2026 Final Gross Rate Changes - Missouri: +23.1%; ~417,000 enrollees looking at massive rate hikes in January (updated)

Fri, 10/31/2025 - 9:14pm

Originally posted 8/03/25

via the Missouri Insurance Dept:

Healthy Alliance Life Insurance Co:

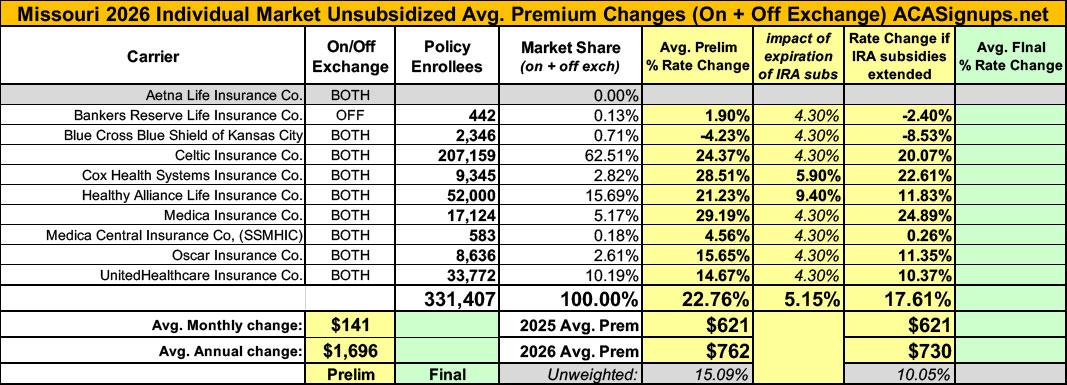

Healthy Alliance Life Insurance Company (HALIC) has filed for premium rate changes for its Affordable Care Act (ACA) compliant Individual health insurance plans. This filing includes an average rate change of 21.23%, effective January 1, 2026, with plan prices changing between 18.75% and 24.73%. The price changes will impact about 52,000 people that have HALIC plans now and will keep HALIC plans next year. An insured person’s actual rate increase could be higher or lower depending on their benefit, where they live, how old they are, number of children, and if they use tobacco.

Data from HALIC’s 2024 ACA-compliant plans has been used to develop the proposed rates. HALIC has made assumptions around how that data will change between 2024 and 2026. Assumptions include how much the health of people will change between 2024 and 2026 (morbidity), who will purchase what kind of plans in 2026 (demographics and benefits), how much medical and pharmacy costs will change between 2024 and 2026 (trend), and how much HALIC’s costs will be to run its business operations in 2026 (non-benefit expenses). In addition to these assumptions, some of the most significant factors underlying the rate change are changes in the purchasing population.

...Morbidity Adjustment

Adjustments are made to account for the differences between the average morbidity of the experience period population and that of the anticipated population in the projection period. The projected population consists of expected retention of existing policies and new sales. The sources of new entrants include the previously uninsured population, grandfathered and transitional policies voluntarily migrating to ACA-compliant plans, and previously insured populations from other carriers or markets. The morbidity adjustment reflects projected Anthem and market changes in morbidity, including changes from the expiration of the enhanced ACA premium tax credits on December 31, 2025. Selective lapsation is expected to increase morbidity of the risk pool as a disproportionate number of healthy enrollees is expected to leave the market due to increases in their net premiums after subsidies and economic considerations. The cumulative morbidity factor can be found in Exhibit E, which is a factor of 1.0940 applied to claims.

Blue Cross Blue Shield of Kansas City:

Blue Cross and Blue Shield of Kansas City (BCBSKC) is filing rates for individual plans in Missouri. The overall average premium increase for individual plans in 2026 is -4.2% compared to the 2025 individual rates. The changes for plans range from -9.1% to 1.5%. This does not include and additional small increase for attaning a new age. That is, an individual’s premium rates will increase each year as they get older, even if the rates for their plan do not change. This small increase is not factored in to the average increases stated above.

In developing assumptions and setting rates for 2026, BCBSKC used data from its own claim experience, as well as information received from Wakely, a company which provides free services to aid insurance companies which provide coverage to individuals and small groups. In 2024, the “experience period” used as a starting point for developing rates for 2026, BCBSKC experienced a medical loss ratio (MLR) of 91.0%. This means that 91.0% of premium and risk transfer received was spent on medical and drug claims. Our projected loss ratio for Affordable Care Act (ACA) individual plans in 2026 is 84.0%.

Celtic Insurance Company:

Celtic Insurance Company’s proposed rate change is 24.4% and it applies to 207,159 members. The most significant driver of the rate increase is an increase in statewide morbidity.

Celtic Insurance Company began business in Missouri in 2018, with plans offered in 40 counties; Celtic Insurance Company’s will be offering plans in 109 counties for 2026. Premium rates were reduced in 2025 and will be increased in 2026. We expect this, in addition to rising claim costs, to increase the estimated 2024 Medical Loss Ratio (MLR) of 69.3% to 84.5% for 2026. The MLR describes the percentage of premium payments used to pay medical claims and to improve the quality of care. Our estimate for 2026 is that 84.5% of premiums paid to Celtic Insurance Company’s will be used to pay member claims and support activities that improve the quality of the care we offer.

