Hope Floats? Bipartisan House team introduces ACA enhanced tax credit extension bill which...isn't terrible!

Fri, 11/21/2025 - 1:34pm

Back in September, before the federal government shutdown, I said:

At a bare, bare minimum, do not settle for a one- or two-year extension of the eAPTCs.

Kicking this particular can down the road for only one or two years would not only be an absolute gift to Republicans politically (since it would push the pain out until just past the midterms, which is of course the only reason why any Republicans are willing to discuss doing so at all), but it would also mean we'd be right back here with the exact same scary headlines a year or two from now, with 24 million people never knowing whether their health insurance premiums are going to skyrocket from year to year.

Nothing is worse for the insurance industry than uncertainty, and anytime they're uncertain about anything you can be sure they'll jack up rates as a "just in case" cushion.

WITH ALL THAT SAID, I could see at least some room for negotiation on the specific parameters of the permanently extended enhanced ACA tax credits.

Well, for good or for bad, the shutdown is over now and Congressional Republicans are absolutely not going to agree to a permanent extension...and so far, the only alternative they've come up with which seems to be gaining any traction is LA Sen. Bill Cassidy's "HSA's for Everything!" proposal, which would take the money currently allocated towards the enhanced premium tax credits and instead use it to cut down on deductibles, co-pays & coinsurance for enrollees in high-deductible Bronze plans instead.

As I noted in my write-up about his proposal, it isn't completely insane, but it's sorely lacking in details and there's a ton of legal & logistical stuff which would have to be fleshed out, most of which has zero chance of happening by January 1st even if his bill somehow managed to get 60 votes in the Senate, 218 in the House and was signed into law by Trump before then.

Today, however, a bipartisan House team, consisting of Democrats Tom Suozzi (NY-03) & Josh Gottheimer (NJ-05) and Republicans Don Bacon (NE-02) & Jeff Hurd (CO-03) have introduced a bill they call the "HOPE (Healthcare Optimization, Protection, and Extension) Act" which is much closer to what I described as what a reasonable compromise might look like back in September in every way but one: The timeframe, which would only be for two years.

Setting that aside for the moment, let's take a look at the bill:

Today, Congressmen Tom Suozzi (D-NY), Don Bacon (R-NE), Josh Gottheimer (D-NJ), and Jeff Hurd (R-CO) co-led the introduction of the Bipartisan Healthcare Optimization, Protection, and Extension (HOPE) Act. This bill would address the healthcare affordability crisis by extending the enhanced premium tax credits (PTCs) for two years and adding new income caps and guardrails against fraud in the process.

...The bill would extend the enhanced PTCs for enrollees earning less than $200,000 per year for a family of four. The bill would phase out the enhanced PTCs for enrollees earning between $200,000 and $300,000 for a family of four.

Moreover, the bill would create new guardrails to prevent “ghost beneficiaries,” crack down on fraud, and enhance delivery clarity. The bill cracks down on broker fraud by implementing several measures, including those presented in the Insurance Fraud Accountability Act, to codify CMS’s authority to remove bad actors from ACA marketplaces, penalize bad actors, implement new consumer protections, and more. It also directs ACA marketplaces to regularly confirm enrollee eligibility with the Death Master File and requires marketplaces to better notify recipients the value of PTCs they are receiving from the federal government.

Finally, recognizing that many would-be recipients may have been discouraged from purchasing health insurance by previously high premiums, the bill would extend open enrollment to May 15.

OK, let's look at these one at a time: As I said in September,

One criticism of the elimination of the "Subsidy Cliff" is that it's theoretically possible that a family earning up to, say, $500,000 or more could still qualify for tax credits. This is true (especially in states with insanely high gross premiums like Alaska, West Virginia and Wyoming), but it's also disingenuous since:

- a) the amount of eAPTC those households qualify for is pretty nominal (literally $5/month or less in some cases);

- b) those instances are extremely rare since you'd almost certainly have to be older than 55 or so for the benchmark plan to cost that much of your income, and almost everyone 55+ with that high of an income likely has employer benefits anyway; and

- c) people who have a corporate job which pays half a million dollars or more are likely receiving far more in tax credits via the Employer Sponsored Insurance Tax Exclusion anyway.

