Back in July, I warned that my original projections from earlier in the year of how much net ACA enrollee premiums will increase starting in January 2026 in all 50 states +DC if the enhanced premium tax credits are allowed to expire would have to be revised & updated due to two major changes which had taken place since then:

OK, this is a bit embarrassing, but I just realized that the last time I wrote anything significant about about Illinois joining 20 other states in moving off of the federally-facilitated ACA marketplace (HealthCare.Gov) onto their own fully state-based platform (Get Covered Illinois) was nearly 2 1/2 years ago, when the state legislature passed the bill and Gov. Pritzker signed it into law!

For obvious reasons it feels a little weird to be writing about it at this particular moment in time, but the fact remains that yes, Illinois will be making the move starting November 1st, 2025. Here's a formal press release from August:

Get Covered Illinois Transitions to a State-Based Marketplace this November

Company’s HR Manager Really Pushing Infinite-Deductible Health Care Plan

During a meeting with new hires Wednesday to discuss employee benefits, Radian Analytics human resources manager Ellen Schultz is said to have strongly pushed the company’s infinite-deductible health care option.

According to sources in attendance, Schultz described the low-premium, infinite-deductible plan as the simplest and most convenient choice available to employees, and said it works the same whether plan members need to visit their primary care physician, fill a prescription, or be admitted to a hospital, allowing them in each case to pay 100 percent of the incurred medical expenses.

It's been awhile since I've done one of these, but let's go through his entire post point by point, shall we?

Ronald Reagan once quipped that “nothing lasts longer than a temporary government program.”

He could have been talking about the effort to extend — for a second time — former President Joe Biden’s Affordable Care Act-enhanced tax credits, a set of extremely generous federal health insurance subsidies intended to help Americans get through the COVID-19 crisis.

Stop right there: The "extremely generous" subsidies which he refers to are actually far less generous for higher-income enrollees than employer-sponsored insurance tax exclusions.

The District of Columbia has around ~15,000 residents enrolled in ACA exchange plans. Unlike most states where nearly all ACA exchange enrollees are subsidized, in DC only around 28% are due to the District having an unusually high income eligibility threshold for Medicaid (210%).

DC also has a unique requirement that ACA individual market plans can only be sold on their ACA exchange; I'm assuming perhaps 1,000 off-exchange enrollees regardless but officially I believe this should be pretty much zilch. With net attrition since January, however, it looks like the grand total is actually a bit below 14,000 District-wide.

This page contains proposed health plan rate information for the District of Columbia’s health insurance marketplace, DC Health Link, for plan year 2026.

The District of Columbia Department of Insurance, Securities and Banking (DISB) received 188 proposed health insurance plan rates for review from CareFirst BlueCross BlueShield, Kaiser Permanente and United Healthcare in advance of open enrollment for plan year 2026 on DC Health Link, the District of Columbia’s health insurance marketplace.

The three insurance companies filed proposed rates for individuals, families and small businesses for the 2026 plan year. Overall, 188 plans were filed, compared to 198 last year. The number of small group plans decreased from 171 to 161, and the number of individual plans remained at 27.

I joined Brad Friedman of The Brad Blog yesterday to discuss the ongoing battle over saving democracy & the impending expiration of the enhanced ACA premium tax credits (I show up starting about halfway into the hour-long episode).

You can listen to our discussion via various outlets:

