2026 Final Gross Rate Changes - Nebraska: +29.1% (updated)

Sat, 11/01/2025 - 9:56am

Originally posted 8/8/25

Overall preliminary rate changes via the SERFF database, Nebraska Insurance Dept. website and/or the federal Rate Review database.

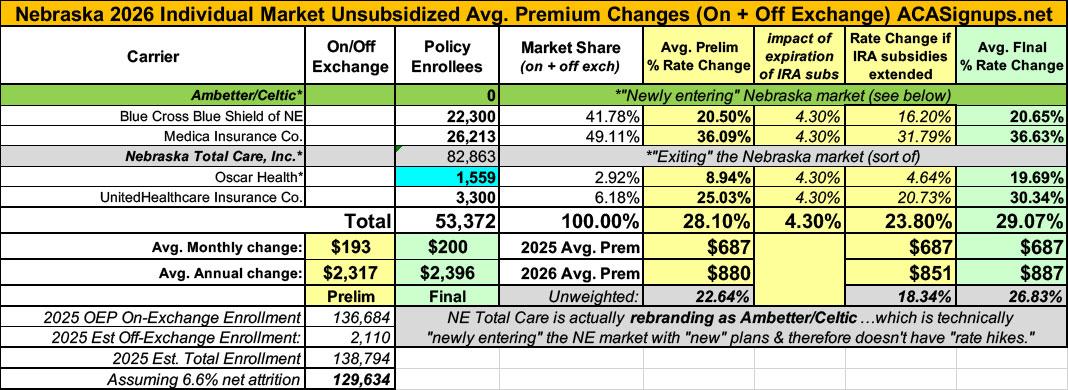

Blue Cross Blue Shield of NE:

Blue Cross and Blue Shield of Nebraska (BCBSNE) is setting new rates for its Individual ACA market business in Nebraska. The rate change will take effect January 1, 2026, and will impact an estimated 22,300 members. On average, rates will go up by 20.5% compared to 2025 individual rates. Depending on the network and plan, rate changes will range from a decrease of 1.1% to an increase of 33.3%. Additionally, premiums will go up a bit each year as people get older, even if their plan rates stay the same.

BCBSNE used its own claims and enrollment data, and other publicly available information to set these rates.

BCBSNE expects the new rates to cover medical costs and result in a medical loss ratio (MLR) of 86.3%. This means 86.3 cents of every premium dollar will go towards members' medical expenses and improving health care quality. This MLR is higher than the ACA's minimum requirement of 80%. If the three-year average MLR falls below 80%, BCBSNE will refund the difference to policyholders as required by federal law.

Key Drivers Behind the Rate Increase

The proposed rate changes for 2026 are due to several important factors, including:

- A correction to rates for unexpected changes to the market’s overall health.

- Estimated changes in the market's health because the extra premium subsidies from the American Rescue Plan Act (ARPA) will end December 31, 2025, which might affect who enrolls and the overall risk pool.

- Rising medical and pharmacy costs due to price inflation, changes in how often services are used and new treatments.

- Changes in administrative costs, regulatory requirements, and changes in plan benefits.

All these factors have been considered in setting the new rates to ensure they are fair and stable for the market.

Medica Insurance Co:

Medica Insurance Company (MIC) is requesting a rate change for its Affordable Care Act (ACA) individual market business in Nebraska. The rate change will take effect on January 1, 2026 and will impact an estimated 26,213 members. The average rate change will be 36.1% and will result in rate changes that vary across plan designs. This includes changes to the costs of care.

MIC uses 2024 data from Nebraska to develop premium rates. This data includes estimates of changes to the below through 2026:

- Population Medica expects to insure

- Cost of medical services

- Cost of pharmacy services

- Taxes and fees

The significant factors that impact the rate change include those listed above. Claim costs per member per month are expected to change from $639.75 in 2024 to $793.45 in 2026.

In 2024, 94% of premium dollars went towards medical services after taxes and fees were removed. Under the ACA, individual products are required to pay at least 80% of premium dollars, after taxes and fees are removed, toward medical services. For 2026, MIC is expecting that 89% of premium dollars will be spent on medical services.