HOWEVER, if Republicans really want to be absolutely certain that there's no possibility whatsoever of Bill Gates or Elon Musk sponging $5/month in ACA tax credits, fine: Bring back the "Subsidy Cliff" at a much higher income threshold.

What might that look like? Well, I speculated about something like this:

While I'd prefer that the Subsidy Cliff not return at all, I could see negotiating to bring it back at a much higher income threshold...say, 1,200% FPL.

While I'd prefer to keep the high-end 8.5% of income cap locked where it is, I could see compromising at a max of 9% at 400% FPL, or perhaps adding a tier at 10% around 800% FPL or whatever.

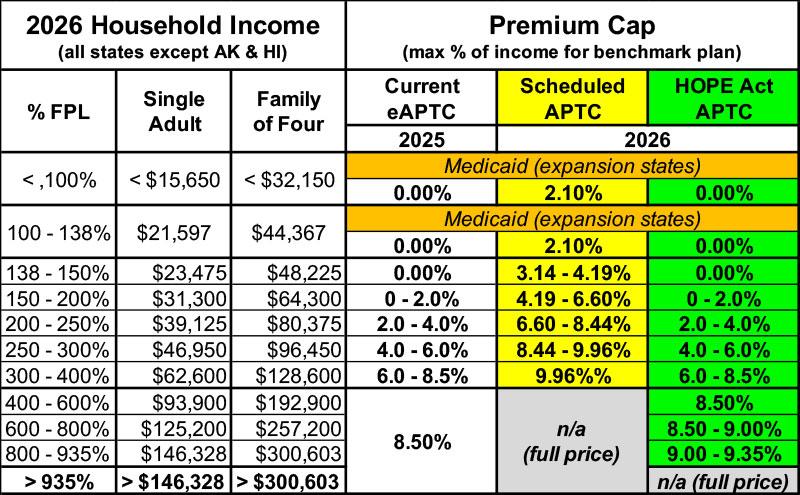

So, what does the HOPE Act tax credit subsidy table actually look like? Well, based on the actual legislative text, it would keep the enhanced tax credit formula exactly as it is now for all enrollees under 400% FPL.

For those earning more than 400% FPL, it would keep the benchmark Silver plan capped at the same 8.5% of income up to 600% FPL, after which point there'd be two more household income tiers, one at 800% FPL and one at 935% FPL...which is where the Subsidy Cliff would return & above which enrollees would have to pay full price.

Here's what it looks like in table form, side by side with the current (enhanced) Advanced Premium Tax Credit formula and what the APTC formula is scheduled to change to starting January 1st if nothing is done legislatively:

If the HOPE Act were to become law, the only changes to the subsidies from where they are right now would be from 600% FPL - 935% FPL.

