Last week I broke the story (later picked up by Axios, NY Magazine and Vox.com) that the Graham-Cassidy bill would make thousands of current insurance policies illegal starting on January 1, 2018...just 98 days from now.

Why? Because, as noted at the link, while the current ACA structure (exchanges, tax credits, etc) would stay mostly in place for 2 more years, some provisions would be repealed immediately...including a nationwide ban on any exchange policy offering abortion coverage.

This morning JP Massar (who called my attention to the 1/1/18 effective date the first time) inquired as to whether that had changed with the new version of G-C. As you can see on pages 2 & 3 of the new bill...nope. It’s still in place.

Here's direct links to the bill itself and to the GOP's table showing what they claim would be the net federal funding changes from 2020-2026 for each state relative to current law...but they pulled one hell of a fast one.

it's pretty rare for the entire medical, hospital and insurance industry to agree on just about anything...and yet here we are (emphasis in the original):

The following statement was jointly released on September 23, 2017 by the American Medical Association, American Academy of Family Physicians, American Hospital Association, Federation of American Hospitals, America's Health Insurance Plans and the BlueCross BlueShield Association regarding the Graham-Cassidy-Heller-Johnson legislation.

We represent the nation's doctors, hospitals and health plans. Collectively, our organizations include hundreds of thousands of individual physicians, thousands of hospitals, and hundreds of health plans that serve tens of millions of American patients, consumers and employers every day across the United States.

Anyone who's followed me either here at ACASignups.net or over at Twitter over the past eight months knows that no one has been sounding the alarm louder or more frequently than me about both the real and potential sabotage of the ACA being carried out (or at least attempted) by the GOP in general and Donald Trump/Tom Price specifically. Hell, back in July, I even warned of a half-dozen things to look out for, several of which have since already been proven true:

This brings me to the main point of this entry: This is likely just the beginning. I'm not going to say that any or all of the following will happen--it's possible that Trump/Price/Verma will show some level of restraint--but I wouldn't be at all surprised to see any or all of these happen during this fall's Open Enrollment Period (which runs from Nov. 1st - Dec. 15th, by the way):

The past few weeks, while trying to push the Godawful "Graham-Cassidy" ACA repeal bill, Louisiana Republican Senator Bill Cassidy has used the following as one of his standard talking points:

.@BillCassidy shares the story of a Louisiana man paying more than $40,000 for his special needs son’s health care under Obamacare. pic.twitter.com/AaZ0IQIfF7

Credit where due. Last time around McCain made everyone hold their breath in suspense (then again, in his defense, he had just been diagnosed with a brain tumor and had to schlep all the way back from Arizona to DC for the vote a day or so earlier).

This time around he’s being more clear and up front about it: He says he likes the idea of the bill in general, and would be influenced by AZ Gov. Ducey’s support of it, but the process has stunk and continues to stink from top to bottom:

Seriously, good for him. He’s being quite clear about not just his decisions but his reasons...and while it would be nice if he opposed the bill on the merits (it stinks), his actual reasons make perfect sense as well.

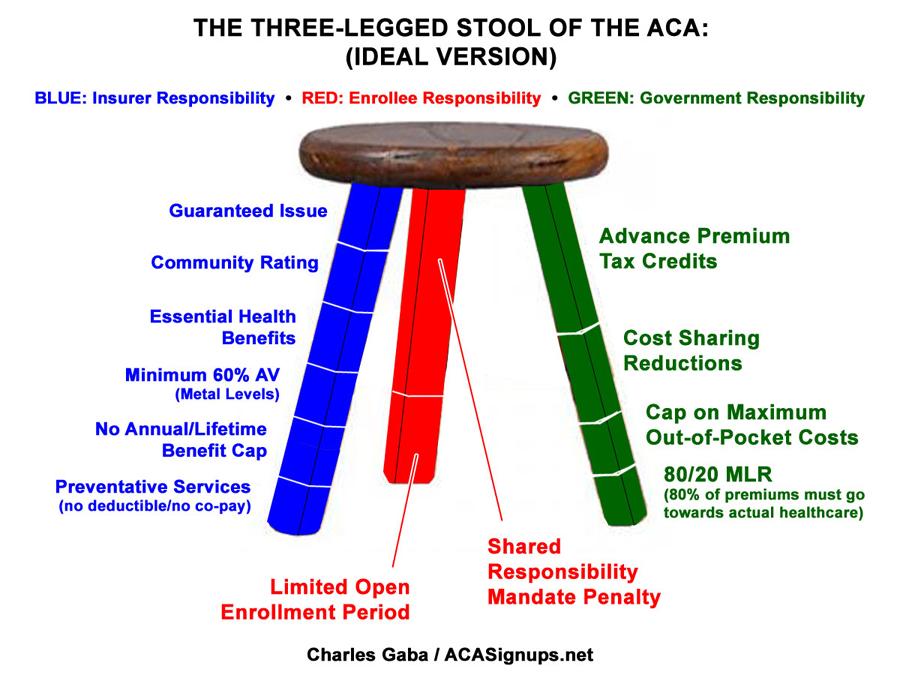

It's time to once again dust off the Three-Legged Stool visual aid to help explain just what the Graham-Cassidy bill would do to the individual insurance market. It's important to note that none of this has anything to do with Medicaid (expansion or traditional), the group market, Medicare and so forth; just the individual market.

Once again, here's what the "3-Legged Stool" was supposed to look like under the Affordable Care Act:

Here's what it actually looks like today, with some rather obvious gaps in the red (enrollee responsibility) and green (government responsibility) legs:

As the final deadline for final 2018 individual market rates to be locked in and the contracts signed, more states are coming into focus, and the pattern continues to be remarkably consistent.

In Mississippi, I originally pegged the requested rate hikes across the two individual market carriers (technically three, but "Freedom Life" is a phantom carrier with only 2 alleged enrollees) at 16.1% if CSR payments are made and 39.6% if they aren't. It turns out I was off by a bit, however, because I didn't realize that BCBS of Mississippi was only selling policies off-exchange next year. That means the CSR issue won't impact them either way, since none of their enrollees would receive the assistance anyway.

Alaska (along with Hawaii) will continue to receive Obamacare’s premium tax credits while they are repealed for all other states. It appears this exemption will not affect Alaska receiving its state allotment under the new block grant in addition to the premium tax credits.

Delays implementation of the Medicaid per capita caps for Alaska and Hawaii for years in which the policy would reduce their funding below what they would have received in 2020 plus CPI-M [Consumer Price Index for Medical Care].

Provides for an increased federal Medicaid matching rate (FMAP) for both Alaska and Hawaii."

Well, now.

Bird doesn't have the actual legislative text, but they threw Hawaii in there as well (not to win their votes...Dems Brian Schatz and Mazie Hirono are solid NOs no matter what). That means that the wording is probably along the lines of:

The Congressional Budget Office stated that they won't be able to provide a full score of the projected 10-year impact of the Graham-Cassidy bill for "at least several weeks". Instead, they expect to provide a partial score, focusing purely on the budget-related stuff necessary to "count" towards Senate reconciliation voting rules "early next week".

What won't be included are some pretty damned important details, like:

Impact on the federal deficit

Impact on insurance premiums, and of course...

Impact on the number of people with health insurance coverage

Unfortunately, Mitch McConnell and Senate Republicans are insisting on squeezing the vote on Graham-Cassidy through within the next 10 days, before the fiscal year ends on Sept. 30th, since that's the only way they have a chance at passing it using 50 votes (after the 30th, they would require 60 votes, which of course they have no chance at getting).