(Sigh) OK, here goes: How about my own family?

Mon, 11/03/2025 - 11:08am

For nearly a year now, I've been writing about the upcoming expiration of the enhanced ACA premium tax credits (eAPTC) which have been in place for the past five years. They're currently scheduled to expire at the end of December, less than 2 months from today.

I spent most of the year posting projected estimates of how much more different households will have to pay.

More recently, as the actual 2026 premium rate filings have been published, I revised those estimates with more accurate data.

Over the past few weeks as the various ACA exchange websites brought their 2026 ACA window shopping live, I've started plugging in different household scenarios to see what actual, real world price hikes look like.

Throughout all of these examples, however, two things have remained consistent:

- I've used the benchmark Silver plan as the policy of choice for both years for pretty much every example, and...

- Aside from the occasional side reference here & there, I've avoided using my own family as a case study.

The reason I always use the benchmark plan is because that's the only way to run a true apples to apples comparison between this year and next. There are dozens or even hundreds of different plans available in every county nationally, ranging from Bronze HMOs to Platinum PPOs and numerous variants in between.

The full price of the benchmark Silver plan (defined as the second least-expensive Silver plan available in your area) is what the entire tax credit formula is based on, so this is the natural one to use as my baseline.

However, the benchmark Silver plan isn't always the best option. It may not have the healthcare providers you need (doctors, hospitals, clinics); the drug formulary may not include the prescriptions you need, and so on.

I've been avoiding talking too much about my own family's situation for a couple of reasons: First, to protect our privacy: I'm pretty open, but my wife is a pretty private person and I don't have the right to discuss her or my son's medical needs publicly.

Second, I don't want to make this sound like I'm putting out a plea for charity. We're gonna get hit pretty hard no matter what, but we're still gonna be a lot better off than millions of other Americans, especially the ~42 million who just lost SNAP benefits, some of whom are also about to be hit by the expiring ACA tax credits, I should note (the general cut-off for SNAP is 130% FPL).

Having said that, if you do happen to find my healthcare wonkery useful and want to support it, you can do so once or monthly here.

My wife has given me her OK to reveal that she has some chronic medical conditions, one of which requires a pretty damned expensive prescription drug...and by expensive, I mean the full list price would be thousands of dollars each month. Without it, she'd risk severe allergic reactions, potentially including severe breathing issues and possibly even death.

She's on a treatment plan which will hopefully alleviate the need for this medication in the future, but that could be a couple of years away, so for at least the next year or so, we have to operate on the assumption that this prescription alone will max out any deductible or maximum out of pocket limit that we end up with.

There's also the other "normal" medical needs that any middle-aged couple and their college-age kid may have in a typical year.

In addition, our healthcare provider requirements are such that we pretty much have to stick with either Blue Cross Blue Shield of Michigan or Blue Care Network (BCBSM = PPOs, BCN = HMOs).

So. First things first: Let's plug in our household info and see what comes up.

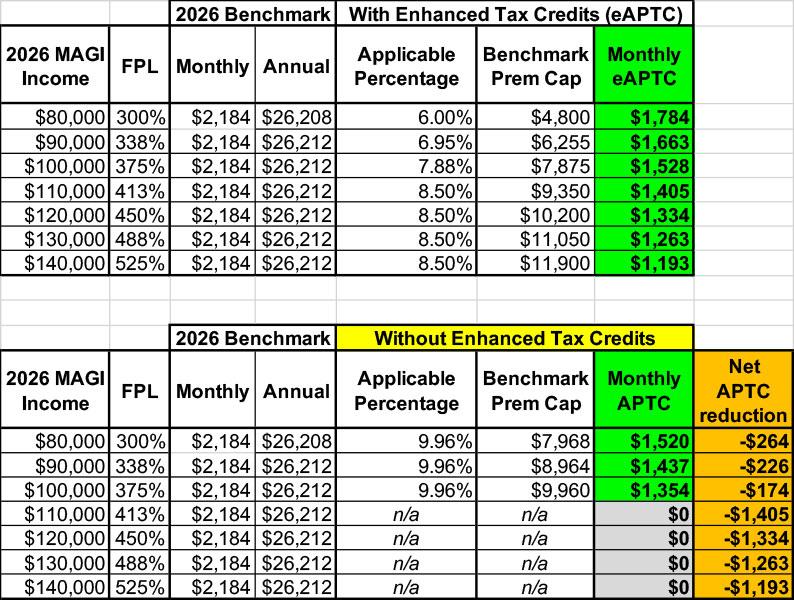

In Oakland County, Michigan, for 2026, the benchmark Silver plan is a UnitedHealthcare UHC Silver Value (No Referrals) HMO plan.