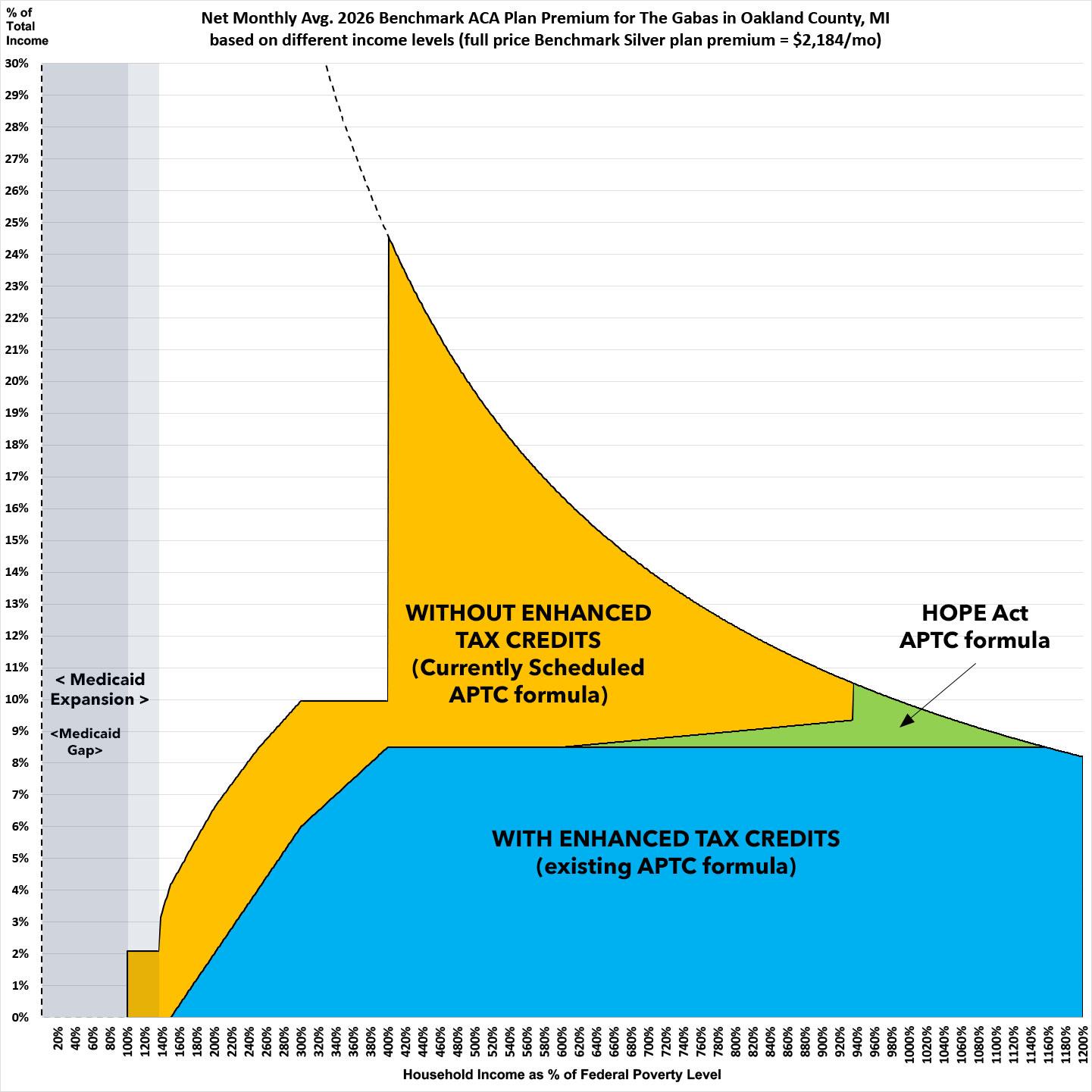

Here's what this looks like visually, using my own family here in Oakland County, Michigan. My wife and I are in our 50's and have one college-age child, and Michigan is in the middle of the pack in terms of unsubsidized ACA premiums nationally, so we make a fairly typical case study:

As you can see, our subsidy eligibility would remain exactly the same in 2026 as it is today as long as our income is below 600% FPL (around $160,000). If it ends up over that, we'd have to pay a bit more of our income, topping off at 9.35% if our household income hit exactly $249,177.50.

If we earn more than that, the subsidy cliff kicks in and we'd have to pay full price at that point...but at a quarter million dollars per year income, it'd only amount to 10.4% of it as opposed to the whopping 24.6% of our income it's currently scheduled to cost if our income is only $106,601 next year.

