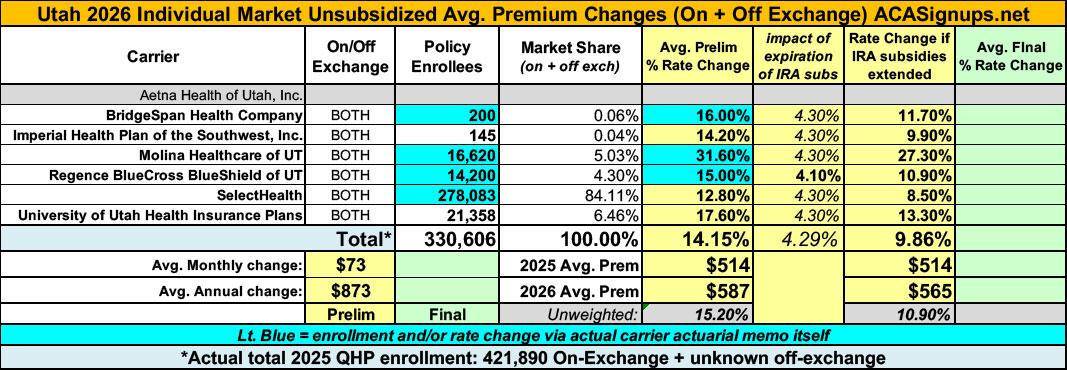

2026 Rate Changes - Utah: +14.2%; ~421,000 enrollees looking at massive rate hikes

Mon, 08/04/2025 - 5:40pm

BridgeSpan Health Co:

The projected average rate change for plans effective January 1, 2026 is 16.0% which is an average rate change of about $87 per member per month (pmpm). Because 16.0% (or about $87) is an average, it is possible to have a different rate change. Factors affecting a member's premium are age, tobacco use, family composition, plan, and geographic area. Expected cost differences by product are updated every year to ensure premium differences are appropriate. BridgeSpan has approximately 200 members enrolled in this line of business as of March 2025.

...The rate change described above is driven by the following factors:

- Medical Trend : 9.1%

- Change in Benefits, Age, Area, and Network : -1.5%

- Change in Market Morbidity : 5.0%

- Exchange User Fees : 1.0%

- Other : 2.0%

Other includes: actual results vs. expected, changes to admin expenses, and rx rebates. Actual results vs. expected reflect differences between actual results and past assumptions, including a true-up of market morbidity estimates

Molina Healthcare of Utah:

1. Scope and range of the rate increase: Molina’s proposed rates represent an average rate change of 31.6% for the 16,620 Molina members enrolled in continuing plans effective April 2025. The proposed rate changes vary by metal tier. Members would receive premium changes ranging from 21.1% to 35.8% depending on their plan, geographic location, and age.

2. Financial experience of the product: Baseline claims experience was used from Molina’s 2024 Utah Marketplace business. 2024 Utah premium of $609.65 per member per month and risk adjustment transfers of $29.42 per member per month were received compared to allowed claims of $656.36 per member per month.

The proposed premium rates yield a medical loss ratio of 87.8%. The medical loss ratio represents the percentage of every premium dollar that Molina expects to spend on medical expenses and improving health care quality for our members. The projected medical loss ratio of 87.8% exceeds the Affordable Care Act minimum required loss ratio of 80.0%.

3. Changes in Medical Service Costs: Medical inflation related to the utilization and cost of covered services increased claims by 10.6% per year on average between 2024 and 2026. Trend is one of the primary contributors to an increase in rates. Changes in provider contracting rates also contributes significantly to the overall and regional rate changes.

4. Changes in Benefits: Molina is renewing 7 gold and silver plan offerings from 2025. The impact on rates from benefit design changes for all renewal plans is minimal.

5. Administrative Costs and Anticipated Profits: Total administrative expenses are expected to decrease, contributing to a decrease in rates of approximately 0.4%, slightly dampening the overall impact of rate increases from other rate increase components. Targeted profit margin remains the same as the prior year’s filing.

6. Program Changes: The expiration of the enhanced Premium Tax Credits (eAPTCs) and Program Integrity will lead to people leaving Marketplace, with a higher skew of healthier people leaving and therefore driving up the acuity in the risk pool.

Regence BlueCross BlueShield of Utah

The projected average rate change for plans effective January 1, 2026 is 15.0% which is an average rate change of about $86 per member per month (pmpm). Because 15.0% (or about $86) is an average, it is possible to have a different rate change. Factors affecting a member's premium are age, tobacco use, family composition, plan, and geographic area. Expected cost differences by product are updated every year to ensure premium differences are appropriate. Regence has approximately 14,200 members enrolled in this line of business as of March 2025.

The rate change described above is driven by the following factors:

- Medical Trend : 9.1%

- Change in Benefits, Age, Area, and Network : -1.8%

- Change in Market Morbidity : 5.0%

- Exchange User Fees : 1.0%

- Other : 1.3%

Other includes: actual results vs. expected, changes to admin expenses, and rx rebates. Actual results vs. expected reflect differences between actual results and past assumptions, including a true-up of market morbidity estimates.

SelectHealth:

SelectHealth is offering products in the Individual ACA plan market in 2026. These plans will be available across all counties in Utah. The requested rate change will impact approximately 278,083 members and will vary depending on selected benefit, network, member’s age and geographic area. The 2026 average rate change is an increase of 12.8% with a minimum rate change of 9.2% and a maximum increase of 18.6%.

University of Utah Health Insurance Plans:

Section 2 – Scope and Range of Rate Increases

The overall weighted average 2026 premium rate increase is 17.6% for the 21,358 members enrolled in continuing plans. The proposed rate changes vary by metal tier and network. Members would receive premium rate changes ranging from 7.2% to 27.1% depending on their metal tier and network.

Section 3 – Financial Experience of the Product

For the most recent completed benefit year (2024), the total premium revenue was $568 per member per month (PMPM) plus $168 in risk adjustment premium revenue. The incurred medical claims were $711 prior to administrative costs, producing a near breakeven Medical Care Ratio. Considering the rate increase for 2025, expected trends between 2024 and 2026, and impact from the expected ending of expanded subsidies, the premium increases are expected to keep the product in a net positive income position.

Section 4 – Changes in Medical Service Costs

The biggest factor in the rate increase is the increased claim costs and expected impact from the expected ending of expanded subsidies. UUHIP expects an average annual claim trend of 9.8% over the next two years.

Section 5 – Changes in Benefits

The plan benefits were changed to comply with allowed ranges in actuarial values (AV). The increase or decrease in AV is a factor in the rate increase or decrease. The AV change is not a large factor in the overall rate increases.

Section 6 – Administrative Costs and Anticipated Margins

The administrative costs assumptions and anticipated margins have not increased as a percentage of claims from the prior filing and are not a significant factor in the rate increases.

Note: The requested rate changes as well as the enrollment numbers vary between the Utah Insurance Dept. and federal Rate Review website filings, which are in light blue.

For carriers which don't publicly clarify how much the IRA subsidies expiring are impacting unsubsidized rate changes I'm substituting the CBO's projection of 4.3% for 2026 from last December.

It's important to remember that these are just for unsubsidized, full price premiums. The impact on net rate hikes for the vast majority of ACA exchange enrollees will be much higher than 14.2%.

Advertisement