Axios: GOP considering both of my tax credit ideas...but only for two years? FORGET IT.

Mon, 09/22/2025 - 10:42am

Last week I urged Democrats to demand Congressional Republicans rein in the Trump Regime's out-of-control dictatorial rampage as well as going big on healthcare policy as part of the "government shutdown" battle...but that to the extent that they do make the main focus healthcare policy, at the very least to not settle for simply bumping out the enhanced ACA tax credits by a year or two:

You know I'm a pretty mainstream Democrat. I'm not demanding Medicare for All here. What I am urging on the healthcare front is for three clear demands:

- Restore the massive funding cuts to the NIH & other critical medical/scientific departments of the federal government;

- Repeal the draconian cuts to Medicaid (especially the disaster-as-a-feature-waiting-to-happen "work reporting requirements;" and...

- Make the enhanced ACA premium tax credits (eAPTC) permanent so we can avoid this Sword-of-Damocles worry which is paralyzing carriers, providers and enrollees every few years.

At a bare, bare minimum, do not settle for a one- or two-year extension of the eAPTCs.

Kicking this particular can down the road for only one or two years would not only be an absolute gift to Republicans politically (since it would push the pain out until just past the midterms, which is of course the only reason why any Republicans are willing to discuss doing so at all), but it would also mean we'd be right back here with the exact same scary headlines a year or two from now, with 24 million people never knowing whether their health insurance premiums are going to skyrocket from year to year.

To their credit, the official counteroffer continuing resolution offered up by House & Senate Democrats included all of the above as well as a slew of provisions which would theoretically end and reverse many (most?) of Trump's illegal actions when it comes to how federal dollars are spent.

I then went on to state that when it does come to ACA tax credits specifically, there is some wiggle room for debate which I could see happening:

For instance: One legitimate criticism of how the ACA functions which was first reported on by Julie Appleby of KFF has been the rise of broker fraud, in which unscrupulous health insurance brokers have apparently been secretly either enrolling people into ACA exchange plans without the enrollee's knowledge or permission, or switching them from one plan to another without their knowledge/permission, in order to pocket the commission.

I went on to note that the federal & state exchanges have already started imposing measures to crack down on this problem, but that to the extent that it really is an issue...

One possible thing I could see Dems agreeing to would be to add a $1/month minimum net premium regardless of how much in APTC enrollees are otherwise eligible for. I'm not saying I'd be thrilled with this, but I could see that winning over support.

The point of doing this wouldn't be the actual dollar amount; in theory it could be literally a penny per month. The point is that this would guarantee that the policy enrollee receives an actual invoice each month so that they're aware that they're enrolled in an ACA exchange healthcare policy, as well as knowing what carrier that policy is with.

Well, according to Axios this morning, this may very well be under consideration after all:

Republican senators are having early discussions about modifying enhanced Affordable Care Act tax credits to allow for an extension of the subsidies before they expire at year's end.

...Sen. Mike Rounds (R-S.D.) said one modification Republicans have discussed is requiring ACA enrollees to have "skin in the game" by making them pay a minimum premium and barring zero-premium plans that are ACA-compliant but that critics contend fuel fraud.

As I noted last week, the Trump Regime actually already tried tacking on a $5/month mandatory premium for current $0-premium enrollees who auto-renew their policies for this reason. Fortunately, this was shot down by a federal judge for being done in an unconstitutional manner.

This is just as well since making it $5/mo would be excessive--remember, most current $0-premium enrollees earn so little that even $5/mo could mean having their electricity or water utilities turned off. Again, the point isn't the dollar amount, it's simply to ensure that enrollees know they're enrolled to prevent fraud.

Still, if this was the only dealbreaker issue, I could see Democrats agreeing to a $1/mo minimum.

The second potential negotiation point I described would be...

