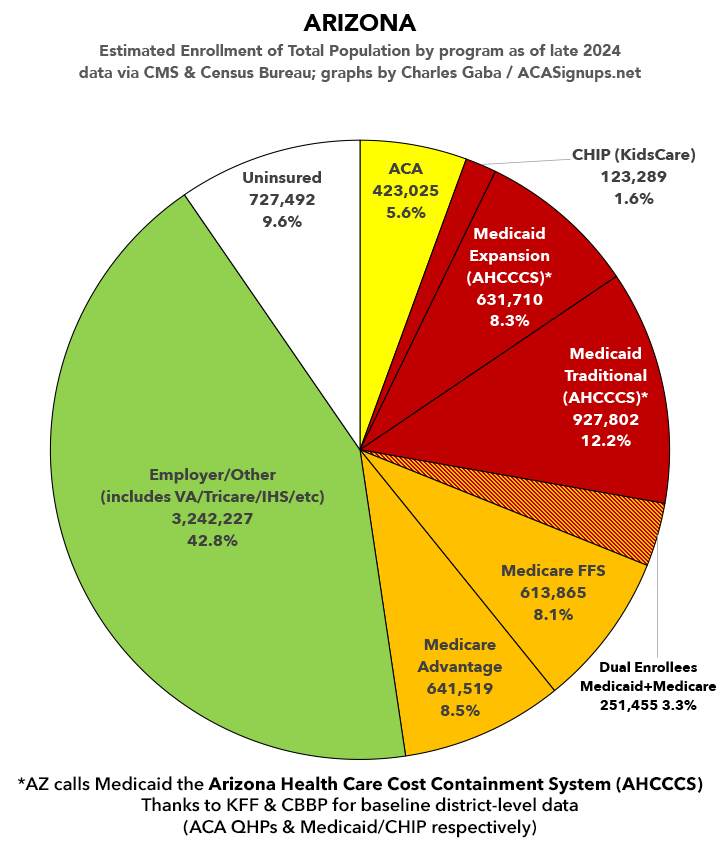

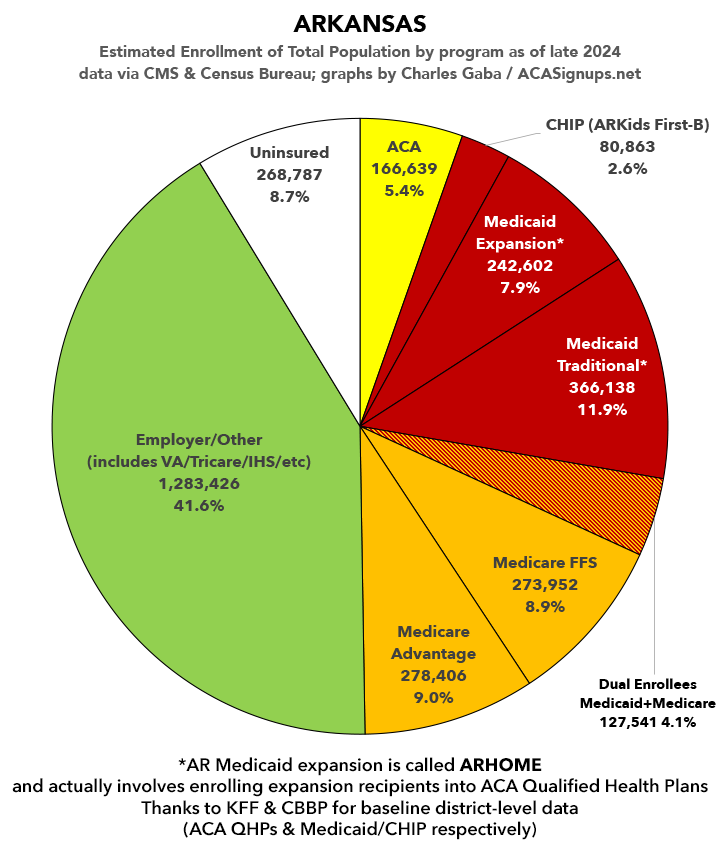

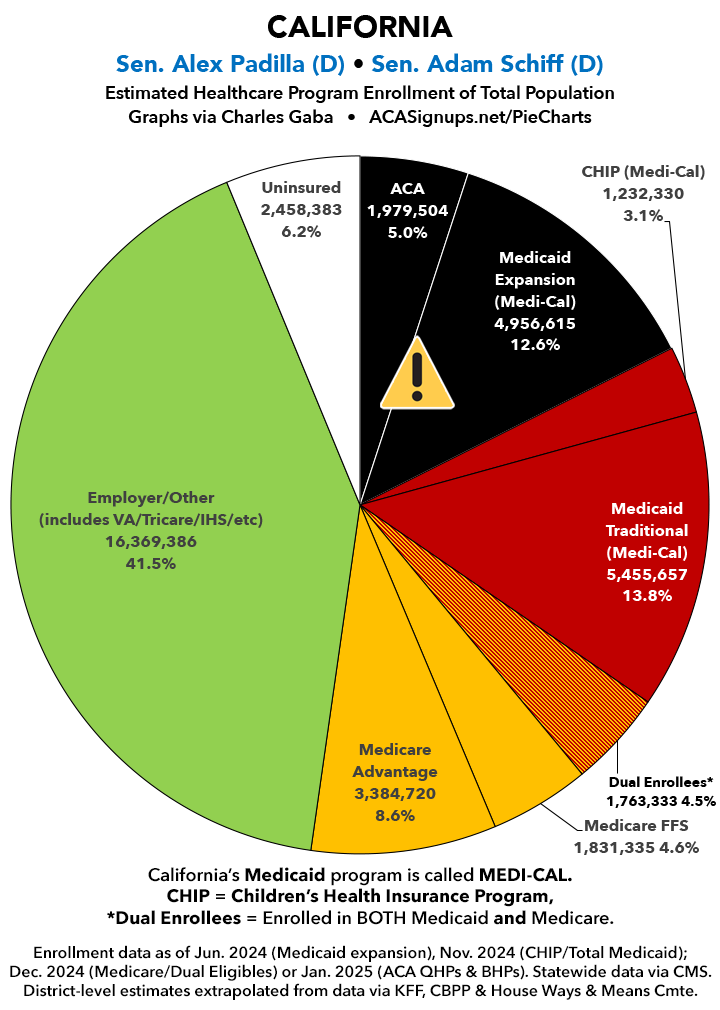

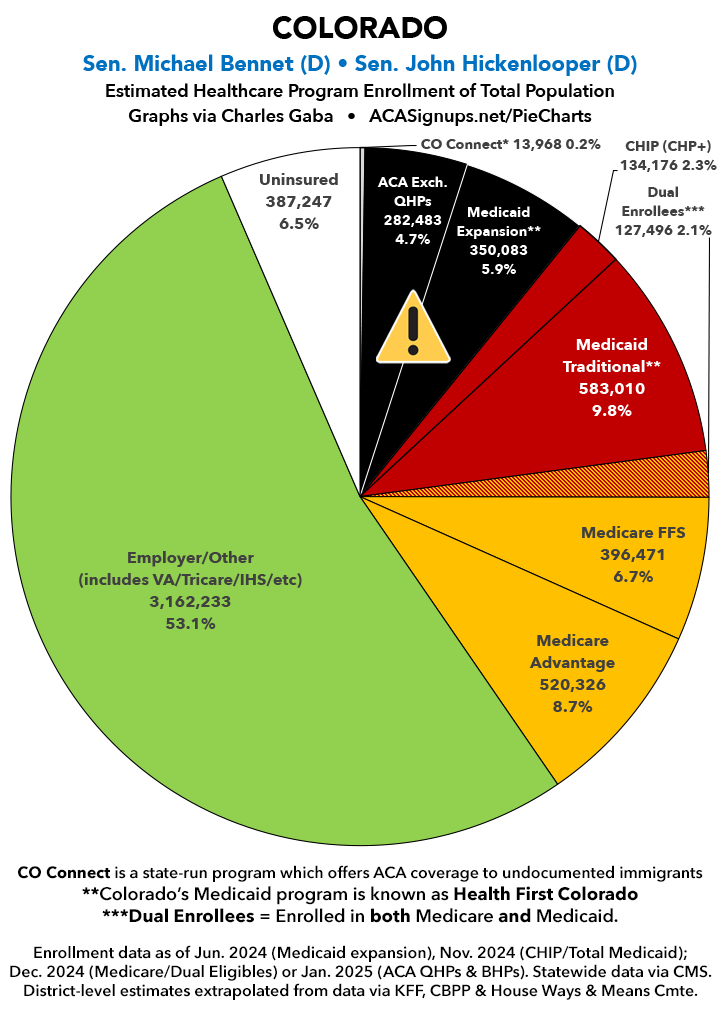

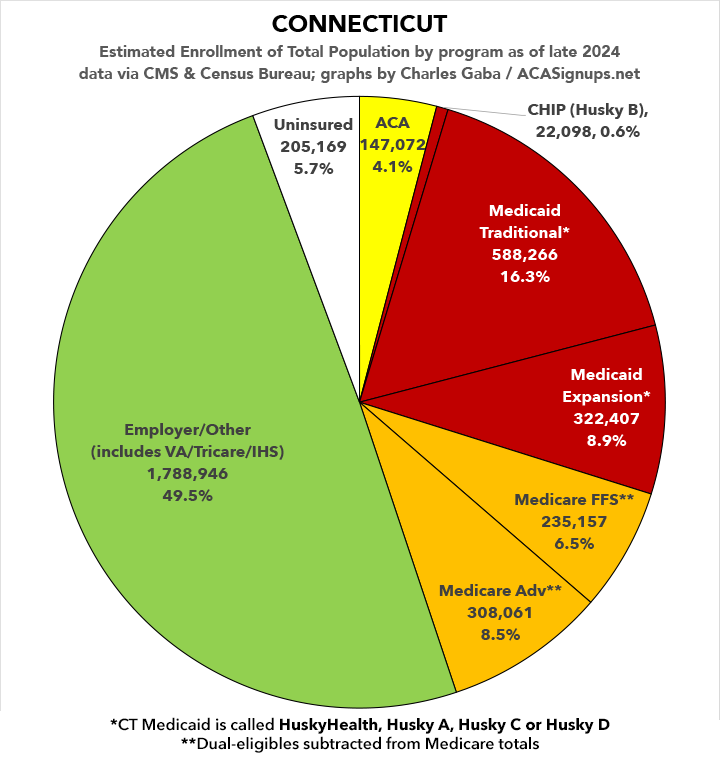