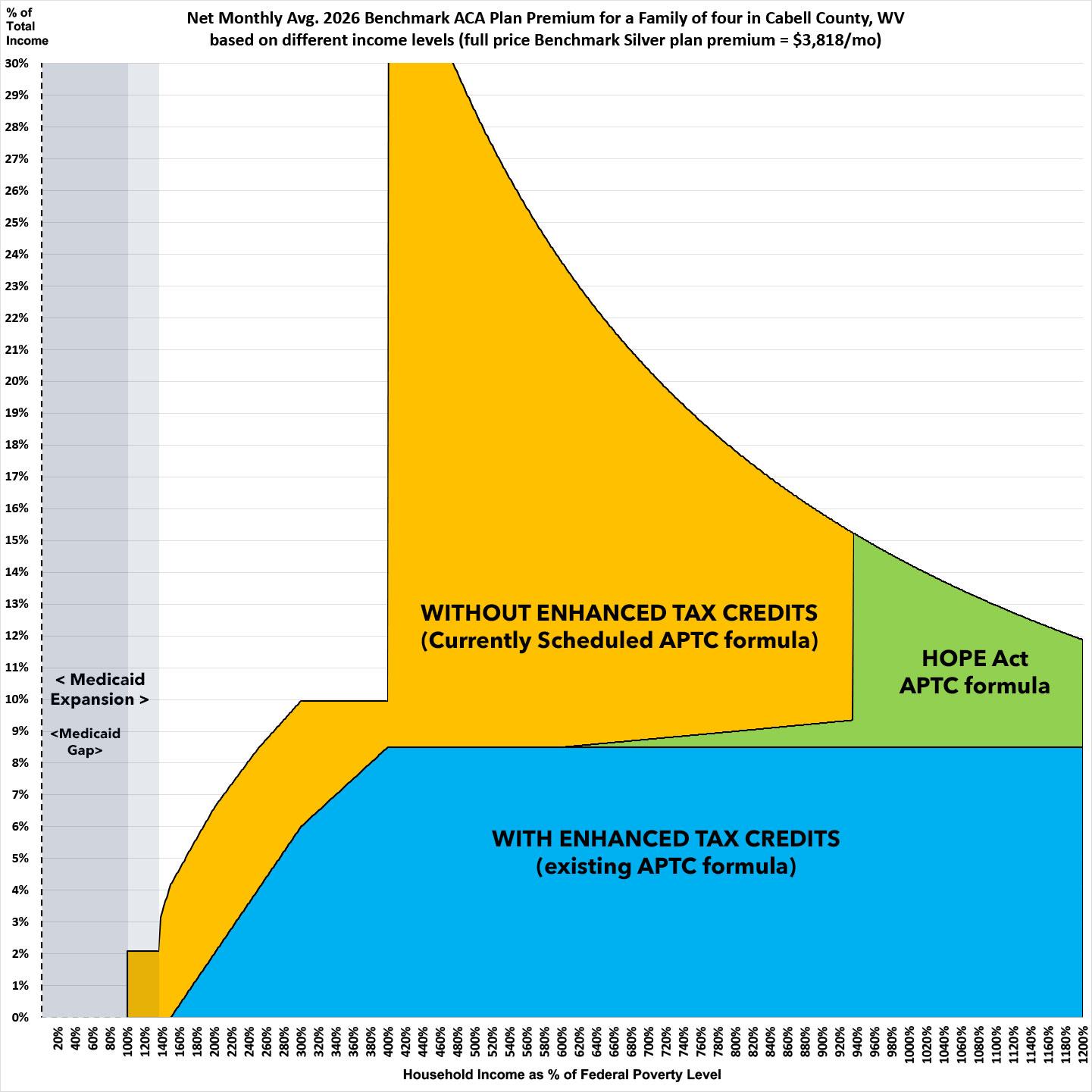

For a more dramatic example, here's a family of four (40 yr old couple with 2 children aged 15 & 12) living in the part of the country with the most expensive ACA benchmark plans I could come up with: Cabell County, West Virginia:

In this case, under the existing formula, with benchmark Silver premiums priced at a whopping $3,818/month, this household would still be receiving (nominal) tax credits if their income were as high as $539,000/year (8.5% of that would be $45,815, or $3,818/month).

