As I noted a few weeks ago, I haven't written a whole lot about the idiotic (but terrifyingly so) TexasFoldEm lawsuit in awhile. Part of this is because I was out of the country over the holidays; part is because there hasn't been a whole lot of movement on the case since right-wing federal Judge Reed O'Connor ruled that the ACA was unconstitutional using a legal argument so thin it hula hoops with a Cheerio.

Covered California Plan Selections Remain Steady at 1.5 Million, but a Significant Drop in New Consumers Signals Need to Restore Penalty

Covered California finishes open enrollment with 1.5 million plan selections, which is virtually identical to 2018’s total, despite federal changes.

A key reason for the steady enrollment is that more people entered the renewal process for 2019 coverage after a strong enrollment period for 2018.

The federal removal of the individual mandate penalty appears to have had a substantial impact, leading to a decrease of 23.7 percent in new enrollment.

SACRAMENTO, Calif. — Covered California announced that more than 1.5 million consumers selected a health plan for 2019 coverage during the most recent open-enrollment period, a figure in line with last year’s total. There was a 7.5 percent increase in the number of existing consumers renewing their coverage and a 23.7 percent drop in the number of new consumers signing up for 2019.

We propose a premium adjustment percentage of 1.2969721275 for the 2020 benefit year, including a proposed change to the premium measure for calculating the premium adjustment percentage. Under §156.130(e), we propose to use average per enrollee private health insurance premiums (excluding Medigap and property and casualty insurance), instead of employer-sponsored insurance premiums, which were used in the calculation for previous benefit years, for purposes of calculating the premium adjustment percentage for the 2020 benefit year. The annual premium adjustment percentage sets the rate of increase for several parameters detailed in the PPACA, including: the annual limitation on cost sharing (defined at §156.130(a)), the required contribution percentage used to determine eligibility for certain exemptions under section 5000A of the Code (defined at §155.605(d)(2)), and the employer shared responsibility payments under sections 4980H(a) and 4980H(b) of the Code.

Here's what this seeming gobbledygook means, as explained by Matt Fiedler of the Brookings Institute:

The midterms are over, and the Democrats won back the U.S. House, so the ACA is (mostly) safe at last, right?

Well...maybe. In addition to the ongoing regulatory sabotage by the Trump Administration to undermine, weaken and generally piss all over the law as much as possible, there's also still a little thing called Texas vs. Azar, aka the #TexasFoldEm federal lawsuit. Oral arguments were held way back in early September, and right-wing Judge O'Connor claimed that he'd rule on a preliminary injunction "quickly" afterwards.

