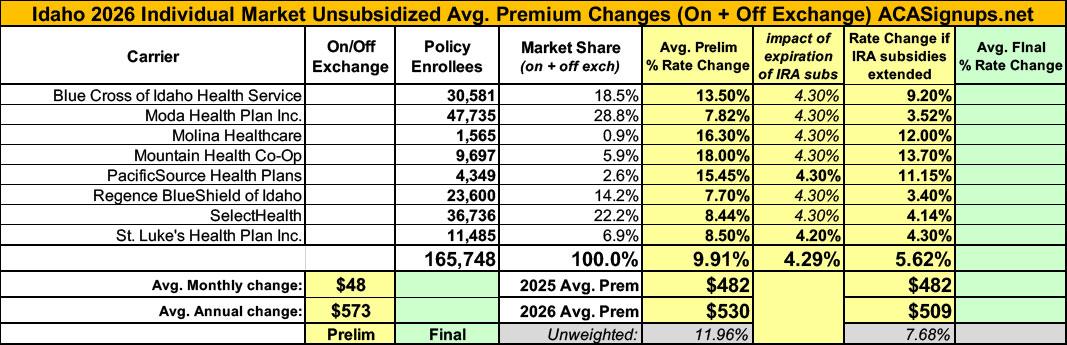

2026 Rate Changes - Idaho: +9.9%, but ~165,000 enrollees are likely looking at much higher net rate hikes.

Sun, 08/03/2025 - 4:58pm

This is the summary page for 2026.

The Department of Insurance receives preliminary health plan information for the following year from insurance carriers by June 1 and reviews the proposed plan documents and rates for compliance with Idaho and federal regulations.The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

A key driver of increases is generally the level of health claims paid compared to the premium collected. The table below shows the level of claims paid and premium collected by each insurance company for ACA-compliant health benefit plans during 2024. In addition to claims paid, the premium needs to cover the company’s administrative costs, insurance fees, and taxes. Those costs generally consume around 20 percent of the premium. Larger rate increases may be needed when the prior year’s premium is not sufficient to pay for health claims and administrative costs and fees.With its rate increase submission, each insurance company submits a consumer-oriented explanation of the increase, which is available by clicking on the name of the insurance company in the table below.

Each health benefit plan has an associated “metal level” of Bronze, Silver, Gold, or Catastrophic and offers, at a minimum, Idaho's Essential Health Benefits package.The metal level is assigned based on the policyholder's "cost-sharing," which includes any deductibles, coinsurances, copays, and out-of-pocket maximums. A Silver plan usually will have lower cost-sharing than a Bronze plan, and a Gold plan will usually have lower cost -sharing than a Silver plan.However a Gold plan usually has a higher monthly premium than a Silver plan, and a Silver plan usually has a higher monthly premium than a Bronze plan. Policyholders are able to choose which metal level and which plan within that metal level best works for them.

Blue Cross of Idaho Health Service Inc:

Reason for Rate Increase(s):

- Medical Inflation: (Cost per instance of type of service) increase due to contract and fee schedule changes.

- Increased Utilization: The usage of services is expected to be different in the projection period than in the experience period.

- Benefits have been changed in the products offered in the effective period due. Changes have been made to allow products to meet the metallic tier requirements of the ACA. Other changes have been made to meet expected market demands and state regulatory requirements.

- Changes in Taxes and Fees.

- Market wide increase in morbidity due to the expiration of the enhanced premium tax credit

For 2026, there are 55 renewing plans introduced as new before 2026, 7 plans being discontinued, and 16 new plans being introduced. Benefit changes and cost sharing changes exist on the renewing plans to maintain regulatory compliance and account for medical cost and utilization when comparing the experience period to the projection period. Impacts will vary by plan. The rate changes in this filing do not affect rate changes for grandfathered or the transitional products.

Changes in the Morbidity of the Population Insured:

The morbidity in the 2026 projected population is expected to differ from the experience period population due to the expiration of enhanced premium tax credit. It is anticipated that members may leave the market due to expiration of the enhanced premium tax credits. Without additional data, it is unclear what portion of the population and their related morbidity will remain in the market. It has been assumed all other differences in the morbidity of this population have been captured in either experience period claims data or in risk adjustment transfers. The expectation is that these individuals have a morbidity similar to that of the historical single risk pool. Insufficient data exists to determine which Special Enrollment Period (SEP) enrollees purchased coverage due to Medicaid redetermination or purchased coverage due to other SEP qualifying events.

Molina Healthcare of Idaho:

Molina retained Milliman to analyze the impact of expiring premium subsidies on statewide morbidity. We reviewed the study and determined that the best estimate for an acuity adjustment is [REDACTED] Please refer to Appendix Exhibit [REDACTED]

PacificSource Health Plans:

Medical inflation, an increase in risk margin, and the impacts of the expiration of enhanced premium subsidies are the primary sources of PacificSource's 15.45% rate change. Rate changes will vary by plan due to plan-specific benefit and pricing adjustments. Rate changes will vary by rating area due to changes to rating area factors. For more information, see Appendix B. The rate change reported in the Unified Rate Review Template is 15.58%, which is weighted by membership and premium and only includes the impact of members on renewing plans.

...The expiration of enhanced subsidies is expected to cause anti-selective market shrinkage. To account for this, a factor of 1.043 is required.

Regence BlueShield of Idaho:

Additionally, this scenario considers the enhanced level of uncertainty resulting from the combined effects of the enhanced premium tax credits expiring, premium tax credit impacts of CSR funding resumption, and the other provisions in the Marketplace Integrity rules and federal Reconciliation Bill that make coverage more difficult to obtain.

SelectHealth:

The significant drivers affecting the change in rates are:

- Single pool experience

- Utilization and Inflation

- Changes to benefits

- Expiration of Enhanced Subsidies

- Changes to the Idaho High Risk Pool Reinsurance program

For carriers which don't publicly clarify how much the IRA subsidies expiring are impacting unsubsidized rate changes I'm substituting the CBO's projection of 4.3% for 2026 from last December.

It's important to remember that these are just for unsubsidized, full price premiums. The impact on net rate hikes for the vast majority of ACA exchange enrollees will be much higher than 9.9%.

| Attachment | Size |

|---|---|

| 124.26 KB | |

| 497.3 KB | |

| 559.94 KB | |

| 107.64 KB | |

| 96.04 KB | |

| 83.77 KB | |

| 388.21 KB | |

| 100.99 KB |

Advertisement