Again, this family almost certainly doesn't exist, but it theoretically could, and that's one of the main gripes Republicans have.

If the enhanced tax credits expire without any action, this family will not only have to pay several times what they do now below 400% FPL, the moment that their income moves higher than 400% FPL ($128,600/yr), they're utterly screwed, as they'd fall off the subsidy cliff and would have to pay the full $45,816 in premiums...or up to 35% of their gross income.

Under the HOPE Act proposal, everything would remain as it is today until their income reaches 600% FPL ($192,900). From there up they'd have to pay a gradually increasing percent of their income up until they hit 935% FPL ($300,602/yr), at which point they'd again fall off the Subsidy Cliff...however, at that income level, the full-price benchmark plan would only cost around 15% of their income.

That's still not chump change, but it'd be a hell of a lot better than 35% of their gross income, and on an income of over $300K/year my sympathy would be a lot lower.

More importantly, again: This is an extreme edge case: only 6% of ACA exchange enrollees earn more than 800% FPL; I can't imagine that more than 2-3% earn more than 900% FPL; only a fraction of those live in states like WV, WY, VT, AK or CT (these are the only states where average ACA premiums break $1,000/month); and only a literal handful of those are gonna be older than 55 or so.

In other words, only a tiny percent of ACA enrollees would ever hit the new, 935% FPL Subsidy Cliff, and most of those who do would be able to afford it, though I'm sure they'd still grumble.

How does this compare with my hypothetical negotiation levels above?

- Well, it brings back the Cliff at 935% FPL, which is worse than I proposed (1,200% FPL).

- On the other hand, it places the highest benchmark plan cost tier at 9.35% of income, which is better than I proposed (10% of income).

Overall, this is pretty damned close to what I would propose as a reasonable compromise.

I could live with this, although again, I'd obviously want it locked in permanently instead of for just 2 years.

Next, let's look at the anti-fraud measures in the HOPE Act:

This section eats up a full 18 of the 22 pages of legislative text; here's the official summary of what they have in mind:

The bill would create new guardrails to prevent “ghost beneficiaries,” crack down on fraud, and enhance delivery clarity.

The bill cracks down on broker fraud by implementing several measures, including those presented in the Insurance Fraud Accountability Act, to codify CMS’s authority to remove bad actors from ACA marketplaces, penalize bad actors, implement new consumer protections, and more.

It also directs ACA marketplaces to regularly confirm enrollee eligibility with the Death Master File and requires marketplaces to better notify recipients the value of PTCs they are receiving from the federal government.

For example:

PENALTIES FOR AGENTS AND BROKERS

...‘‘(ii) CIVIL PENALTIES FOR CERTAIN VIOLATIONS BY AGENTS OR BROKERS.—If any agent or broker fails to provide correct information under subsection (b) or section 1311(c)(8) or other information, as specified by the Secretary, and such failure is attributable to negligence or disregard of any rules or regulations of the Secretary, such agent or broker shall be subject, in addition to any other penalties that may be prescribed by law, including subparagraph (C), to a civil penalty of not less than $10,000 and not more than $50,000 with respect to each individual who is the subject of an application for which such incorrect information is provided.’’;

...Any agent or broker who knowingly provides false or fraudulent information under subsection (b) or section 1311(c)(8), or other false or fraudulent information as part of an application for enrollment in a qualified health plan offered through an Exchange, as specified by the Secretary, shall be subject, in addition to any other penalties that may be prescribed by law, including subparagraph (C), to a civil penalty of not more than $200,000 with respect to each individual who is the subject of an application for which such false or fraudulent information is provided.

In other words, brokers/agents who commit fraud will be subject to up to a $10K - $50K fine for failing to provide accurate information due to negligence/disregard of the rules, and up to a $200K fine for deliberately committing fraud (I'm a little fuzzy about what the actual distinction between these two is).