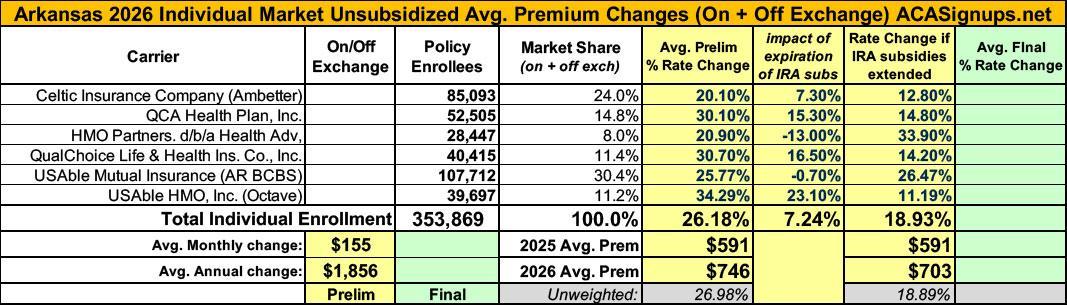

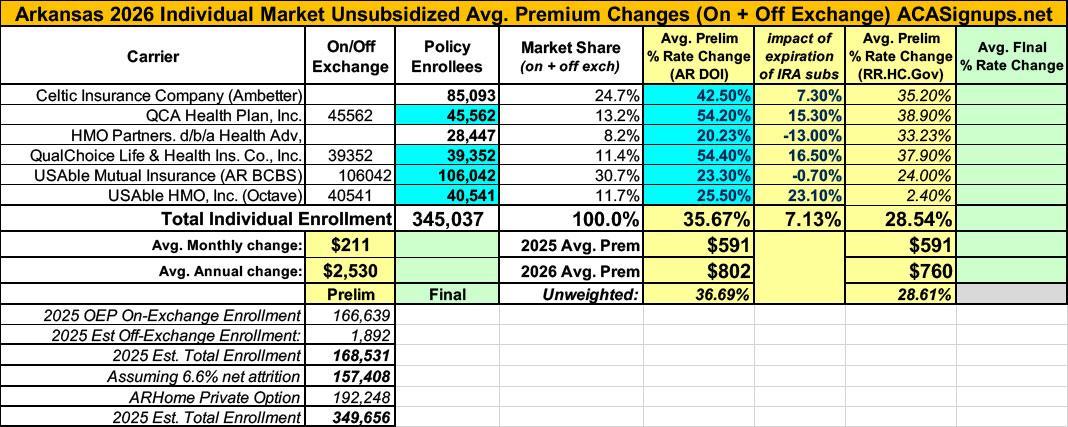

Back in July I posted my analysis of the preliminary 2026 rate filings by the 6 Arkansas insurance carriers participating in the individual market. At the time, they looked like this:

...This letter is formal notice that Aetna Health Inc. (“AHI”) intends to exit from the Individual health insurance market in Virginia effective January 1, 2026. Subject to the Department’s review, we will mail the 180-day notices of discontinuance to covered individuals.

As of May 2025, our records show that AHI has 9,810 subscribers and 13,721 total members in Virginia.

Last week I urged Democrats to demand Congressional Republicans rein in the Trump Regime's out-of-control dictatorial rampage as well as going big on healthcare policy as part of the "government shutdown" battle...but that to the extent that they do make the main focus healthcare policy, at the very least to not settle for simply bumping out the enhanced ACA tax credits by a year or two:

You know I'm a pretty mainstream Democrat. I'm not demanding Medicare for All here. What I am urging on the healthcare front is for three clear demands:

Health Carriers Propose Affordable Care Act Premium Rates for 2026

Anticipated loss of federal enhanced premium tax credits leads to highest individual market rate increases proposed since the start of Maryland’s reinsurance program

BALTIMORE – The Maryland Insurance Administration has received the 2026 proposed premium rates for Affordable Care Act products offered by health and dental carriers in the individual, non-Medigap and small group markets, which impact approximately 502,000 Marylanders.

Neighborhood Health Plan of Rhode Island (if IRA subsidies are extended):

Weighted Average Rate Increase: This represents the average rate increase, including modifications to prior year benefits and other pricing adjustments. The average premium increase to consumers, before reflecting changes in age is expected to be 16.3%.

The range of rate changes, before reflecting changes in age, which consumers will experience, is approximately 15.0% to 17.5%.

Neighborhood Health Plan of Rhode Island (if IRA subsidies AREN'T extended):

Weighted Average Rate Increase: This represents the average rate increase, including modifications to prior year benefits and other pricing adjustments. The average premium increase to consumers, before reflecting changes in age is expected to be 21.2%.