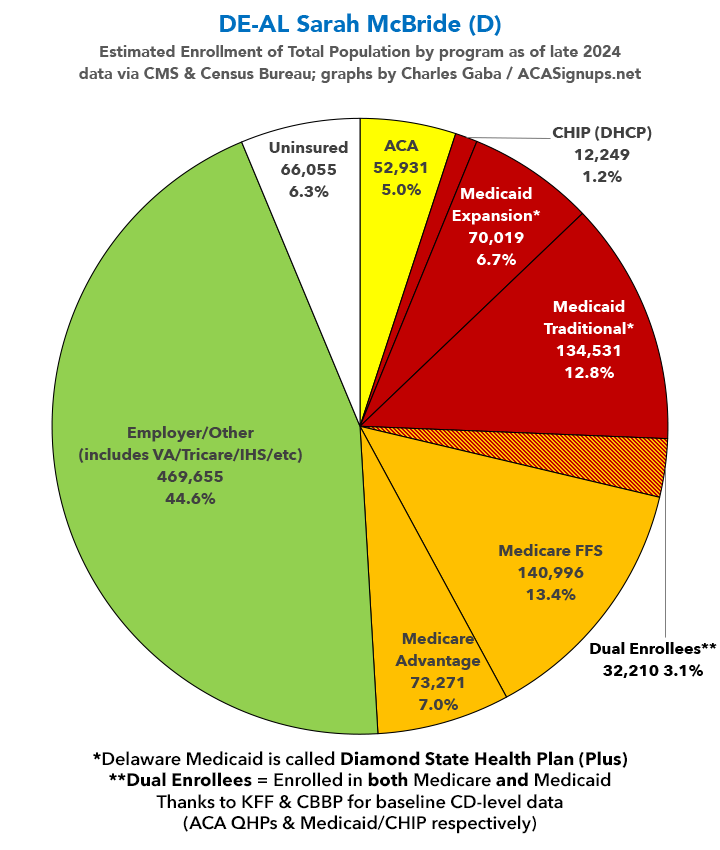

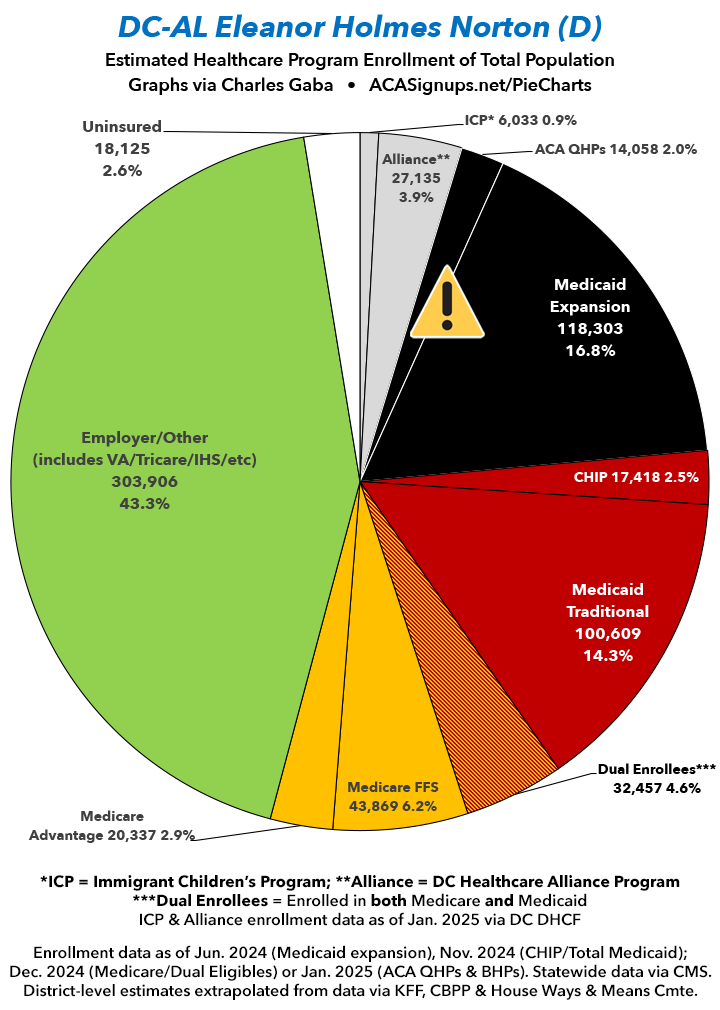

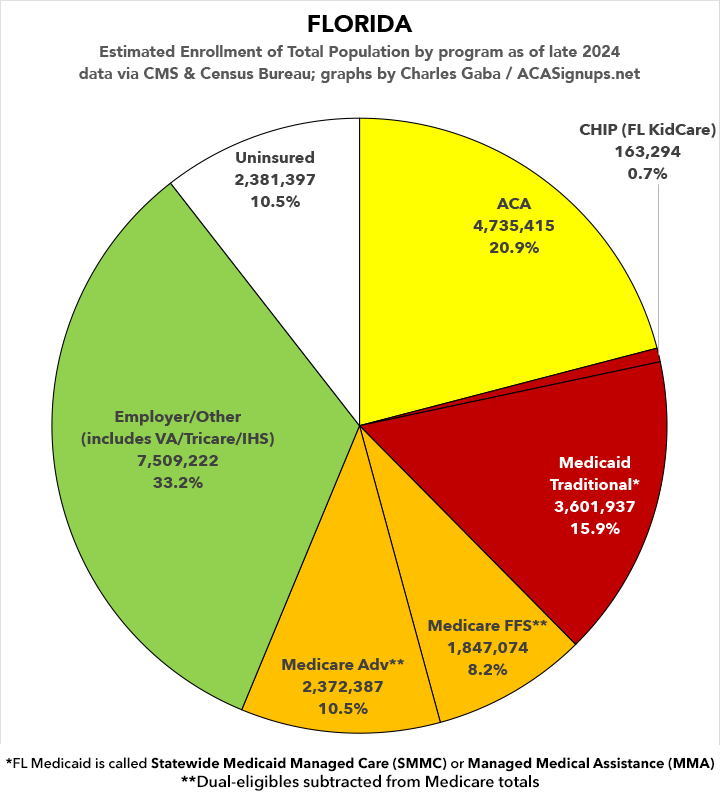

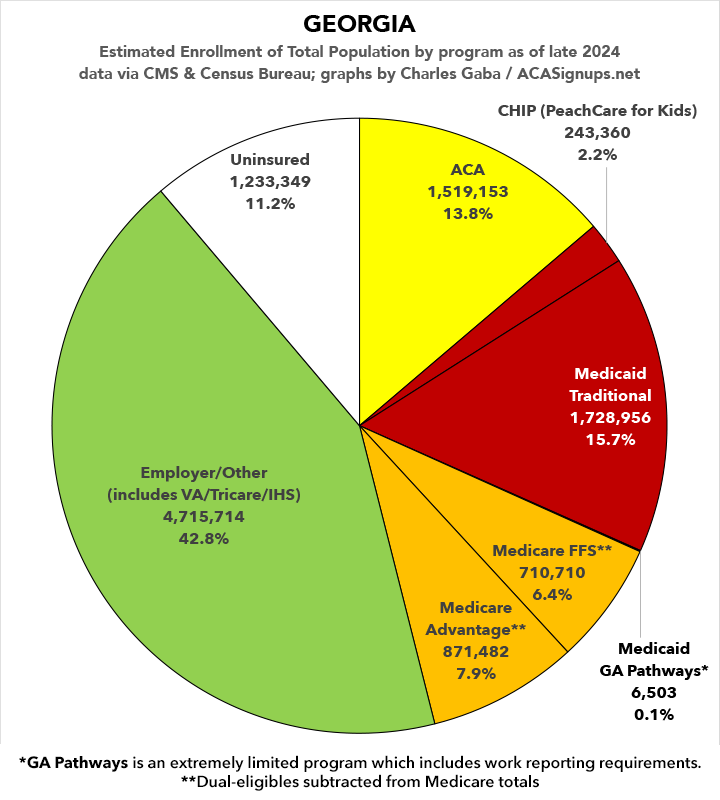

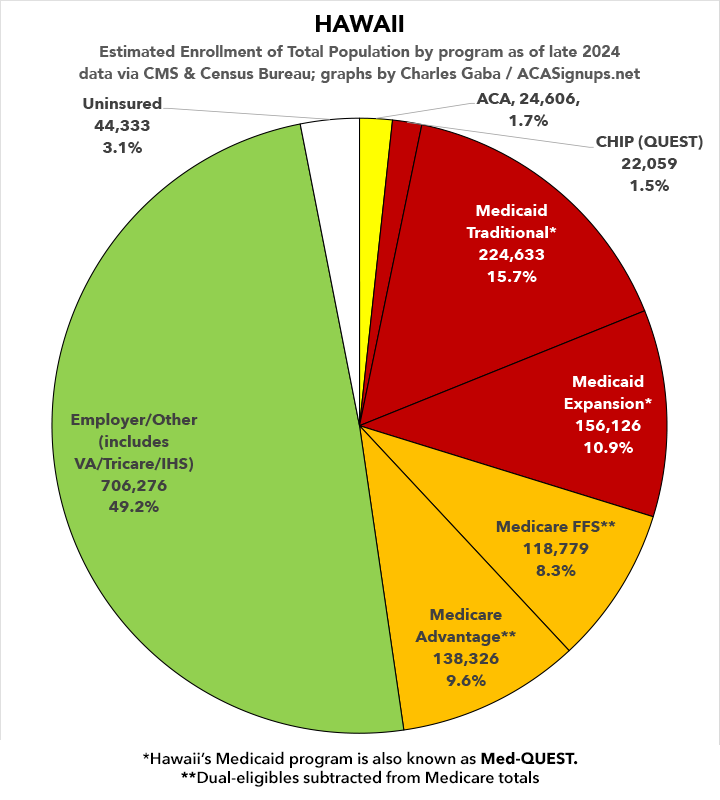