Medical cost changes, in both number of services and costs of services, make up the largest increase to MIC’s premium rates. Impacts due to better rates with hospitals and doctors and reviewing recent experience also aid in determining premium changes. Finally, relationships with providers are helping to improve premium rates through a lower overall cost for care.

MIC updates the plan designs offered each year, which impacts each plan’s cost-sharing (e.g. deductibles, copayments, etc.). These updates follow federal rules for how much of costs the insurance company will cover under that plan. Because these updates will vary between each plan, the rate changes will also vary by plan.

MIC expects the cost to administer coverage per member per month (PMPM) for 2026 to be $84.37, which is higher than the 2025 value of $71.47. The main drivers of MIC’s administrative expenses are employee salaries and benefits, agent commissions, claims processing/IT, and clinical/network services.

Nebraska Total Care:

(it looks like Nebraska Total Care is dropping out of the NE individual market...at least I don't see them listed in either the SERFF database or on the federal Rate Review website. I've estimated their current enrollment; see below)

Oscar Health:

(unfortunately, Oscar has redacted their enrollment data; see below)

Exhibit A summarizes the proposed rate increases by plan effective January 1, 2026. Rate increases vary by plan due to a combination of factors including shifts in benefit leveraging, cost-sharing modifications, and geographic rating factors. Using in-force business as of March 31st, 2025, the proposed average rate change for renewing plans is (REDACTED) . This rate change is absent of rate changes due to attained age.

The significant factors driving the proposed rate change include the following:

The projected premium rates reflect the most recent emerging experience which was trended for anticipated changes due to medical and prescription drug inflation and utilization.

Changes to the overall premium level are needed because of required changes in federal and state taxes and fees. In addition, there are anticipated changes in both administrative expenses and targeted risk margin.

Plan benefits have been revised as a result of changes in the Center for Medicare and Medicaid Services (CMS) Actuarial Value Calculator and state requirements, as well as for strategic product considerations.

Changes to the overall premium level are needed because of anticipated changes in the underlying morbidity of the projected marketplace.

UnitedHealthcare Insurance Co:

UHIC is filing 2026 rates for individual products. The proposed rate change is 25.03% and will affect 3,300 individuals. The rate changes vary between 18.71% and 29.08%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

UHIC does not have 2024 financial experience in Nebraska.

There are many different healthcare cost trends that contribute to increases in the overall U.S. healthcare spending each year. These trend factors affect health insurance premiums, which can mean a premium rate increase to cover costs. Some of the key healthcare cost trends that have affected this year’s rate actions include:

- Increasing cost of medical services: Annual increases in reimbursement rates to healthcare providers, such as hospitals, doctors, and pharmaceutical companies.

- Increased utilization: The number of office visits and other services continues to grow. In addition, total healthcare spending will vary by the intensity of care and use of different types of health services. The price of care can be affected using expensive procedures such as surgery versus simply monitoring or providing medications.

- Higher costs from deductible leveraging: Healthcare costs continue to rise every year. If deductibles and copayments remain the same, a higher percentage of healthcare costs need to be covered by health insurance premiums each year.

- Impact of new technology: Improvements to medical technology and clinical practice often result in the use of more expensive services, leading to increased healthcare spending and utilization.

- Expiration of enhanced premium tax credits: Expanded and enhanced federal premium tax credits for consumers will expire at the end of 2025. As a result, post-tax credit premiums will increase for calendar year 2026.(

- Changes in market morbidity: Premiums reflect the expected increase in the average cost per member due to healthier members leaving the market if enhanced APTCs are allowed to expire.

As noted above, Nebraska Total Care appears to be dropping out of the individual market, which means I don't have their current enrollment and thus can't run a fully weighted average rate change & instead have to use estimated enrollees for them. In addition, Oscar Health has redacted their current enrollment, so I again have to make an educated guess.