The range of rate changes, before reflecting changes in age, which consumers will experience, is approximately 20.1% to 22.2%.

Blue Cross Blue Shield of RI (if IRA subsidies are extended):

Maryland Insurance Administration Approves 2026 Affordable Care Act Premium Rates

Despite increases, Maryland remains a national leader in affordable rates; new state subsidy to offset loss of enhanced federal tax credits

BALTIMORE – Maryland Insurance Commissioner Marie Grant today announced the premium rates approved by the Maryland Insurance Administration for individual and small group health insurance plans offered in the state for coverage beginning January 1, 2026.

Rhode Island has around ~42,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~3,000 unsubsidized off-exchange enrollees.

(Aetna/CVS is pulling out of the ACA individual market in every state; I've made an educated guess as to their current enrollees, who aren't counted as part of the weighted average as they'll have to shop around for a new carrier this fall. See below.)

Antidote Health Plan:

(Antidote's actuarial memo is heavily redacted so I don't know their current enrollment; I've had to make an educated guess. See below.)

With the ongoing budget battle approaching the Sept. 30th federal government shut down deadline, U.S. Senator Patty Murray (D-WA) and U.S. Representative Rosa DeLauro (D-CT-03) have formally introduced a bicameral Continuing Resolution bill to fund the government for an extra month to buy more time to negotiate and avoid a shutdown by the Republican-controlled federal government:

Today, Senator Patty Murray (D-WA), Senate Appropriations Committee Vice Chair, and Congresswoman Rosa DeLauro (D-CT-03), House Appropriations Committee Ranking Member, introduced a continuing resolution (CR) to keep the government funded and allow negotiations to continue over full-year bills that ensure Congress, not President Trump or Russ Vought, decide how taxpayer dollars are spent. The CR also addresses the health care crisis Republicans have single-handedly created and protects Congress’ power of the purse, rejecting President Trump’s illegal “pocket rescission.”

Speaker Johnson, Leader Jeffries, Leader Thune, and Leader Schumer,

We urge you to extend the Affordable Care Act’s enhanced premium tax credits. For millions of hard-working Americans, these subsidies are the only reason health insurance is still within reach in a country where the cost of living keeps going up.

If they expire, premiums will rise by thousands of dollars for many families, millions will lose coverage, and people will be forced to make impossible choices between paying for healthcare, rent, or groceries. Hard-working American families, older Americans not yet on Medicare, small business owners, and rural communities—where marketplace coverage is often the only option—will be hit the hardest.

SACRAMENTO, Calif. — Covered California issued the following statement concerning the California Department of Public Health (CDPH) announcement of official immunization recommendations, following the passage of Assembly Bill 144:

“We applaud Gov. Newsom, the California Legislature and the Department of Public Health for recommending immunizations that are backed by scientific research and supported by trusted medical organizations,” said Covered California Executive Director Jessica Altman. “The evidence overwhelmingly shows that vaccines work, and with these steps Californians – and all Covered California enrollees – will continue to have access to these critical health tools.”

...the good news is that the [U.S. Preventative Services Task Force] can continue to do its job. The bad news is that anti-vaxxer & complete nutjob Robert F. Kennedy Jr. is now the one who gets to decide who serves on the PSTF.

The Task Force is made up of 16 volunteer experts in the fields of preventive medicine and primary care, including internal medicine, family medicine, pediatrics, behavioral health, obstetrics/gynecology, and nursing. Most of our members are practicing clinicians. To develop recommendations, we use our own expertise and routinely invite the input of disease experts and specialists. We also invite input from stakeholders and the public.

(I know numerous other states with Democratic governors have issued similar executive orders already, but I'm a lifelong Michigander as are most of my family so this one comes as particular relief to me)...

via email (no link yet):

Governor Whitmer Signs Executive Directive, Ensuring Michiganders Can Access Vaccines to Stay Healthy Ahead of Cold, COVID-19, and Flu Season

LANSING, Mich.—Today, Governor Gretchen Whitmer signed an executive directive, ensuring vaccines remain available to Michiganders as we approach the fall. Specifically, she has instructed state agencies to identify and remove any barriers to accessing COVID-19 vaccines, so Michiganders can stay healthy ahead of cold and flu season. Governor Whitmer remains committed to supporting the health and wellbeing of every Michigander and their families.