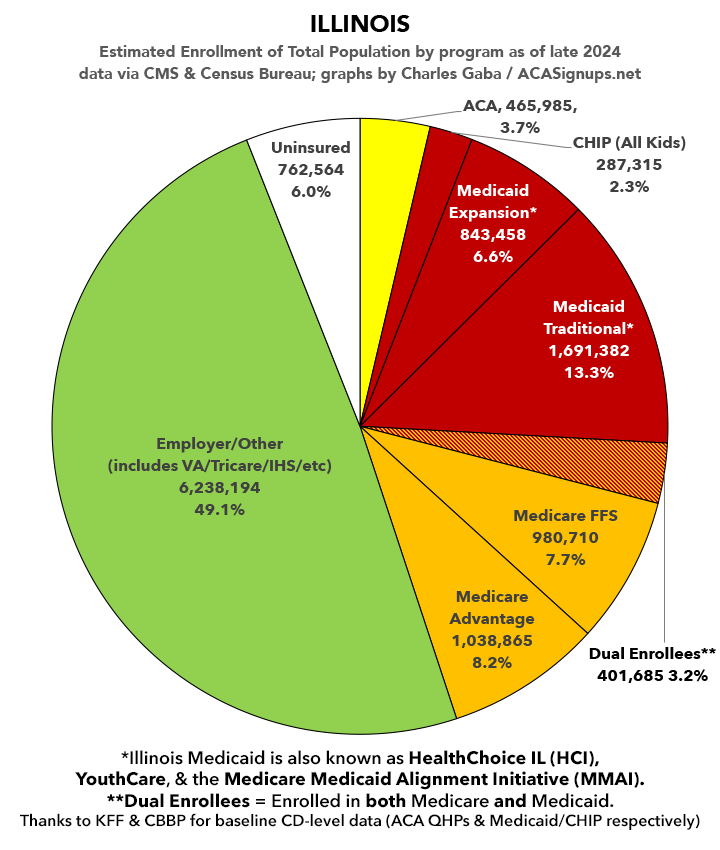

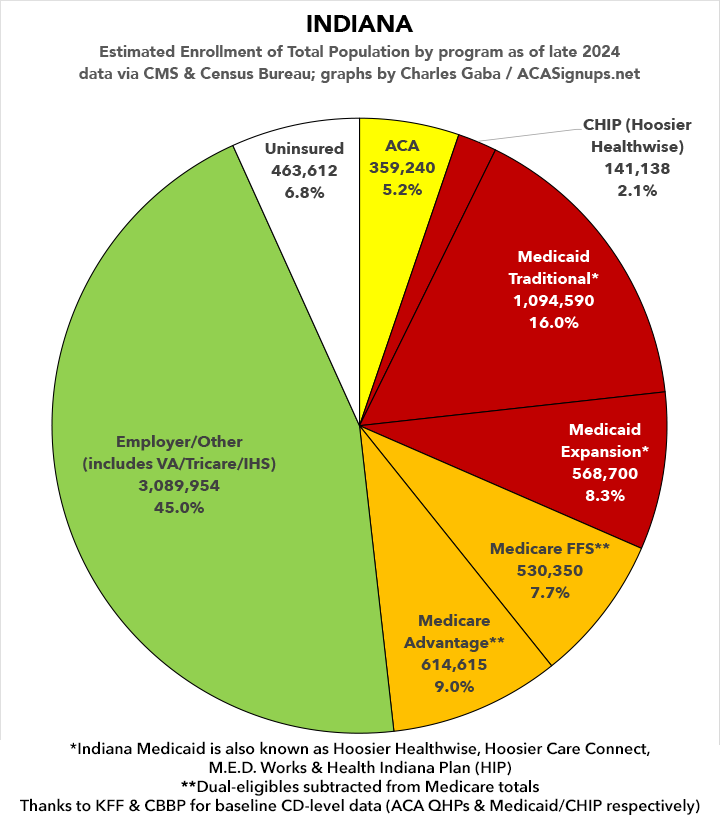

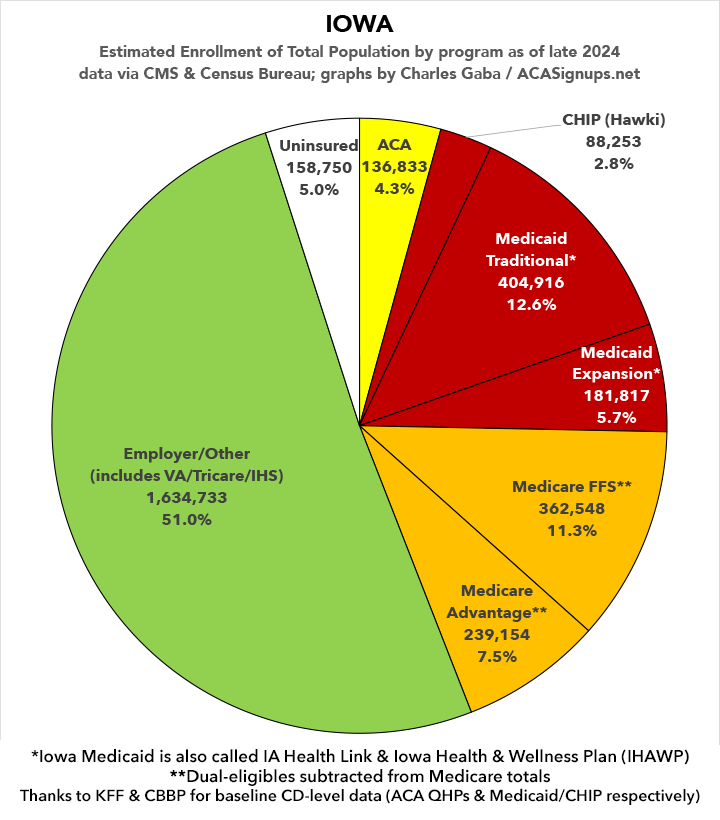

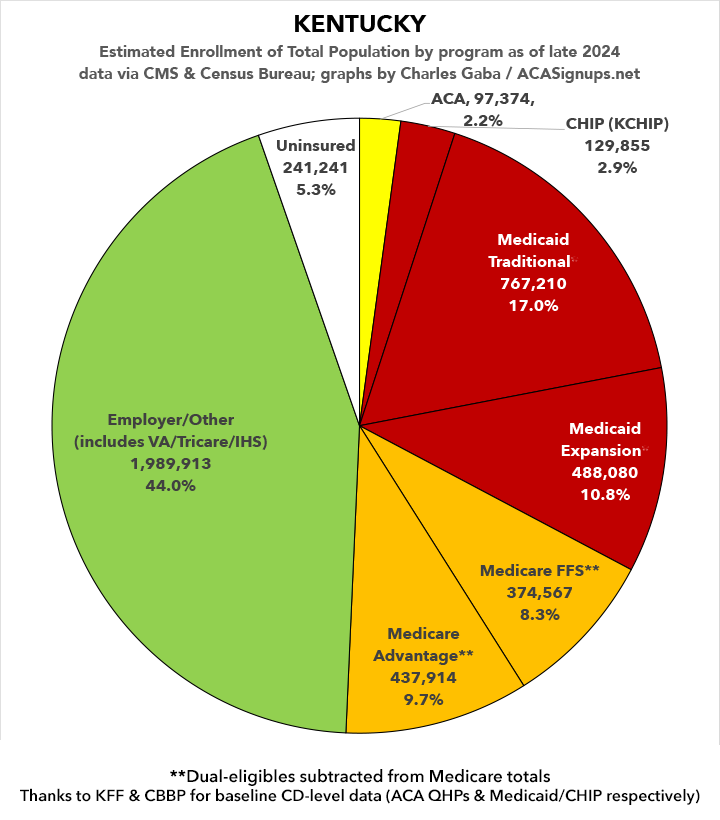

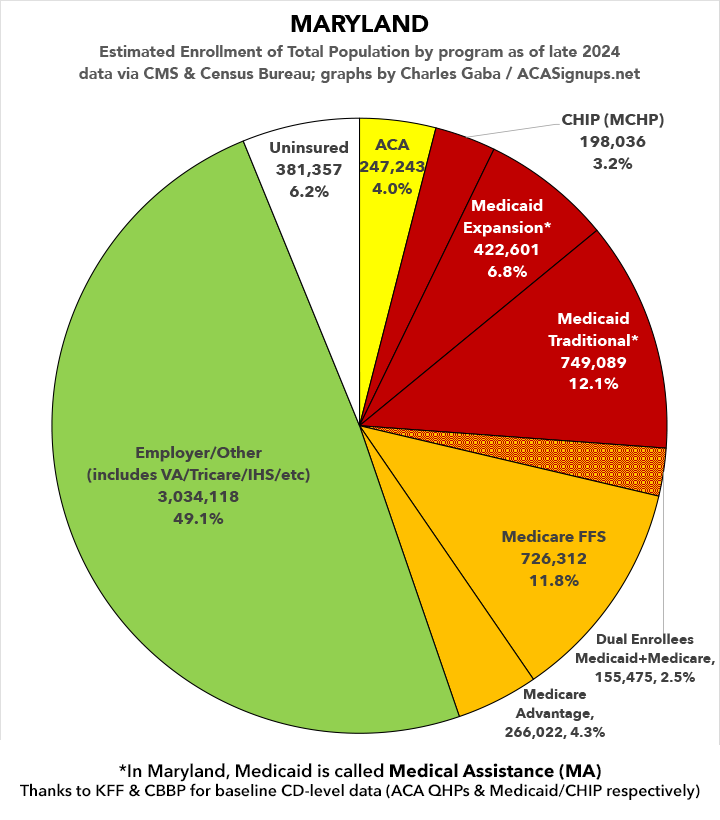

