2026 FINAL Gross Rate Changes - Alabama: +21.1%; Oscar entering market (updated)

Sat, 10/18/2025 - 7:59am

Originally posted 8/8/25

Overall preliminary rate changes via the SERFF database, Alabama Insurance Dept. and/or the federal Rate Review database.

Blue Cross Blue Shield of AL

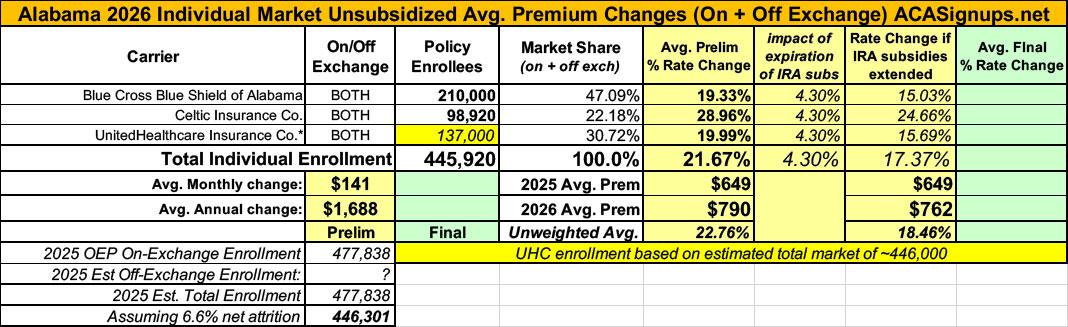

The average rate increase included in this filing is 19.3%, affecting over 210,000 members.

The main factors driving the need for this increase are:

- Alabama market membership loss and remaining members projected to be less healthy following expiration of enhanced premium subsidies in place since 2021

- Projected claim cost trends are higher for 2025 than anticipated in the 2025 filing and are projected to continue into 2026

- Administrative costs increased in 2025 and are expected to rise further in 2026 due to new eligibility and billing rules, along with a higher Exchange User Fee

...Expiring Enhanced Advance Premium Tax Credits

As of the time of this filing, Enhanced Advance Premium Tax Credits (enhanced premium subsidies) that were made available in 2021 and 2022 through the American Rescue Plan Act (ARPA) and extended by the Inflation Reduction Act (IRA) were allowed to expire by the Federal government and are not available after 2025. As a result of these enhanced premium subsidies, the total Alabama Individual ACA Market grew from 195,000 in 2021 to over 475,000 in 2025.

Assumptions in this rate filing related to this change:

- BCBSAL is projecting that a significant number of Individual members will leave the Alabama Individual ACA market in 2026 as enhanced premium subsidies become unavailable and members are no longer able to afford their out-of-pocket premiums.

- Members leaving the market are projected to be healthier than average which will leave the total Alabama market (or single rating pool) projected to be less healthy in 2026

Celtic Insurance Co:

Celtic Insurance Company is filing rates for the individual block of business, effective January 1, 2026. This document is submitted in conjunction with the Part I Unified Rate Review Template and the Part III Actuarial Memorandum.

This information is intended for use by the Alabama Department of Insurance, the Center for Consumer Information and Insurance Oversight (CCIIO), and health insurance consumers in Alabama to assist in the review of Celtic Insurance Company’s individual rate filing.

The results are actuarial projections. Actual experience will differ for a number of reasons, including population changes, claims experience, and random deviations from assumptions.

In 2024, earned premium was $645.83 per member per month (PMPM). Incurred claims in 2024 were $285.39, or 44.19% of premium. Netting risk adjustment from the claims results in an estimated loss ratio (incurred claims net of estimated risk adjustment transfers, divided by earned premiums) of 59.43%. We expect unit costs to increase for 2026. Further, we have updated underlying experience for the single risk pool, expected administrative expense, and assumptions for federal risk adjustment. These factors, as well as changes to the assumed morbidity of the single risk pool and medical trend, result in a premium rate increase.

Medical trend, or the increase in health care costs over time, is composed of two components: the increase in the unit cost of services and the increase in the utilization of those services. Unit cost increases occur as care providers and their suppliers raise their prices. Utilization increases can occur as people seek more services than before. Additionally, simple services can be replaced with more complex services over time, which is known as service intensity trend. An example of service intensity trend would be the replacement of an X-ray with an MRI scan. Replacing the service with a more intense service causes the total cost of medical services to increase.

The proposed rate change of 29.0% applies to approximately 98,920 individuals. Celtic Insurance Company’s projected administrative expenses for 2026 are $83.64 PMPM. Administrative expense does not include $40.09 for taxes and fees. The historical administrative expenses for 2025 were $73.49 PMPM, which excludes taxes and fees. The projected loss ratio is 84.8% which satisfies the federal minimum loss ratio requirement of 80.0%.

UnitedHealthcare Insurance Co:

The following memorandum describes the key drivers of the rate changes of individual rates for UnitedHealthcare Insurance Company (“UHIC”). UHIC policies are individual medical plans offered in Alabama and are fully compliant with the Patient Protection and Affordable Care Act.

Scope and Range of the Rate Increase

UHIC is filing 2026 rates for individual products. The proposed rate change is 19.99% and will affect (REDACTED) individuals. The rate changes vary between 10.88% and 25.64%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

Financial Experience of the Product

The premium collected in plan year 2024 was $1,269,406,274. Incurred claims during this period were $707,133,028 and UHC expects to pay $113,309,007 in risk adjustment. The loss ratio, or portion of premium required to pay medical claims, for plan year 2024 is 61.17%.