I just finished writing up a deep dive into the Arkansas Insurance Dept's move from laissez faire-style Silver Loading to fully-regulated & maximized Premium Alignment in an attempt to mitigate the massive net premium damage about to be caused if the enhanced ACA premium tax credits expire at the end of 2025.

However, it's not just Arkansas which has finally seen the light and joined about a dozen other states in putting full-bore Premium Alignment (PA) pricing into place to help reduce the financial burden on ACA individual market enrollees in 2026.

Other states which have already done so in the past include Colorado (sort of), Texas, New Mexico, Maryland, Pennsylvania (somewhat), Illinois, Vermont and Wyoming.

Warning: This isn't just gonna get deeply wonky, it also requires digging deep into hisory. You've been warned.

Chapter 1: The (simplified) Backstory:

The ACA includes two types of financial subsidies: Advance Premium Tax Credits (APTC), which reduce monthly premiums; and Cost Sharing Reductions (CSR), which cut down on deductibles, co-pays & other out-of-pocket (OOP) expenses for low-income enrollees.

In 2014, then-Speaker of the House John Boehner filed a lawsuit on behalf of Congressional Republicans against the Obama Administration, in part because they claimed that CSR payments were unconstitutional because they weren't explicitly appropriated by Congress in the text of the Affordable Care Act.

A long legal process ensued, the end of which resulted in a federal judge ruling in the GOP's favor and ordering that CSR payments stop being made...but also staying that same order pending appeal of her decision by the Justice Department (then still run by the Obama Administration).

(sigh) So, moments ago I received the following press release from the Centers for Medicare & Medicaid Services (CMS):

Today, the Centers for Medicare & Medicaid Services (CMS) unveiled details on how states can apply to receive funding from the $50 billion Rural Health Transformation Program created under the Working Families Tax Cuts Act to strengthen health care across rural America. This unprecedented investment is designed to empower states to transform the existing rural health care infrastructure and build sustainable health care systems that expand access, enhance quality of care, and improve outcomes for patients.

Amusingly (and sadly), the link itself goes to the WhiteHouse.Gov page describing not the "Working Families Tax Cuts Act" (which doesn't exist) but rather the so-called "One Big Beautiful Bill Act" which is what Trump and Republicans insisted on calling it for months, right up until they realized that it's about as popular as a turd in a punchbowl, at which point they decided that simply rebranding it as a "tax cut" for "working families" will solve all their problems at the midterms next year.

If you've been following my state-by-state 2026 avg. rate change project, you may have noticed that after filling in the final, approved rate filings for a bunch of states over the past month or so, these tapered off to just three more last week (Illinois, Washington and Connecticut).

State Highlights Rising 2026 Health Insurance Rate Proposals

SAINT PAUL, MN: Minnesotans are facing unnecessarily higher health insurance rate hikes, and the blame lies with new Republican-led federal policy changes passed in Washington, says Minnesota Commerce Commissioner Grace Arnold.

“While HR1 has been dubbed the “One Big Beautiful Bill” by Republicans, many in our state will find nothing beautiful in health insurance premium increases they’ll experience for 2026,” Arnold said. “These will be the highest rate hikes since 2017 for individual and group markets.”

The Connecticut Insurance Department has posted the initial proposed health insurance rate filings for the 2026 individual and small group markets. There are 8 filings made by 7 health insurers for plans that currently cover approximately 224,000 people (158,000 individual and 66,000 small group).

Anthem has filed rates for both individual and small group plans that will be marketed through Access Health CT, the state-sponsored health insurance exchange. ConnectiCare Benefits Inc. (CBI) and ConnectiCare Insurance Company, Inc. have filed rates for the individual market on the exchange.