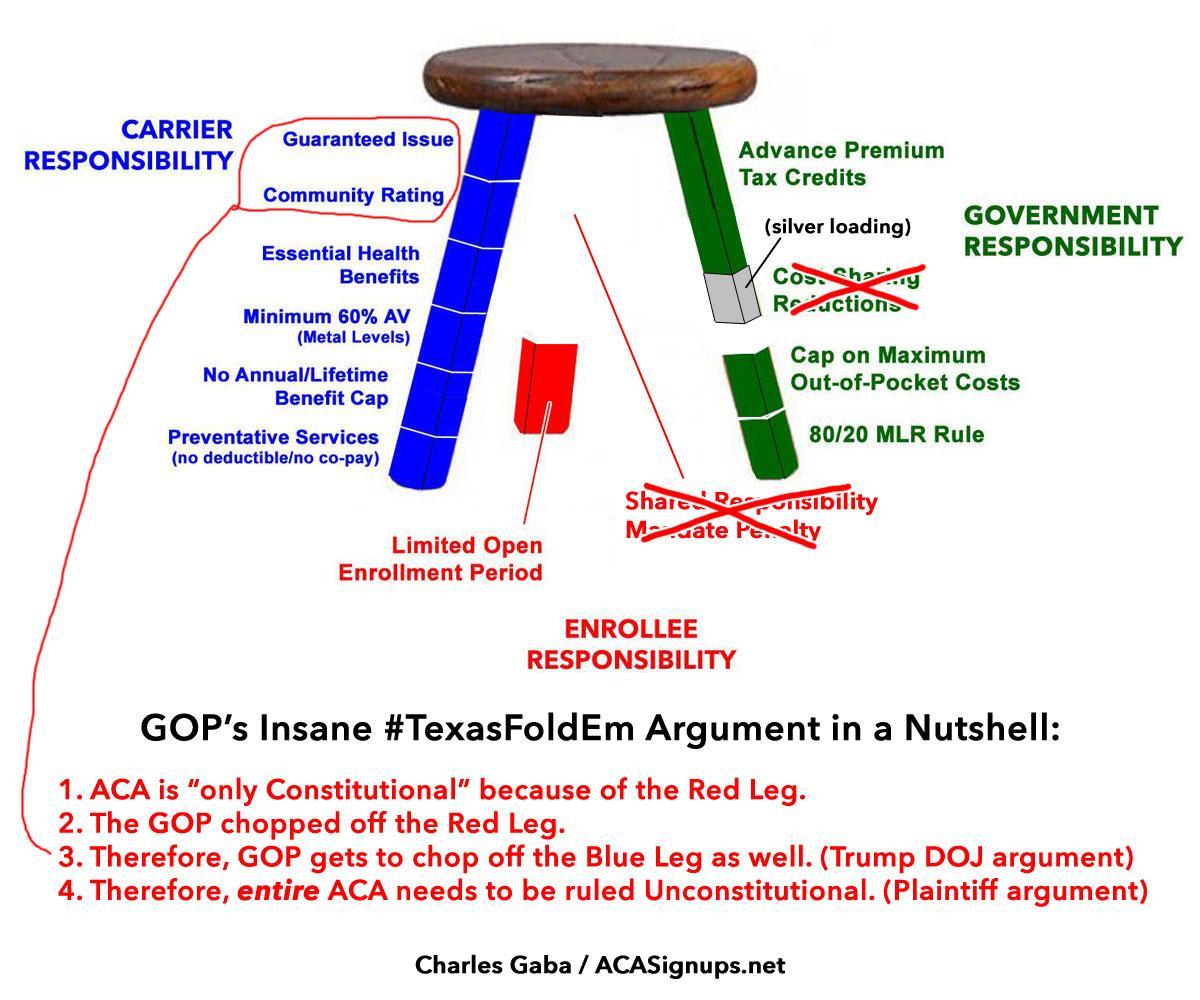

As a reminder, here's the #TexasFoldEm case in a single image:

Michigan was pretty much Ground Zero for the 2018 Blue Wave midterm elections. In addition to Democrats flipping the Governor's seat (and holding onto Debbie Stabenow's U.S. Senate seat), they also flipped the Attorney General, Secretary of State, one of two state Supreme Court seats, both of the stateBoard of Education seats which were up and all six state University Board seats which were up. In addition, they picked up two U.S. House seats, five state Senate seats and five state House seats.

It was a complete and utter repudiation of both Republican governance and their agenda.

As Democratic candidates prepare to take three statewide offices on Jan. 1 — governor, attorney general and secretary of state — Republican lawmakers introduced bills Thursday to challenge their authority.

A month ago I posted a Red Alert about the latest regulatory attack on the ACA...this time coming directly from CMS Administrator Seema Verma. At the time, Verma had just announced a draft version of the new rules for Section 1332 Waivers...starting with changing the name from "State Innovation Waivers" to "State Relief and Empowerment Waivers", which sounds in no way like Orwellian doublespeak propaganda.

Here's the basic backstory on 1332 waivers:

One of the great strengths and dangers of the ACA is that it includes tools for individual states to modify the law to some degree by improving how it works at the local level. The main way this can be done is something called a "Section 1332 State Innovation Waiver":

The midterms are over, and the Democrats won back the U.S. House, so the ACA is (mostly) safe at last, right?

Well...maybe. In addition to the ongoing regulatory sabotage by the Trump Administration to undermine, weaken and generally piss all over the law as much as possible, there's also still a little thing called Texas vs. Azar, aka the #TexasFoldEm federal lawsuit. Oral arguments were held way back in early September, and right-wing Judge O'Connor claimed that he'd rule on a preliminary injunction "quickly" afterwards.

Well, today is November 18th, and there's been nary a peep from Judge O'Connor. Does 75 days later count as "quickly"? In judiciary time, I suppose it might.

With the 2018 Midterm Elections mostly out of the way (there's still at least 7 statewide races which haven't been called yet in Georgia, Florida and Arizona which are currently in the process of various counts, recounts and/or run-off elections), the Democratic Party has indeed retaken the U.S. House of Reprentatives by a solid margin, adding anywhere from 33 - 40 House seats when they only needed a net gain of 23 to take control. Starting in January, the House Democrats will be able to vote on and pass pretty much whatever bills they want, presumably under the leadership of Nancy Pelosi as Speaker of the House.

In U.S. politics, the Hyde Amendment is a legislative provision barring the use of federal funds to pay for abortion except to save the life of the woman, or if the pregnancy arises from incest or rape. Legislation, including the Hyde Amendment, generally restricts the use of funds allocated for the Department of Health and Human Services and consequently has significant effects involving Medicaid recipients. Medicaid currently serves approximately 6.5 million women in the United States, including 1 in 5 women of reproductive age (women aged 15–44).