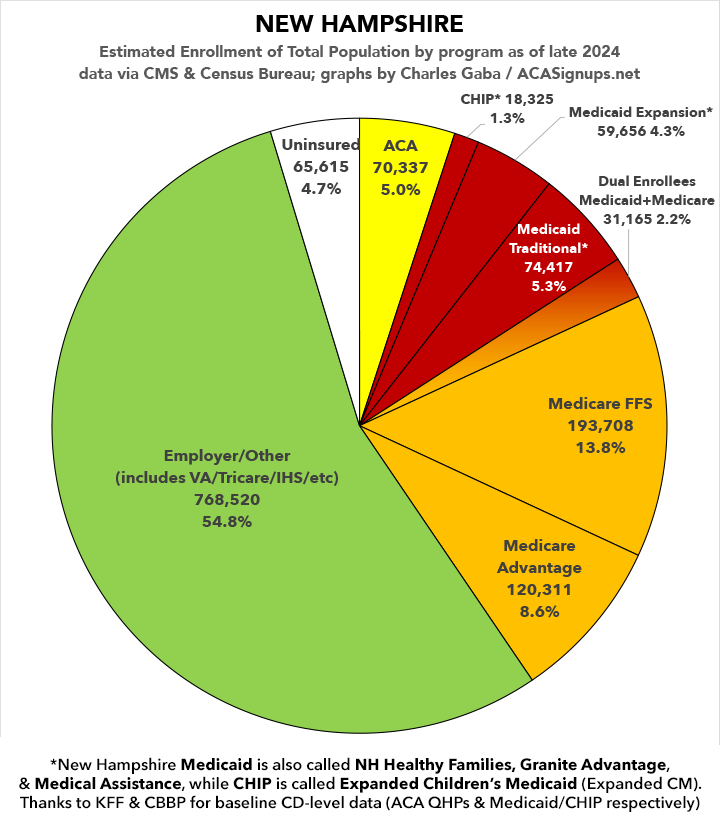

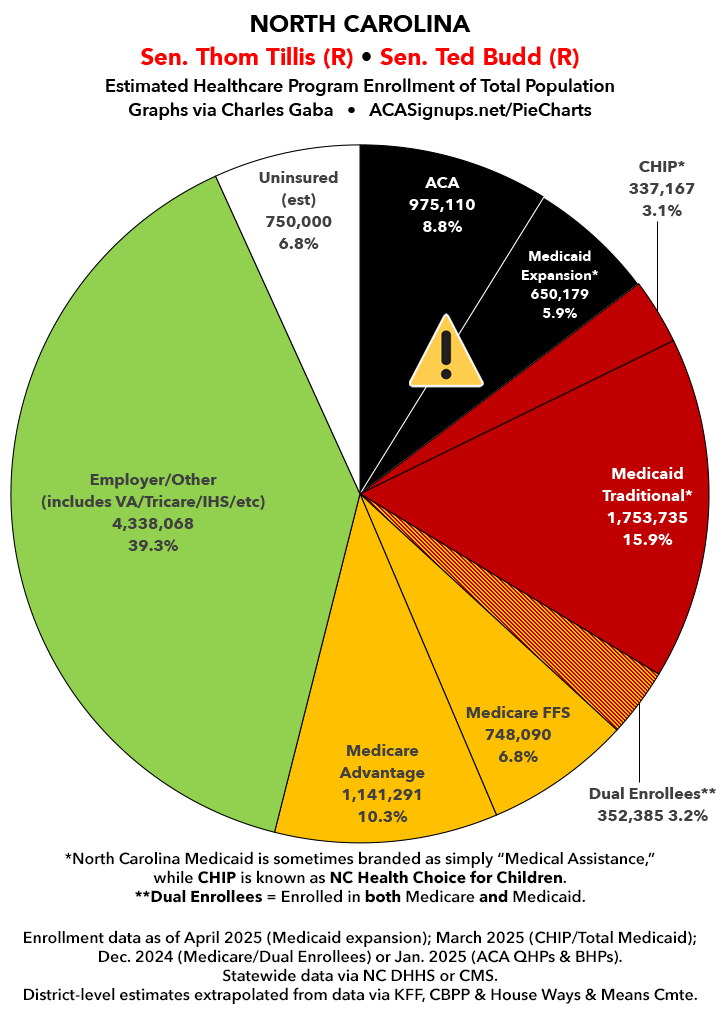

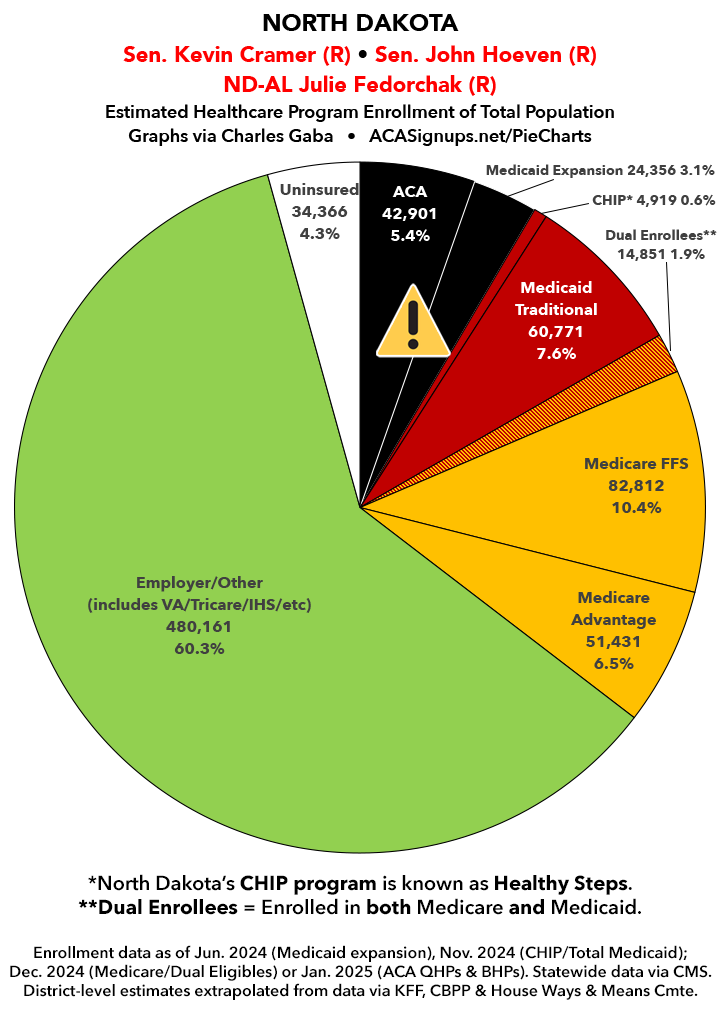

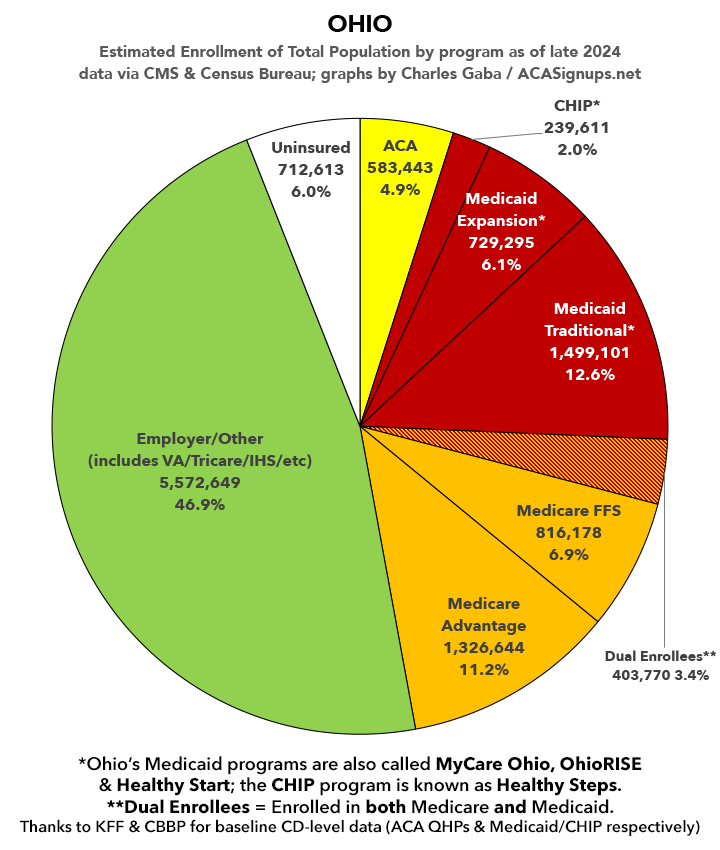

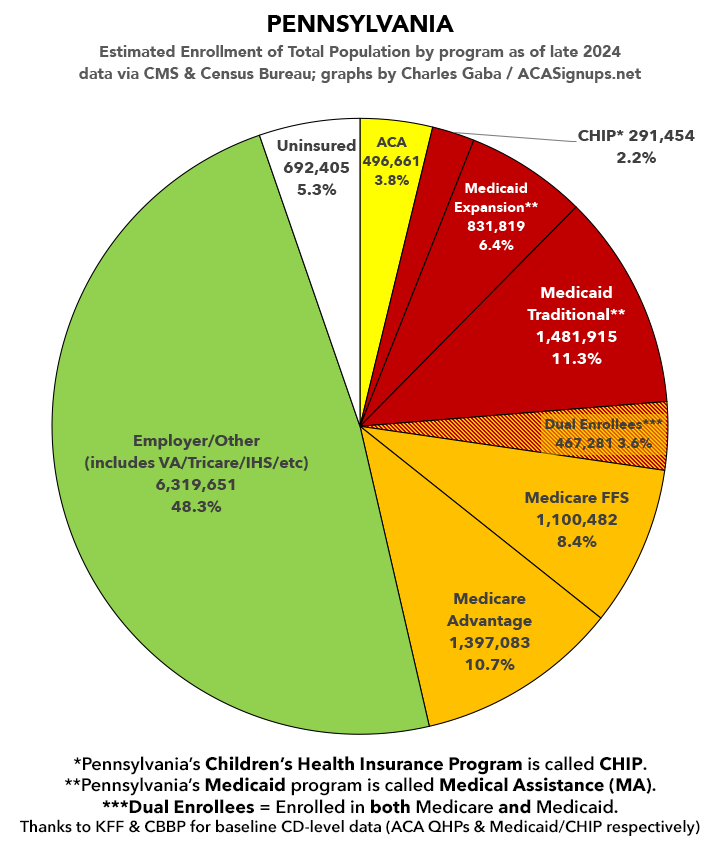

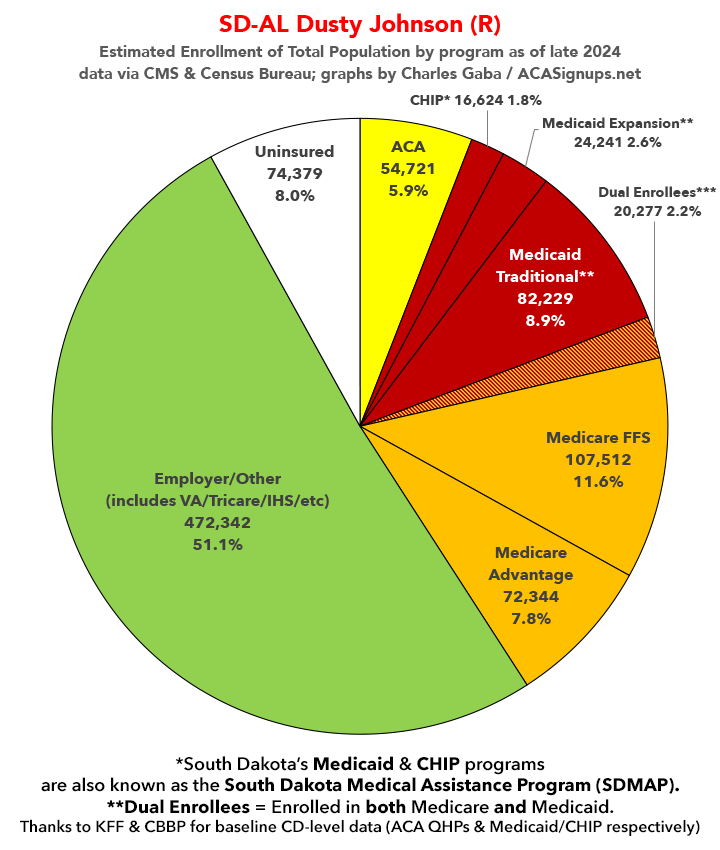