Before I continue, note that yes, I'm aware the 17.8% average shown below doesn't match the 22.9% average in the headline above. There's a reason for this which should be obvious if you read on:

The 2026 rate proposals for the individual and small group market are on average higher than last year:

Last week I noted that Colorado legislators passed (and Gov. Polis signed) legislation to scrape together up to $100 million in emergency funding to backfill perhaps 40% or so of the federal tax credits the state expects their ~225,000 subsidized enrollees to lose in 2026 when the enhanced IRA credits expire this December:

...The Senate then approved House Bill 25B-1006, which would sell tax credits to bring in money for the Health Insurance Affordability Enterprise fund. That pays for programs to reduce individual insurance market premiums.

The bill aims to raise $100 million for that enterprise to soften the impact of the expiration of federal enhanced premium tax credits. Health insurance premiums for people who buy insurance on the individual market are expected to face an average of a 28% increase next year, with higher increases along the Western Slope.

This is gonna be one of the stranger references I've made on this site, but bear with me.

Back in 1996 there was an HBO movie called "The Late Shift" which told the story of the Late Night TV show battle between David Letterman and Jay Leno over who would succeed Johnny Carson as host of The Tonight Show. As stupid as this may sound today, this was actually a Really Big Deal in the '90's...one of those absurd pop culture stories which dominated the headlines and the tabloids for several years.

The movie itself was decent, with some interesting casting including Kathy Bates and Treat Williams, but nothing special. The main problem is that the audience is expected to root and feel sympathy for a couple of dudes who were already rich & famous and who would both continue to be rich & famous no matter how the story played out. The stakes weren't exactly the fate of the world, is what I'm saying.

OLYMPIA, Wash. — Fourteen health insurers have requested an average rate change of 21.2% for Washington state's 2026 Individual Health Insurance Market. Insurers base their requested rate changes on assumptions they make about the services their policyholders will use and the cost to deliver that care. The health plans and proposed rate changes are currently under review by the Office of the Insurance Commissioner.

Wellpoint Washington, Inc. is new to the market and plans to sell in Grays Harbor, King and Spokane counties.

Back in June I ran an analysis to try and break out just how many Americans are likely to lose healthcare coverage in every Congressional District nationally under the recently-passed MAGA Murder Bill, officially known as H.R.1, the One Big Beautiful Bill.

As I showed at the time, while there's around 65% more people enrolled in Medicaid via ACA expansion in House districts held by Democrats (roughly 12.7 million in blue districts vs. 7.7 million in red districts), there's around 34% more ACA exchange enrollees in red districts (around ~13.9 million vs. ~10.4 million in blue districts).

I then went a step further and broke out the House districts into 10 tiers based on what percent of the vote Donald Trump received last year to take a more granular look and found that, shocker, there's no "winners" here; every district is a loser across the ideological spectrum.

The good news is, the Illinois Insurance Dept. now provides a handy, simple table with the actual average rate changes as well as direct links to the actuarial memos & other filing forms for every carrier, which made it easy for me to plug in the effectuated enrollment & calculate the weighted average rate hikes for every carrier in both the individual and small group markets.

The bad news is, some of the actuarial memos themselves are heavily redacted, meaning I'm unable to see how much of the rate hikes are due to the IRA subsidies expiring, CSR payments being reinstated or Trump's tariffs.

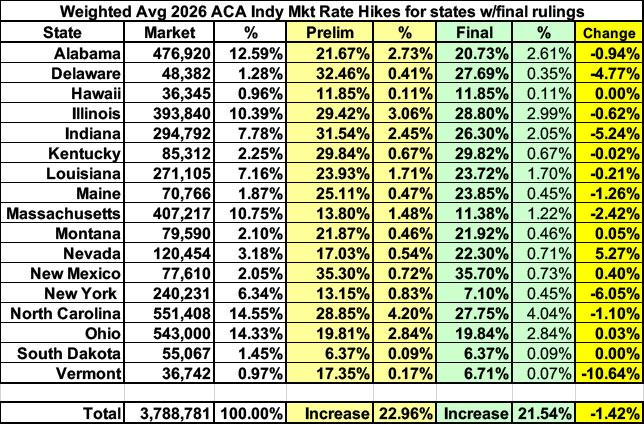

As of this morning I've confirmed final/approved filings across 17 states. Across these state the weighted average year over year increase is 21.5%, down about 1.4 points from the preliminary increase of 23.0%.