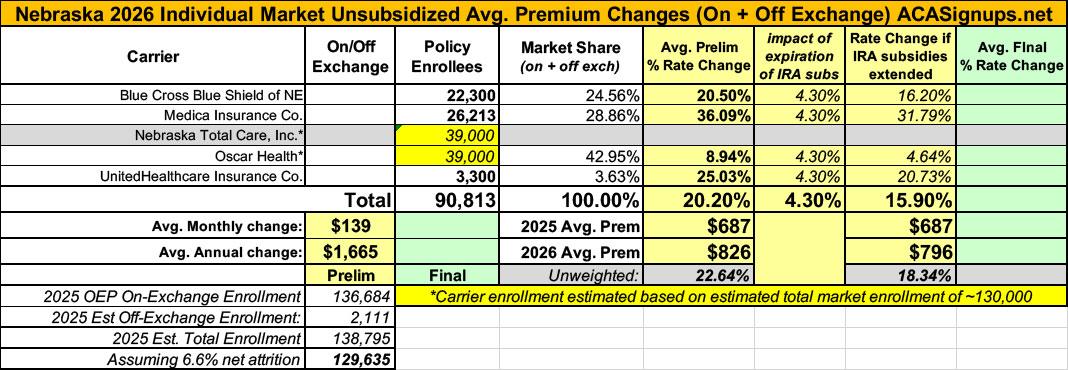

Total 2025 Open Enrollment Period (OEP) on-exchange enrollment was 136,684. Based on 2024 liability risk score data from CMS, I'm estimating perhaps another ~1,300 off-exchange enrollees, for a total individual market of roughly ~138,000 people.

There's ~51,813 enrollees across the other three carriers, which leaves roughly ~86,000 in NE Total Care & Oscar combined. If I assign them evenly (and don't include the NE Total Care number in the total, since they'll have to shop around for a new carrier), that would give a semi-weighted average rate hike being requested of 19.7%.

It's important to remember that this is for unsubsidized enrollees only; for subsidized enrollees, ACTUAL net rate hikes will likely be MUCH HIGHER for most enrollees due to the expiration of the improved ACA subsidies & the Trump CMS "Affordability & Integrity" rule changes.

Update 8/14/25: I've revised my estimate of the total market down to ~130,000, which results in a slight increase in the weighted average to +20.2%.

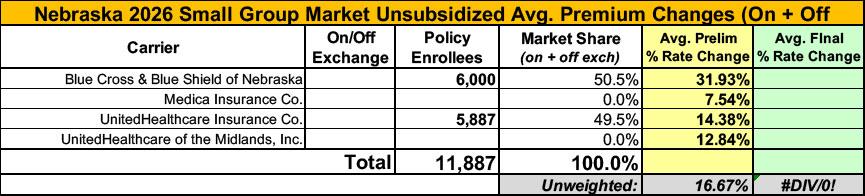

Meanwhile, I have no enrollment data at all for two of the small group carriers; the unweighted average 2026 rate hike there is around 16.7%.

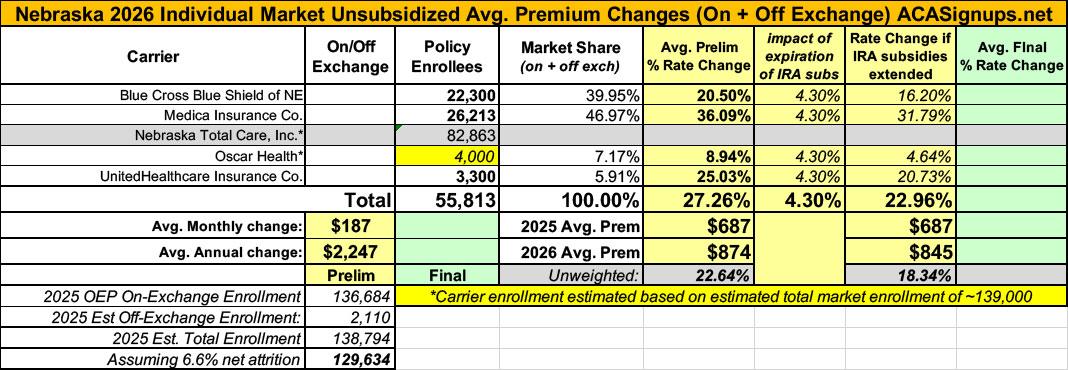

UPDATE 8/29/25: I was able to track down the withdrawal letter from Nebraska Total Care, and it turns out their current enrollment is much higher than I thought: 82,863 people.