For our family, at full price this would run $2,184/month ($26,212/year), with an $8,000 family deductible and a $19,000 family MOOP (maximum out of pocket cap for in-network services). We won't be using UHC, but this is still critical to know.

Now let's look at our annual 2026 income. I'm not going to specify how much it is for two reasons:

First, to maintain some level of privacy.

Second, because we honestly have no idea. Both my wife and I are self-employed and our income can vary wildly from year to year, generally ranging between around $80,000 - $140,000/year...which translates into somewhere between 300 - 500% FPL.

For 2025, that income range would mean between $405 - $980/month in federal tax credits...but that was based on the 2025 benchmark Silver plan running just $1,385/month at full price.

However, as noted above, the 2026 benchmark plan runs $2,184/month at full price...which means that IF the enhanced tax credits were to continue next year, we'd be eligible for anywhere from $1,193 - $1,784/month in federal assistance...

...but with the enhanced tax credits expiring, our tax credit eligibility drops anywhere from substantially to entirely:

What does this mean for what we actually have to pay?

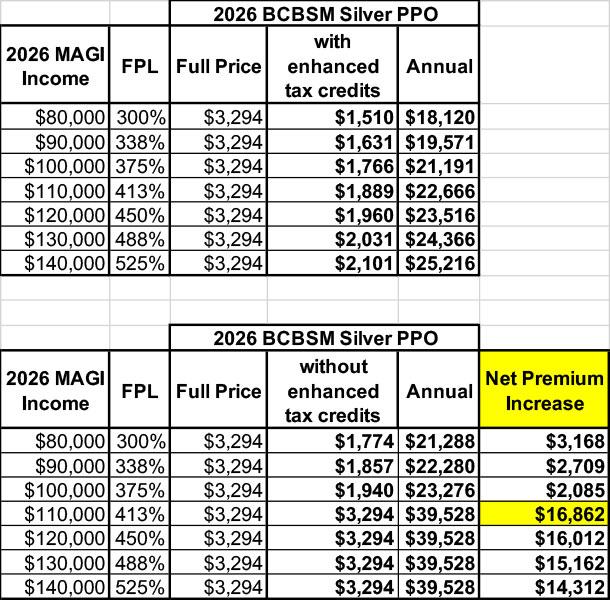

Well, as noted above, the benchmark Silver plan isn't relevant any longer since we have to stick with BCBSM or BCN.

We're currently enrolled in a Silver BCBSM PPO plan. This year it costs $2,466/month at full price...but starting in January, this is shooting up a whopping 33.5% to $3,294/month. Ouch.

Here's what that translates into for us, assuming we stay on the same plan:

- If our 2026 MAGI income turns out to be less than 400% FPL ($106,600), we'll have to pay at least $2,000 more in premiums next year.

- If our 2026 MAGI income turns out to be more than 400% FPL, however (by even $1)...we're seriously screwed: Our net premiums skyrocket by an additional $14,000 - $17,000 for the year.

It's important to keep in mind that I haven't even gotten into deductibles & other out-of-pocket expenses yet, which is vitally important given that, as I note above, my wife's prescriptions alone will likely blow both our deductible and MOOP out of the water.

The BCBSM Silver PPO we're on today has a famiily deductible of $7,800 and a family MOOP of $15,400.

So what other options do we have? Well, as I said, we're pretty much limited to BCBSM or BCN, which narrows the 64 total plans in Oakland County down to 26.

We also have a Health Savings Account (HSA), which narrows things down to 13; the following all assume full price (unsubsidized):

- 8 BCN HMOs (1 Catastrophic, 7 Bronze), ranging from $1,487 - $2,068/mo

- 5 BCBSM PPOs (1 Catastrophic, 3 Bronze, 1 Silver), ranging from $1,762 - $3,294/mo (our current plan)

HC.gov's "estimated total yearly cost" -- assuming low use for my son and I but high use for my wife -- gives the following estimated total annual costs at full price:

- HMOs: From $29,128 - $34,976/year

- PPOs: From $32,379 - $47,914/year

Put another way, our current plan appears to be the worst choice we have.

It looks like our best bet would be to go for the lowest-priced PPO or to drop back to an HMO assuming all of our providers are still in network.

If we're able to keep our 2026 MAGI income below the 400% FPL threshold, we'll be eligible for $16K - $18K in tax credits, which would cancel out between 33 - 62% of the total (combined) costs.

And obviously if we have a windfall year and hit, say, 600% FPL, the extra income would more than make up for the dramatic price spikes.

If, however, we end up anywhere between 400 - 500% FPL (which is the most likely scenario), we're in trouble...because we'd lose out on ~$17K in tax credits without earning enough to cancel it out.

The good news (such as it is) is that there are ways of reducing your MAGI income which are perfectly legal, including things like HSAs and IRAs. I'll be writing more about those soon.

Advertisement