I expect final filings for at least a dozen more states to come in over the next week or so, but unless a couple of large states like Texas or Florida have dramatic reductions in their rate increases along the lines of New York or Vermont, I'd still expect the overall national average to and up over 20%.

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of May 2025:

PENNSYLVANIA – August 26, 2025 – Pennie, Pennsylvania’s official health insurance marketplace, in coordination with Health Market Connect LLC (HMC), the newly appointed contractor of Pennie’s Assister Network, is taking a major step forward in connecting the uninsured with affordable health coverage. Pennie and HMC are launching a new network of regional organizations dedicated to providing localized support throughout the Commonwealth.

This innovative and community-centered model is designed to ensure that every Pennsylvanian, regardless of where they live, has access to trusted, in-person assistance when exploring their health coverage options. The appointed regional organizations will be responsible for hiring local Pennie-Certified Assisters who will serve as trusted guides throughout the enrollment process and conducting outreach to the uninsured.

Marketplace enrollees from across the country joined State-based Health Insurance Marketplace leaders and insurance experts at a virtual press conference today to discuss the immediate, real-world impacts of potentially losing their health insurance tax credits.

More than 24 million Americans enrolled in Health Insurance Marketplaces have come to rely on increased insurance affordability, thanks to enhanced premium tax credits (EPTCs) set to expire at the end of 2025. Without Congressional action by September 30, the loss of EPTCs is estimated to cause 4.2 million Americans to lose their health insurance. Marketplace consumers are expected to see an average 75 percent cost increase across states.

From small towns to the nation’s most populous state, enhanced premium tax credits are helping millions of Americans get the financial help they need to get connected to affordable health insurance.

Each year insurers that sell Individual and Small Group plans in Maine's pooled risk market must submit their proposed forms and rates to the Bureau of Insurance, using the System for Electronic Rate and Form Filing (SERFF). Details of the filings submitted to the state since June 10, 2010 can be viewed in the system.

Anthem Health Plans of Maine:

The proposed rates have been developed from 2024 Individual and Small Group ACA combined experience, and the proposed average annual rate change at the Merged Market level is 18.0%.

The proposed annual rate changes by product for Individual range from 17.9% to 20.6%, with rate changes by plan from 10.1% to 30.0%. These ranges are based on the renewing plans, and are consistent with what is reported in the Unified Rate Review Template. Exhibit A shows the rate change for each plan.

Factors that affect the rate changes for all plans include:

Maine has around 64,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~4,500 unsubsidized off-exchange enrollees.

Combined, that's around 70,000 people, although it could be somewhat lower due to net enrollment attrition since January.

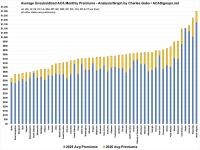

For months now I've been shouting from the rooftops about the imminent expiration of the improved federal tax credits for ACA enrollees, repeatedly pointing out that those already paying full price are gonna get hit with average premium hikes of over 23% while most of the 92% of exchange enrollees who currently receive at least some federal assistance will see their net premiums skyrocket by up to 100%, 200% or even 300% or more.

Having helped cause this crisis in the first place both by refusing to push Congressional Republicans to extend the enhanced subsidies as well as by changing the Premium Adjustment Percentage Index formula (PAPI) to make the remaining subsidies even less generous, the Trump Regime has come up with what I'm sure they think of as a brilliant "solution" to the problem.

Back in March I wrote about a proposed rule (really a set of rules) put out by the Trump Regime's Centers for Medicare & Medicaid Services (CMS) which, if implemented, would make major changes to how the Affordable Care Act is administered. This rule was finalized in June, with some provisions kicking in immediately, most starting January 1st and others over the next couple of eyars.

This set of regulatory changes is completely separate from the impending expiration of the improved premium tax credits which I've written so much about; these have to do with the specifics of how the ACA is actually implemented going forward.