Bankers Reserve Life Insurance Co.

Bankers Reserve Life Insurance Co.’s proposed rate change is 1.9% and it applies to 442 members. The most significant driver of the rate increase is an increase in statewide morbidity.

This is a sophomore filing with no credible experience. Our estimate for 2026 is that 89.0% of premiums paid to Bankers Reserve Life Insurance Co. will be used to pay member claims and support activities that improve quality of the care we offer.

Cox Health Systems Insurance Company

Purpose and Scope of Rate Justification:

This letter explains the rate change for Cox Health Systems Insurance Company’s (CHSIC) calendar year 2026 rates. This letter is for health plans offered to individuals. These plans are offered through the website Healthcare.gov. CHSIC will offer plans in these Missouri counties: Barry, Christian, Lawrence, Stone and Taney.

Plans sold to Missouri individuals are:

- Plan Name Metal Tier

- Gold Preferred $1000 Deductible Gold

- Gold Standard $2000 Deductible Gold

- Silver Connect 9 $6500 Deductible Silver

- Silver Preferred $5500 Deductible Silver

- Silver Standard $6000 Deductible Silver

- Bronze Expanded Standard $7500 Deductible Bronze

- Bronze Preferred $10,600 Deductible Bronze

The average rate change is a 28.5% increase. This rate change applies to 9,345 members. The actual rate change will vary by plan. The smallest change is a 18.5% increase. The largest change is an 33.1% increase.

Data, Information and Assumptions Used to Develop the Rates:

To set rates for 2026, CHSIC used their costs for their business in Missouri. CHSIC believes members will use services like prior years. The non-claim expenses are based on actual expenses from the prior year.

Main Factors Causing the Rate Change:

- We assume claim costs for medical and pharmacy services will go up. Today, health care costs are rising 9.9% per year. This means the premium rates were increased to cover the higher claim costs.

- We are assuming the members who enroll with CHSIC will have more claims than the previous members. This caused the premium to go up.

- Hospital costs are expected to go up for visits at Cox Medical Centers. This caused the premium to go

- up.

- We are assuming CHSIC will have to make Risk Adjustment payment. This caused the premium to go up.

Medica Central Insurance Company

Medica Central Insurance Company (MCTIC) is requesting a rate change for its Affordable Care Act (ACA) individual market business in Missouri. The rate change will take effect on January 1, 2026 and will impact an estimated 583 members. The average rate change will be 4.6% and will result in rate changes that vary across plan designs. This includes changes to the costs of care.

MCTIC uses 2024 data from Missouri to develop premium rates. This data includes estimates of changes to the below through 2026:

- Population Medica expects to insure

- Cost of medical services

- Cost of pharmacy services

- Taxes and fees

The significant factors that impact the rate change include those listed above. Claim costs per member per month are expected to change from $537.72 in 2024 to $658.25 in 2026.

Medica Insurance Company

Medica Insurance Company (Medica) is requesting a rate change for its individual market business in Missouri. The rate change will take effect on January 1, 2026 and will impact an estimated 17,124 members. The average rate change will be 29.2% and will result in rate changes that vary across plan designs. This includes changes to the costs of care.

Medica uses 2024 data from Missouri, which includes estimates of changes to the below through 2026:

- Population Medica expects to insure

- Cost of medical services

- Cost of pharmacy services

- Taxes and fees

The significant factors that impact the rate change include those listed above. Claim costs per member per month are expected to change from $399.48 in 2024 to $494.20 in 2026.

Oscar Insurance:

The purpose of this document is to present rate change justification for Oscar Insurance Company’s (Oscar’s) Missouri individual Affordable Care Act (ACA) products, with an effective date of January 1, 2026, and to comply with the requirements of the Missouri Department of Insurance.

The average rate increase for renewing plans is 15.7%. Rate increases vary by plan due to a combination of factors including plan design and geographic rating factors. This rate increase is absent of rate changes due to members aging.

The rate increase impacts an estimated 8,636 members.

2. Reason for Rate Increase(s)

The significant factors driving the proposed rate change include the following:

- Medical and Prescription Drug Trends

The projected premium rates reflect trends for anticipated changes in cost and usage of medical and prescription drug services.

- Administrative Expenses, Taxes & Fees, and Risk Margin

Changes to the overall premium level are needed because of required changes in federal and state taxes and fees. In addition, there are anticipated changes in both administrative expenses and profit.

- Prospective Benefit Changes

Plan benefits have been revised as a result of changes in the Center for Medicare and Medicaid Services (CMS) Actuarial Value Calculator and state requirements, as well as new and updated offerings which are more consumer friendly and easier to understand. The AV calculator is used to determine whether health insurance plans offer enough coverage to meet ACA requirements and to set metal levels.