Normally this wouldn't impact the weighted average rate increase of the other carriers since Total Care's enrollees aren't part of the denominator, but in this case it means that my estimate of Oscar Health's enrollment is way too high...and since Oscar is requesting a much lower rate hike than the other 2 remaining carriers, this means dropping Oscar down from my previous estimate of ~39,000 enrollees to ~4,000 dramatically increases the weighted marketwide average, from 20.2% to 27.3%.

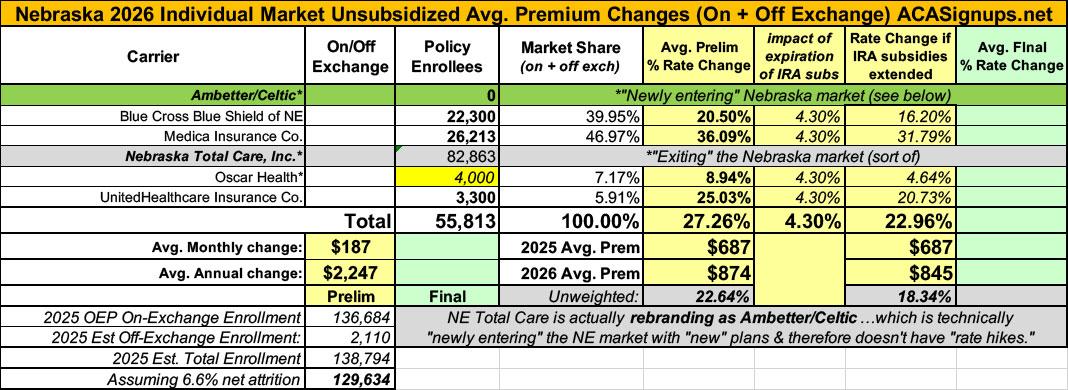

UPDATE 10/20/25: Thanks to Louise Norris for calling my attention to a closer reading of the Nebraska Total Care withdrawal letter, which states that they're actually rebranding as "Ambetter Health/Celtic Insurance" but will apparently not be kicking their current enrollees to the curb.

This is confirmed on the Ambetter website, where I found this notice:

Ambetter from Nebraska Total Care is grateful for your partnership in support of our members we serve across Nebraska. Beginning January 1, 2026, our product name is changing to Ambetter Health and our underwriting entity will change from Nebraska Total Care, Inc., to Celtic Insurance Company.

Your contract with us remains valid and no action is needed. While our brand name is getting a refresh, our commitment to delivering quality care and services to our members remains as strong as ever. Members will be notified the week of October 31 as part of the annual renewal notification process. During the Marketplace Open Enrollment Period, which occurs from Nov. 1 to Dec. 15, members will be able to select Ambetter Health for 2026. Providers should not reach out to members, however, it’s important to us that you have this information should your patients have any questions. The general terms of a member’s policy and coverage provisions will have minimal changes. However, due to the underwriting entity change, members must make their payment by Dec. 15, 2025, to keep their coverage.

The good news is that over 82,000 enrollees in Nebraska won't have to scramble to find another carrier (unless they want to). However, the way the rebranding is being done, technically speaking Ambetter is "newly entering" the Nebraska market with "new" plans and therefore doesn't have any actual "rate increase" to report since they don't have "existing" plan pricing.

This wouldn't be too irritating except that NE Total Care holds a whopping 60% of the Nebraska individual market, so that's a pretty big hole in the data, but whatever...

UPDATE 11/01/25: Just hours before the 2026 Open Enrollment Period launched, the final/approved rate filings were posted at the federal Rate Review database.

Two of the four carriers were approved pretty much as is; the other two (Oscar Health and UnitedHealthcare) saw significant increases...except that Oscar turns out to have fewer enrollees than I thought. The net result is that the average rate increase is 1.9 points higher than I had it pegged at, for a final increase of 29.1%.

| Attachment | Size |

|---|---|

| 90.01 KB | |

| 127.64 KB | |

| 291.2 KB | |

| 149.73 KB | |

| 52.19 KB |

Advertisement