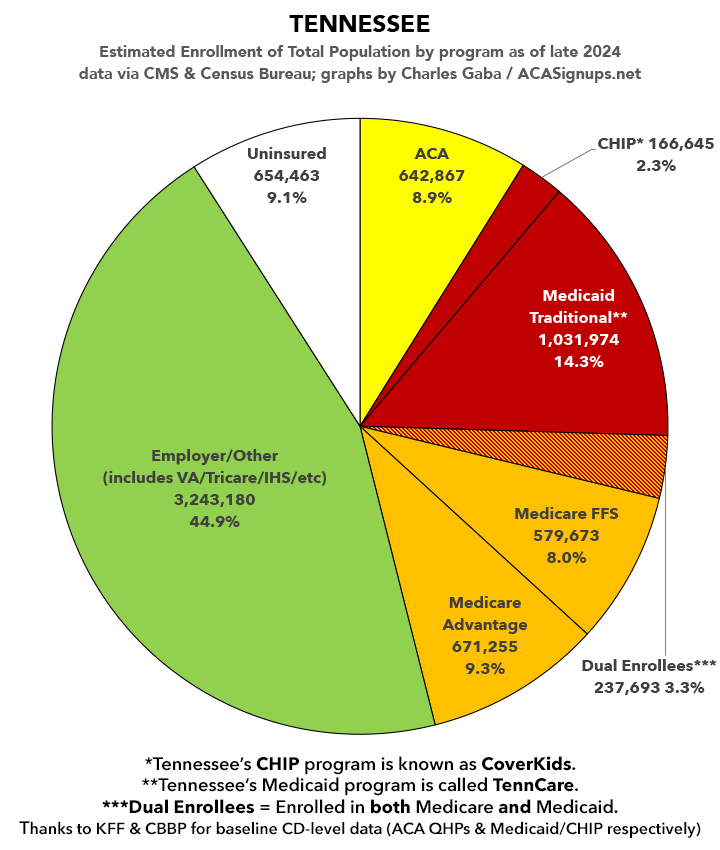

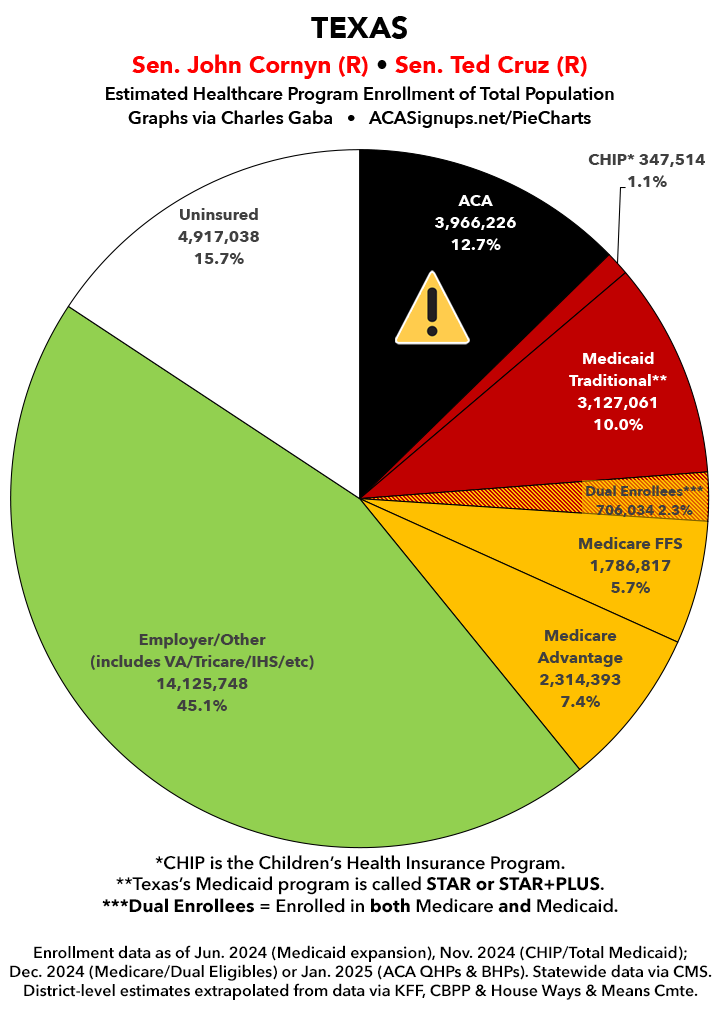

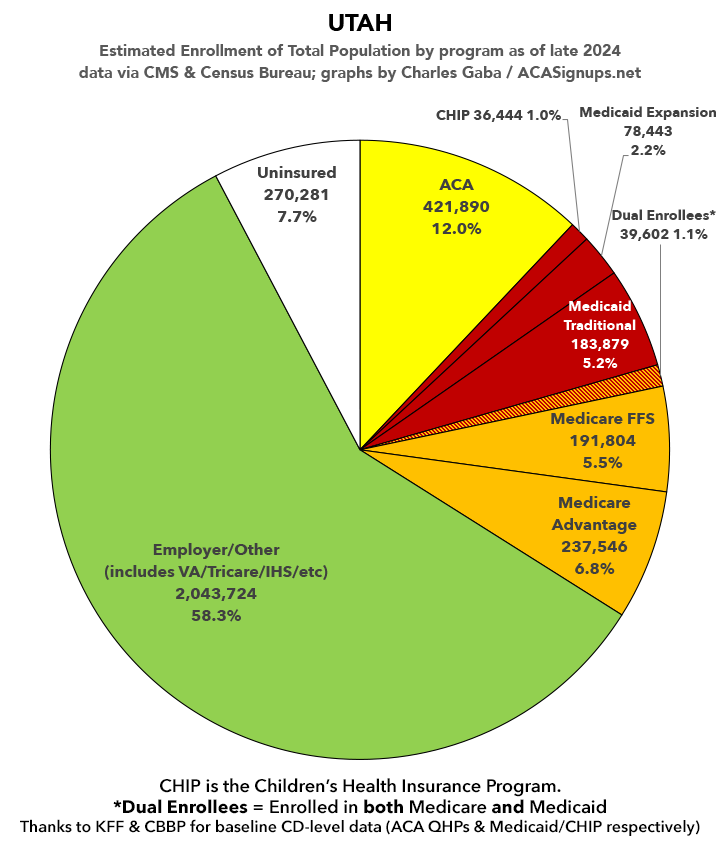

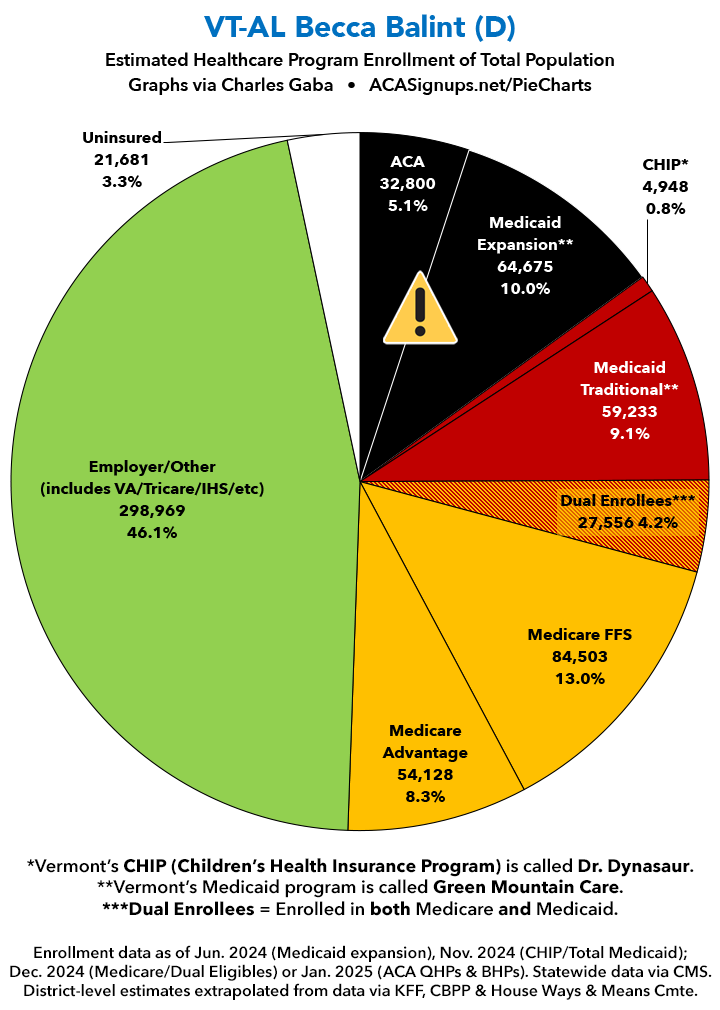

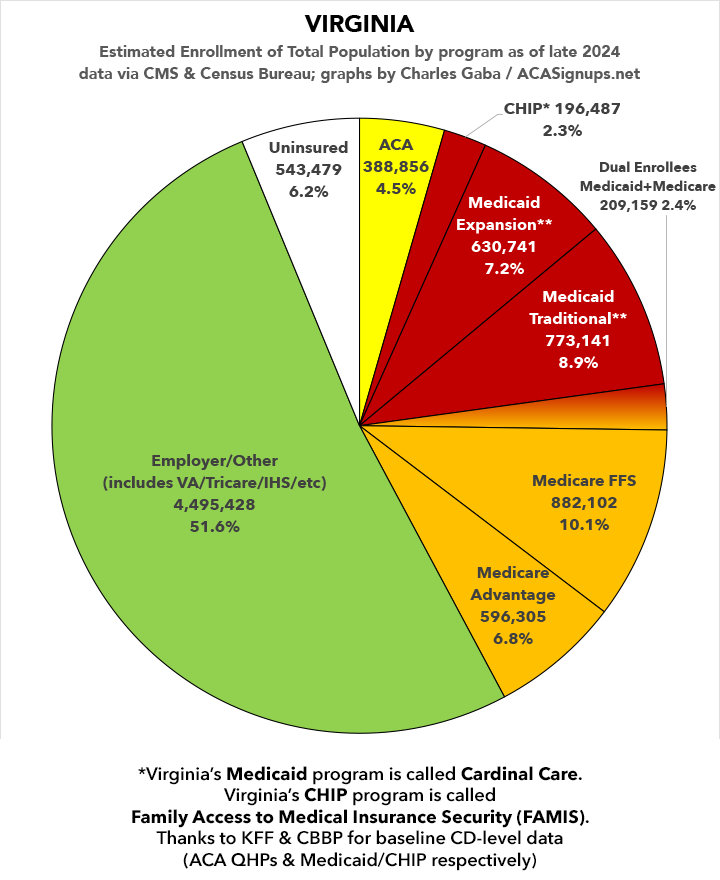