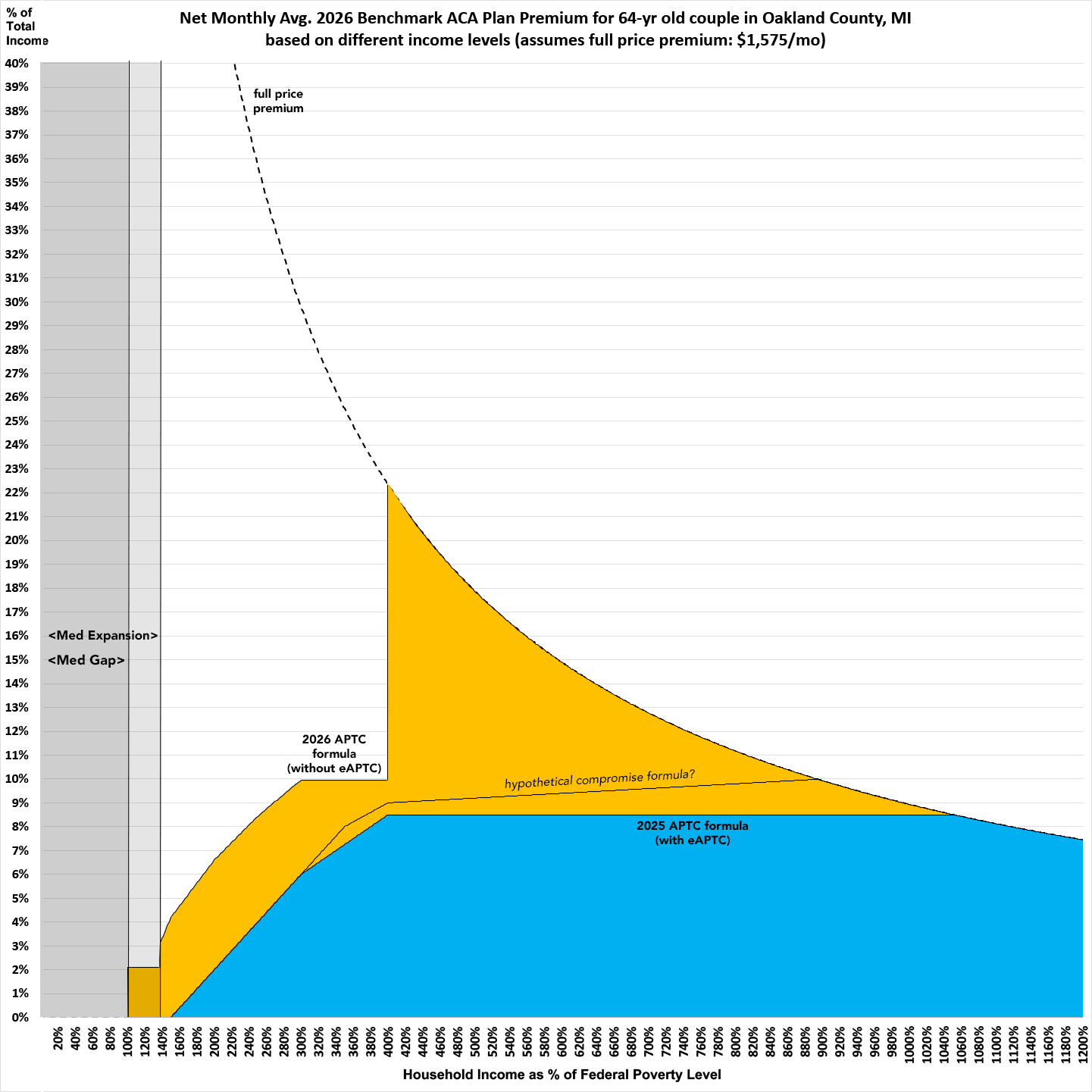

...at the upper end of the spectrum. The pre-2021 Subsidy Cliff kicked in at 400% of the Federal Poverty Level (FPL), which is $62,600/year for a single adult or $128,600 for a family of four. As I make crystal clear in my "Subsidy Expiration by State" project, this will go back to being absolutely devastating for families earning more than that.

...One criticism of the elimination of the "Subsidy Cliff" is that it's theoretically possible that a family earning up to, say, $500,000 or more could still qualify for tax credits. This is true (especially in states with insanely high gross premiums like Alaska, West Virginia and Wyoming), but it's also disingenuous since:

- a) the amount of eAPTC those households qualify for is usually pretty nominal (literally $5/month or less in some cases);

- b) those instances are extremely rare since you'd almost certainly have to be older than 55 or so for the benchmark plan to cost that much of your income, and almost everyone 55+ with that high of an income likely has employer benefits anyway; and

- c) people who have a corporate job which pays half a million dollars or more are likely receiving far more in tax credits via the Employer Sponsored Insurance Tax Exclusion anyway.

HOWEVER, if Republicans really want to be absolutely certain that there's no possibility whatsoever of Bill Gates or Elon Musk sponging $5/month in ACA tax credits, fine: Bring back the "Subsidy Cliff" at a much higher income threshold.

I suggested (purely as an example) moving the Cliff up the scale from the current 400% FPL to, say, 1200% FPL, which will be ~$188K/yr for a single adult, ~$254K for a couple, or ~$386K for a family of four in 2026.

This would make certain that anyone below those levels is protected from absurd premiums while also guaranteeing that no one earning in the high six figures receives assistance (alternately, you could raise the percent-of-income threshold from 8.5% to, say, 10% of income at 1000% FPL or whatever).

Well, sure enough, according to Axios today...

Another potential change is limiting the tax credits so that enrollees who earn above a certain income level are not eligible.

It doesn't go into any more detail about this prospect. If it's 1200% FPL, that might be feasible, but if they're talking about anything below that (likely 600% or 800%) that should be a non-starter, as that would still be devastating to older enrollees around the country.

Unfortunately, the Axios piece then throws cold water on both of these points anyway:

Any extension is also likely to be only for a couple of years, not permanent like Democrats would prefer.

...Senate Majority Leader John Thune (R-S.D.) left the door open to a subsidy extension on Friday, but said stopgap "continuing resolutions aren't places to load big health policy changes in."

...Sen. Lisa Murkowski (R-Alaska) introduced a bill last week to provide for a clean two-year extension of the credits.

Asked why Democrats are pushing for action on the Sept. 30 bill and not accepting talks later this year, Senate Minority Leader Chuck Schumer (N.Y.) told reporters Friday, "Why not do it now? People are hurting."

Again: IF they were a) made permanent and b) were locked in now (as part of a deal which also includes reining in the Trump Regime), I could see being willing to concede to a $1/mo minimum and a 1200% FPL Cliff, for example...but not for just 2 years, and certainly not after the CR is already agreed to otherwise.

I still say NO DEAL.

-----

As an aside, as a reminder, the graph below is a visual representation of what we're talking about here: It's based on a 64-yr old couple in Oakland County, Michigan enrolled in the 2025 benchmark Silver plan; the actual 2026 plan will likely cost around 17% more at full price.

The orange area is where legitimate negotiations could take place.

Advertisement