In addition, in extreme cases they may very well go to prison for up to ten years:

CRIMINAL PENALTIES.—Any agent or broker who knowingly and willfully provides false or fraudulent information under subsection (b) or section 1311(c)(8), or other false or fraudulent information as part of an application for enrollment in a qualified health plan of fered through an Exchange, as specified by the Secretary, shall be fined under title 18, United 22 States Code, imprisoned for not more than 10 years, or both.’

I'm not an attorney or an insurance broker and I haven't read over the text too deeply yet, so I have to be careful about drawing any conclusions about this section, but I'd say that a $10K - $200K civil penalty and the possibility of actually going to prison for up to 10 years should be pretty damned effective at stopping broker/agent fraud, I would imagine.

Again, I'm not a lawyer or broker, but the initial response from a professional insurance broker friend of mine who specializes in ACA enrollment is that there are no immediate red flags which jump out.

Next, it goes into "Consumer Protections" which include stuff like:

...the Secretary shall establish a verification process for new enrollments of individuals in, and changes in coverage for individuals under, a qualified health plan offered through such Exchange, which are submitted by an agent or broker in accordance with section 1312(e) and for which the agent or broker is eligible to receive a commission.

...The enrollment verification process under subparagraph (A) shall include—

‘‘(i) a requirement that the agent or broker provide with the new enrollment or coverage change such documentation or evidence (such as a standardized consent form) or other sources as the Secretary determines necessary to establish that the agent or broker has the consent of the individual for the new enrollment or coverage change;

‘‘(ii) a requirement that any commissions due to a broker or agent for such new enrollment or coverage change are paid after the enrollee has resolved all inconsistencies in accordance with paragraphs (3) and (4) of section 1411(e);

‘‘(iii) a requirement that the information required under clause (i) and, as applicable, the date on which inconsistencies are resolved as described in clause (ii), is accessible to the applicable qualified health plan through a database or other resource, as determined by the Secretary, so that any commissions due to a broker or agent for such enrollment can be effectuated at the appropriate time;

‘‘(iv) a requirement that individuals are notified of any changes to enrollment, coverage, the agent of record, or premium tax credits in a timely manner and that such notice provides plain language instructions on how individuals can cancel unauthorized activity;

‘‘(v) a requirement that individuals be able to access their account information on a website or other technology platform, as defined by the Secretary, when used to submit an enrollment or plan change, in lieu of the Exchange website described in subsection (d)(4)(C), including information on the agent of record, the qualified health plan, and when any changes are made to the agent of record or the qualified health plan, on a consumer-facing website or through a toll-free telephone hotline; and

‘‘(vi) a requirement that the agent or broker report to the Secretary any third party marketing organization or field marketing organization (as such terms are defined in section 1312(e)) involved in the chain of enrollment (as so defined) with respect to such new enrollment or coverage change.

Again, the details matter, but the measures listed above make a lot more sense to me than forcing enrollees pay $5/month (or even $1/month) just so that they're aware that they've been enrolled in a plan or switched to a different one.

The Secretary shall ensure that the enrollment verification process under subparagraph (A) prioritizes continuity of coverage and care for individuals, including by not disenrolling individuals from a qualified health plan without the consent of the individual, regardless of whether the broker, agent, or qualified health plan is in violation of any requirement under this paragraph.

The next section gets into regulation of broker/agent marketing organizations to make sure that they're all certified and on the up & up (this section eats up several pages). Again, the details matter but generally speaking this seems reasonable to prevent scam brokers.

The next section gets into audits of insurance agents/brokers:

For plan years beginning on or after such date specified by the Secretary, but not later than January 1, 2029, the Secretary, in coordination with the States and in consultation with the National Association of Insurance Commissioners, shall implement a process for the oversight and enforcement of agent and broker compliance with this section and other applicable Federal and State law (including regulations) that shall include—

‘‘(i) periodic audits of agents and brokers based on—

‘‘(I) complaints filed with the Secretary by individuals enrolled by such an agent or broker in a qualified health plan offered through an Exchange;

‘‘(II) an incident or enrollment pattern that suggests fraud; and

‘‘(III) other factors determined by the Secretary; and

‘‘(ii) a process under which the Secretary shall share audit results and refer potential cases of fraud to the relevant State department of insurance.