A very simple example of this is the length of the annual Open Enrollment Period, which has ranged from as long as 6 months during the very first OEP in 2013-2014 to as short as just 75 days during most of the first Trump Administration.

As I noted last month, Colorado's ~321,000 individual health insurance market enrollees are currently staring down the barrel of massive premium hikes less than four months from today:

Every state government is handling this situation differently. In Arkansas and New Hampshire, the strategy seems to be to either shout at or beg carriers to re-file with lower gross premium increases for 2026. New Mexico, California and New Jersey, in contrast, are all retooling their existing state-based supplemental subsidy programs to help cushion at least some of the impact.

For the individual market, this is actually slightly lower than the national average (23.4%), and New Hampshire will still end up with the 2nd-lowest avg. premiums in the country (Idaho should be slightly lower next year), but 22.4% is still pretty steep, and the state insurance dept. isn't happy about it:

New Hampshire Insurance Department Urges Health Carriers to Submit Revised 2026 Premium Rates Reflecting Current Economic Conditions

Every year, I spend months painstakingly tracking every insurance carrier rate filing (nearly 400 for 2025!) for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

As of September 2nd, I've managed to fill in preliminary weighted average 2026 rate filings for all 50 states +DC as well as the final/approved rate filings for 15 states.

While it will move up or down slightly as more states finalize their 2026 filings, as of this writing, the weighted average rate increase for unsubsidized enrollees is 23.4% nationally.

This is the 2nd highest year-over-year gross rate hike since the ACA overhauled the individual market starting in 2014.

And yes, a significant chunk of this is due specifically to three factors:

Estimated Health Impacts of Almost $13 Billion Annually, Paralyzing Our Health Care System

1.5 Million New Yorkers Stripped of Health Care Coverage and Become Uninsured; Projected $8 Billion in Losses for New York’s Hospitals

Governor Kathy Hochul today joined U.S. Representative Ritchie Torres, local elected officials, doctors, and healthcare leaders to warn of the destructive ramifications of President Trump and Congressional Republicans’ “Big Ugly Bill” on New York State. The cuts imposed by Washington Republicans are expected to have a significant impact, with an anticipated nearly $13 billion affecting New Yorkers healthcare system. Additionally, approximately 1.5 million New Yorkers are projected to lose their health insurance coverage, while over 300,000 households are expected to lose some or all of their SNAP benefits.

Well this is a welcome bit of good news. While ACA major medical health insurance policy premiums are set to skyrocket in 2026 (largely due to Congressional Republicans allowing the improved premium subsidies to expire while the Trump Administration changes the underlying tax credit formula to make it significantly less generous), Covered California just announced that 2026 premiums for their standalone dental plans are set to cost pretty much the same next year:

Covered California Announces Premium Change for 2026 Dental Plans After Another Year of Steady Growth

SACRAMENTO, Calif. — Covered California announced that the statewide weighted average rate change for dental plans offered through the marketplace in 2026 will be 0.35 percent.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Anthem Health Plans of KY:

This filing includes an average rate change of 24.0%, excluding the impact of aging, effective January 1, 2026. At the individual plan level, rate increases range from 11.1% to 28.9% for renewing plans. A subscriber’s actual rate could be higher or lower depending on the geographic location, age characteristics, dependent coverage, and other factors.

Unfortunately, Anthem doesn't provide their actual 2025 individual market enrollment; I've had to estimate this based on marketwide estimated enrollment; see below.

Nevada has around ~110,000 residents enrolled in ACA exchange plans, 87% of whom are currently subsidized. I estimate they also have another ~23,000 unsubsidized off-exchange enrollees.

Generally, once a year MVP files for a change to the current premium rates on file for their products based on a review of the adequacy of the rate level. Premiums need to be sufficient to cover all medical and pharmacy claims submitted from covered members, cover the administrative cost of operations, Federal and New York State taxes/assessments levied and New York State statutory reserve requirements.