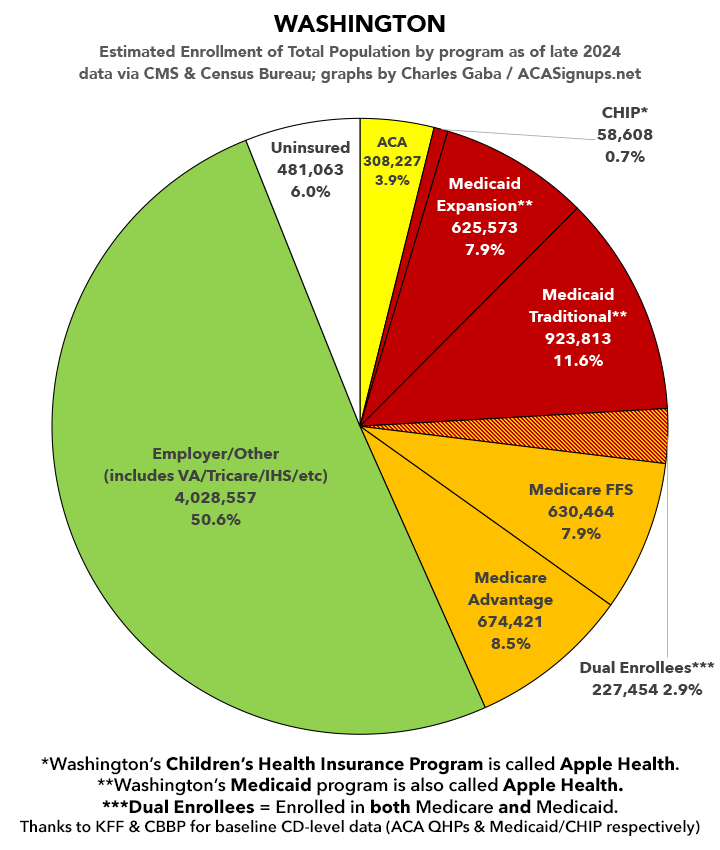

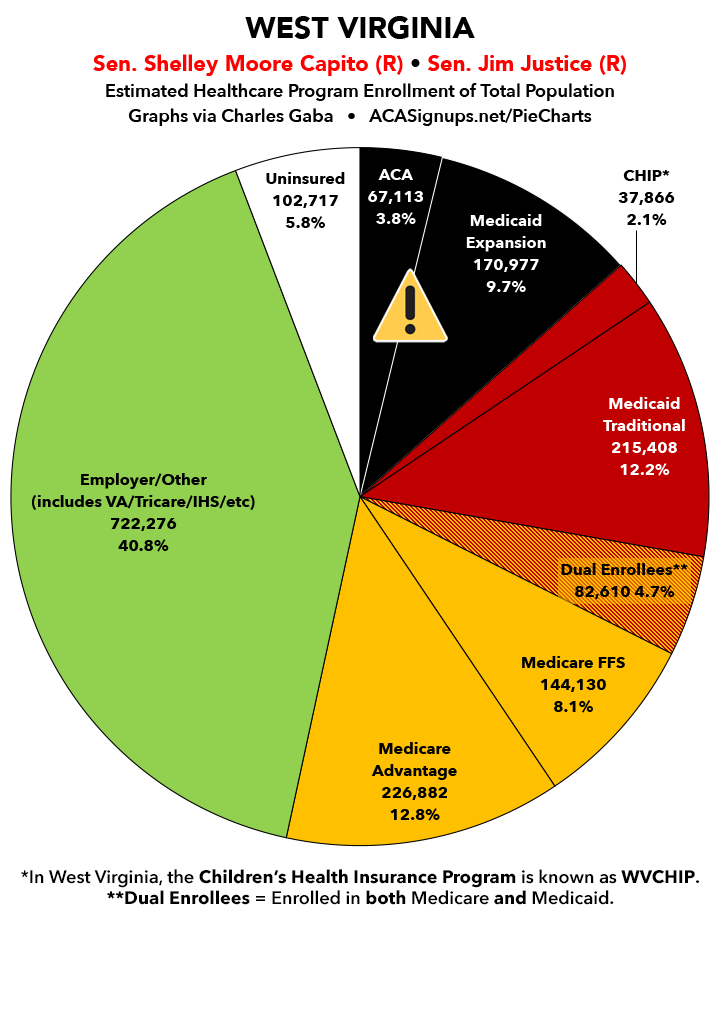

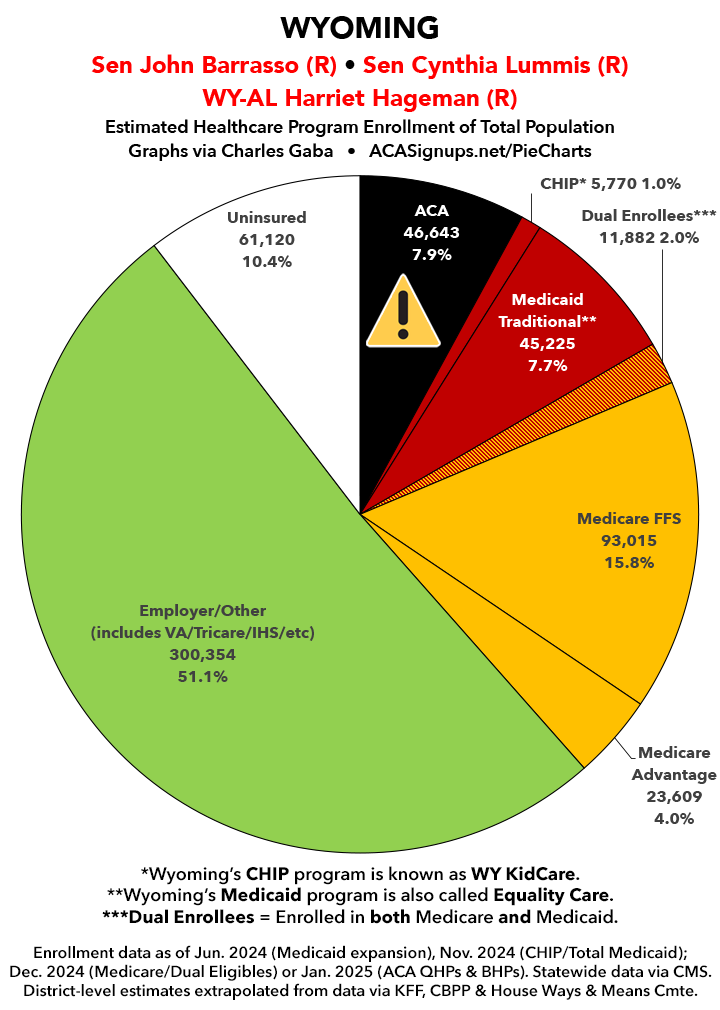

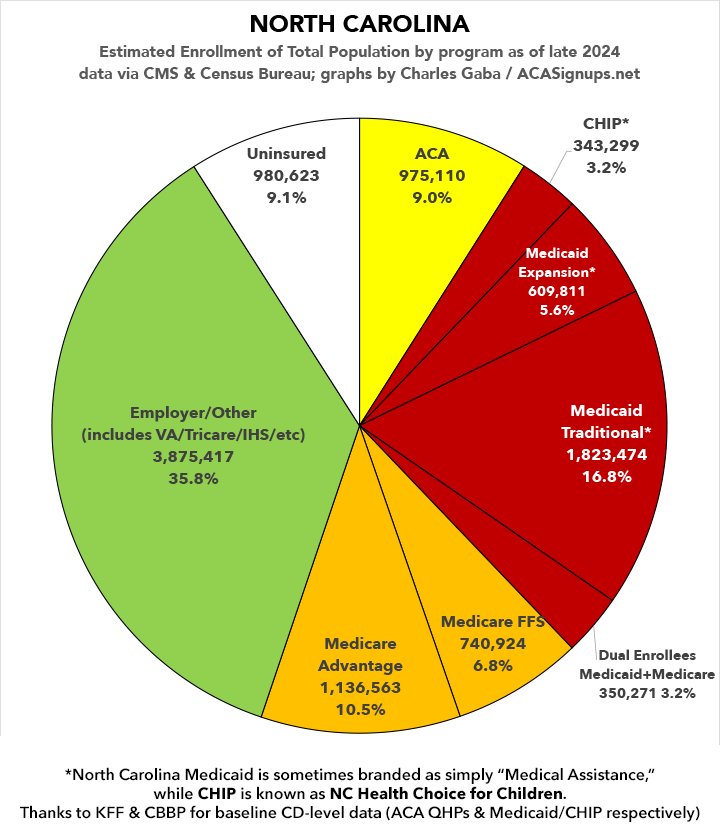

Meanwhile, below I've posted pie chart graphics highlighting just how many people are currently enrolled in both ACA exchange plans and ACA Medicaid expansion coverage. All told, they add up to over 45 MILLION Americans (or nearly 47 million if you also include Basic Health Plan enrollees in NY, MN & OR...but that gets a bit wonky & technical).

Find your state below & please share these graphics widely on social media!

{kind=link}

{kind=link}

Advertisement