Changes in Medical Service Costs

There are many different healthcare cost trends that contribute to increases in the overall U.S. healthcare spending each year. These trend factors affect health insurance premiums, which can mean a premium rate increase to cover costs. Some of the key healthcare cost trends that

have affected this year’s rate actions include:

- Increasing cost of medical services: Annual increases in reimbursement rates to healthcare providers, such as hospitals, doctors, and pharmaceutical companies.

- Increased utilization: The number of office visits and other services continues to grow. In addition, total healthcare spending will vary by the intensity of care and use of different types of health services. The price of care can be affected using expensive procedures such as surgery versus simply monitoring or providing medications.

- Higher costs from deductible leveraging: Healthcare costs continue to rise every year. If deductibles and copayments remain the same, a higher percentage of healthcare costs need to be covered by health insurance premiums each year.

- Impact of new technology: Improvements to medical technology and clinical practice often result in the use of more expensive services, leading to increased healthcare spending and utilization.

- Expiration of enhanced premium tax credits: Expanded and enhanced federal premium tax credits for consumers will expire at the end of 2025. As a result, post-tax credit premiums will increase for calendar year 2026.

- Changes in market morbidity: Premiums reflect the expected increase in the average cost per member due to healthier members leaving the market if enhanced ATPCs are allowed to expire.

As noted above, UnitedHealthcare has redacted their current enrollment total, so I've had to make an educated guess in order to run a weighted average across the individual market.

Total 2025 Open Enrollment Period (OEP) on-exchange enrollment was 478,838, plus an unknown number of additional off-exchange enrollees. Since then, the April Medicaid/CHIP report says that on-exchange enrollment had dropped by around 6.6%. Based on this, I'm estimating UHC's enrollment at roughly 137,000 people.

If so, this gives a semi-weighted average rate hike being requested by Alabama carriers of 21.7%.

It's important to remember that this is for unsubsidized enrollees only; for subsidized enrollees, ACTUAL net rate hikes will likely be MUCH HIGHER for most enrollees due to the expiration of the improved ACA subsidies & the Trump CMS "Affordability & Integrity" rule changes.

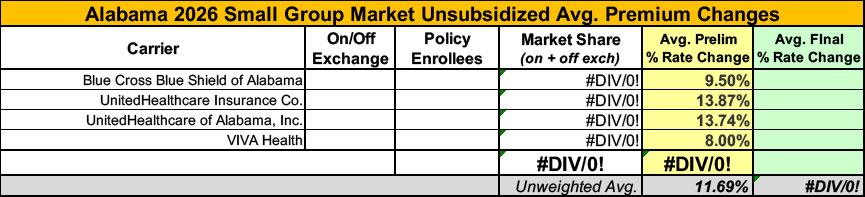

Meanwhile, I have no enrollment data at all for the small group carriers; the unweighted average 2026 rate hike there is around 11.7%

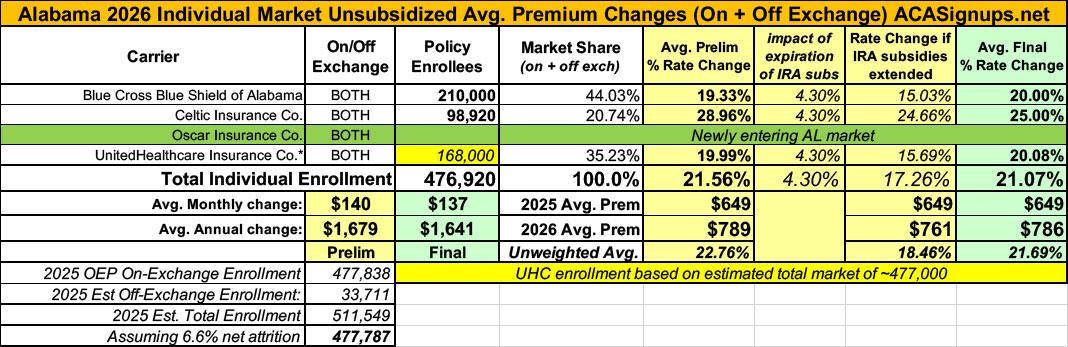

UPDATE 10/18/25: Alabama's individual market carriers have published their approved 2026 gross rate filings. The only major change was Celtic, which had their increase reduced from 29% to 25%. Overall the weighted average increase was shaved down slightly to 21.1%.

In addition, it turns out that Oscar Insurance is newly entering the Alabama market in 2026.

Here's the official press release from the Alabama DOI:

2026 ACA Rate changes for Alabama policies in the individual market

The Alabama Department of Insurance (ALDOI) has approved the revised 2026 premium rates for the Affordable Care Act Individual Market in Alabama. The rates will be effective on January 1, 2026. The four carriers in the Alabama individual market are Blue Cross Blue Shield of Alabama (BCBS), UnitedHealthcare Insurance Company (UHC), Celtic Insurance Company (CIC), and Oscar Insurance Company (Oscar).

On average, rates for BCBS increased 20.0%, rates for UHC increased 20.1%, and rates for CIC increased 25.0%. Oscar is new to the Affordable Care Act Individual Market in Alabama in 2026, and therefore, there is no rate change.

| Attachment | Size |

|---|---|

| 91.7 KB | |

| 24.42 KB | |

| 189.47 KB |

Advertisement