Next comes the supposed "Phantom Enrollee" problem:

Not later than 90 days after the date of the enactment of this paragraph, and on a quarterly basis thereafter, the Secretary shall conduct a check of the Death Master File (as such term is defined in 2 section 203(d) of the Bipartisan Budget Act of 2013) for purposes of identifying individuals enrolled in a qualified health plan through an Exchange who are deceased.

...The Secretary shall—

‘‘(i) establish a process to verify that an individual identified pursuant to a check described in subparagraph (A) is deceased; and

‘‘(ii) require an Exchange to terminate such individual’s enrollment under a qualified health plan.’’.

Again, I have no idea how much of an issue "dead enrollees" actually are, but to the extent that they're a problem...I mean, yes, they should be removed.

CAVEAT: The one problem I could foresee would be if the insurance carrier tried to get out of paying claims on an enrollee who received medical services before they passed away...or where they were undergoing covered medical treatment at the time of their death.

STANDARD FOR TERMINATION FOR CERTAIN EXCHANGES. —In the case of an agent or broker with an agreement in effect with an Exchange operated by the Secretary pursuant to section 1321(c) to perform activities described in paragraph (1)(A)(i) with respect to such Exchange, the Secretary may terminate such agreement for cause if the Secretary finds, based on a preponderance of the evidence, that such agent or broker has violated such agreement, otherwise applicable law, or any other requirement applicable to such agent or broker.’’.

In other words, if an agent/broker is determined to be likely guilty of committing fraud, they get kicked out of the ACA enrollment program regardless of whether they're actually fined or sentenced for doing so.

The next section is kind of a head-scratcher to me, since I kind of thought this was already required, but apparently not? Huh.

EXCHANGE RESPONSIBILITIES.—Beginning January 1, 2027, if an Exchange is notified under paragraph (1) of an advance determination under section 1411 with respect to the eligibility of an individual for a premium tax credit under section 36B of the Internal Revenue Code of 1986, the Exchange shall, prior to enrolling such individual in a qualified health plan, clearly notify such individual of the amount of such tax credit.

Finally, the HOPE Act would do something very surprising to me: It would legally extend the final enrollment deadline of the 2026 Open Enrollment Period out...by four friggin' months:

The Secretary of Health and Human Services shall revise section 155.410(e) of title 45, Code of Federal Regulations (or any successor regulation) to provide that the annual open enrollment period determined for plan year 2026 pursuant to section 1311(c)(6) of the Patient Protection and Affordable Care Act (42 U.S.C. 18031(c)(6)) shall begin on November 1, 2025, and end on May 15, 2026.

Don't get me wrong, it is a good idea to bump out the final deadline for people to either enroll or switch their 2026 plan given the uncertainty going on right now, but May 15 would be a whopping 4 months from the current deadline in most states (January 15th). In fact, it would make the extended period 60% longer than the total current Open Enrollment Period, which runs around 2.5 months.

I figured that any such 11th-hour extension would only bump the final deadline out by perhaps 2 weeks or so, honestly; perhaps a month at the outside (February 15th). Huh.

In any event, as I said, there could be a poison pill buried in here, and obviously the devil is in the details regarding all of the sections on curtailing broker/agent fraud, consumer notification/protections, "phantom enrollees" etc; and that May 15th deadline extension is oddly long.

HAVING SAID THAT, assuming I'm not missing anything nefarious/problematic, the only real objection I have to this bill is that, again, it only lasts for 2 years.

Then again, that would also make the ACA tax credits as much of a hot potato in 2028 as it already is right now for 2026, so...

Advertisement