MVP is proposing a premium rate adjustment effective January 1, 2026. Policyholders will be charged the proposed premium rates upon renewal in 2026 pending New York State’s Department of Financial Services review. There are 13,062 policyholders and 19,125 members currently enrolled in Individual MVP Health Plan, Inc. plans. The proposed premium rate adjustment represents an average increase of 8.00%. Premium changes will vary by plan design.

Premium rates are changing due to the following reasons:

JULY 31st, 2025 - Nevadans Get a Preview of 2026 Proposed Health Insurance Rate Changes for Upcoming Open Enrollment

[CARSON CITY, NV] - Starting August 1st, Nevada consumers who shop for their health insurance on the individual health insurance market can view and provide comments on proposed rate changes for Plan Year 2026.

The Nevada Division of Insurance (Division) has received and made public on its website the 2026 proposed rate changes from health insurers intending to sell plans on and off the Silver State Health Insurance Exchange (the "Exchange"). The Exchange is the state agency that assists eligible Nevada residents to purchase affordable health and dental plans.

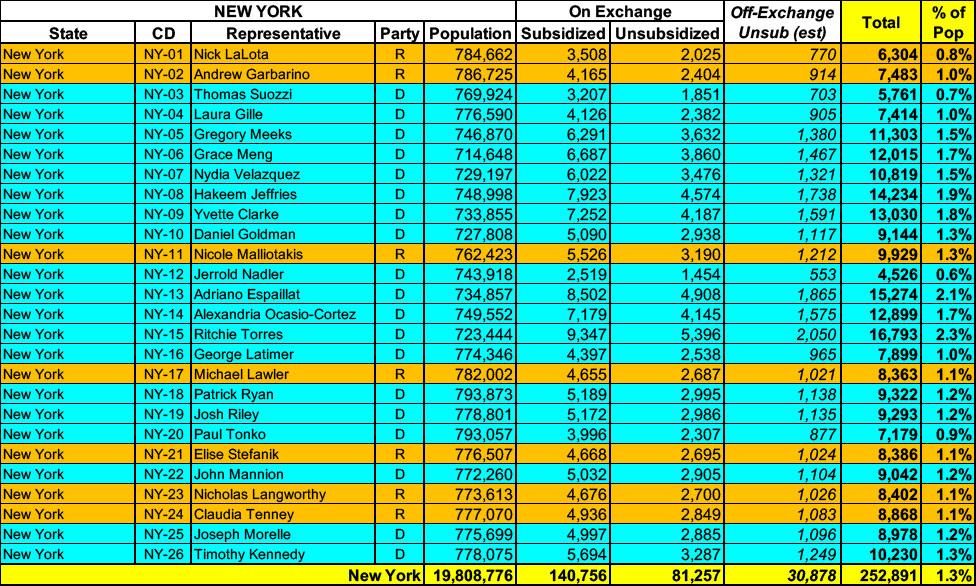

New York has around ~222,000 residents enrolled in ACA exchange plans, 63% of whom are currently subsidized. I estimate they also have another ~31,000 unsubsidized off-exchange enrollees.

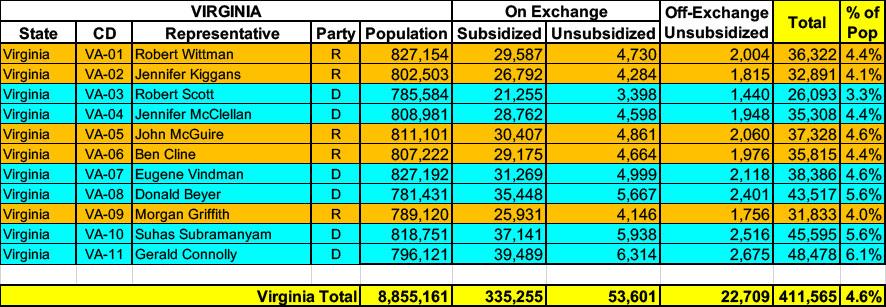

Virginia has ~388,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. They also have over 22,000 off-exchange enrollees. Combined, that's 411,000 people with ACA market coverage, or 4.6% of the total population.