Anticipated Changes in the Average Health of the Covered Population

Changes to the overall premium level are needed because of anticipated changes in the underlying health of the marketplace.

UnitedHealthcare Insurance Company

Qualified Health Plan Issuers are required to provide a justification for the requested rate increase in Missouri. Below is justification for the rate increase effective January 1, 2026, for UnitedHealthcare Insurance Company (UHIC) individual medical plans offered in Missouri that are fully compliant with the Patient Protection and Affordable Care Act (ACA).

Scope and Range for the Rate Increase:

The overall average rate change is +14.7%, and the rate change by plan varies from +9.6% to +19.3%.

The most significant factors underlying the average rate change are described below:

- Medical and pharmacy costs are increasing and we are changing our premium rates to reflect this increase.

- Expected changes in market morbidity in addition to the estimated impact as healthier members leave the market if the enhanced premium tax credits expire.

- Changes in non-claims expenses.

The actual rate change for an individual depends on plan selection, location, age, family size, and tobacco usage

Only one of the carriers (Cox Health Systems) publicly states the impact of the IRA subsidies expiring specifically (the rest of the carriers have this figure redacted), so I've plugged in the Congressional Budget Office's national average projection of 4.3% for the rest of them.

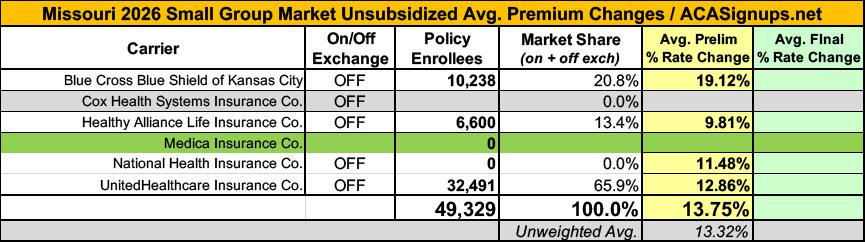

This gives a weighted statewide average of 22.8% on the individual market and 13.8% for the small group market.

It's worth noting that Aetna is dropping out of the indy market while Cox Systems is pulling out of the MO small group market. On the other hand, Medica is newly entering the latter.

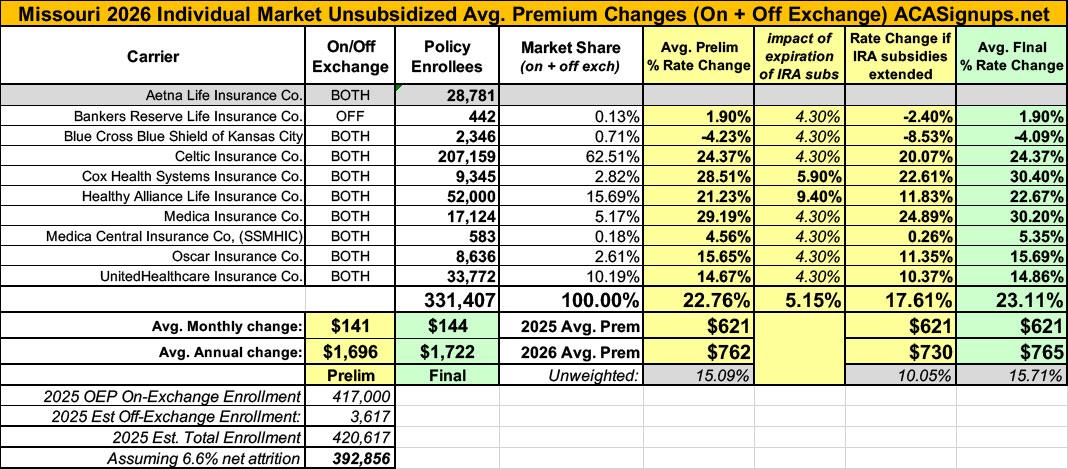

Also note that while the individual market total for Missouri is only 331,407, MO's on-exchange enrollment during the 2025 Open Enrollment Period was actually 417,000 even. I'm assuming that the missing ~85,000 or so enrollees currently have Aetna plans and will have to shop around for a different carrier plan this fall.

It's important to remember that these are just for unsubsidized, full price premiums. The impact on net rate hikes for the vast majority of ACA exchange enrollees will be much higher than 22.8%.

UPDATE 10/31/25: With one day to go before Open Enrollment begins, the Missouri Insurance Dept. has published their final, approved 2026 rate filings.

Not much to report, really...a couple of carriers had their average rate hikes nudged up a hair, so the final weighted average is 23.1% (up 0.4 pts from the preliminary filings).

| Attachment | Size |

|---|---|

| 68.34 KB | |

| 112.08 KB | |

| 145.33 KB | |

| 574.56 KB | |

| 54.55 KB | |

| 36.99 KB | |

| 121.45 KB | |

| 127.75 KB | |

| 82.16 KB | |

| 143.69 KB | |

| 107.96 KB |

Advertisement