2026 Final Gross Rate Changes - Arizona: +46.3% (updated)

Fri, 10/10/2025 - 12:12pm

Originally posted 8/7/25

SCROLL DOWN FOR IMPORTANT UPDATES.

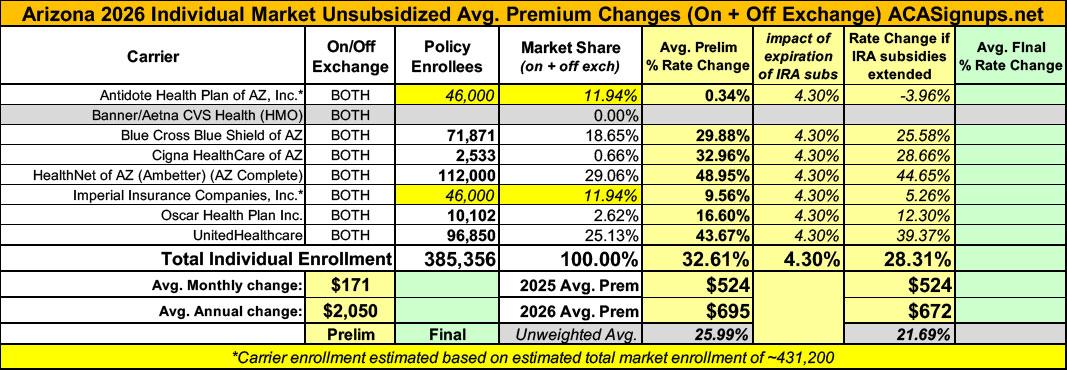

Overall preliminary rate changes via federal Rate Review database.

Antidote Health Plan of AZ:

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Banner/Aetna CVS:

(Dropping out of the individual market for 2026.)

I am writing to notify the Department that Banner Health and Aetna Health Plan Inc. (“Banner | Aetna”) will exit the individual health insurance market effective December 31, 2025. This notification is sent pursuant to Department guidance and Arizona statute 20-1380(D)(1). We made this decision after careful consideration and after evaluating the evolution of business at Banner | Aetna. The details of our individual market exit include the following:

- 1. Number of Lives Impacted: 55,553 (includes both on- and off-exchange)

- 2. Effective Date of Non-renewal: January 1, 2026.

- 3. Line of Business Impacted: Individual HMO

Blue Cross Blue Shield of AZ:

BCBSAZ is filing an average rate increase for plans in the Arizona Individual market of 29.88%, varying between 14.7% and 38.6%, excluding federally prescribed age factors. The average increase is calculated from the most recently implemented rates which were effective January 1, 2025. This increase will be effective on January 1, 2026 and will affect 71,871 Arizona policyholders (as of March 2025).

Cigna Healthcare of AZ:

Cigna estimates that 2,533 customers will be impacted by this rate increase. On average, customers will see an increase of 32.96%, excluding the impact of aging, with a range of increases from 16.87% to 42.64%. In addition to the factors described below, each customer’s rate increase depends on factors such as where they live and what plan they are enrolled in.

Ambetter/AZ Complete Health:

Arizona Complete Health (AZCH) currently provides health care coverage for over 112,000 members enrolled in our Ambetter plans. Premium rates are expected to increase on average by 49.0% for members on renewing plans, effective January 1, 2026. Annual rate changes may range between 36.8% and 57.1%, depending on what county current enrollees reside in and their current plan selection. Variations are primarily driven by underlying cost differences between different plan designs and regional cost trends. Note that these rate changes do not reflect any additional increases in a member’s calculated premium driven by aging an additional year at the point of renewal.

Imperial Insurance Companies, Inc:

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Oscar Health Plan Inc:

The purpose of this document is to present rate change justification for Oscar Health Plan, Inc. (Oscar’s) (HIOS ID 13877) Individual Affordable Care Act (ACA) products, with an effective date of January 1, 2026, and to comply with the requirements of Section 2794 of the Public Health Service Act as added by Section 1003 of the Patient Protection and Affordable Care Act (ACA).

Using in-force business as of March 2025 , the proposed average rate increase for renewing plans is 16.6%. Rate increases vary by plan due to a combination of factors including shifts in benefit leveraging and cost-sharing modifications. This rate increase is absent of rate changes due to attained age.

The rate increase impacts an estimated 10,102 members.

UnitedHealthcare:

Scope and Range of the Rate Increase

UHCAZ is filing 2026 rates for individual products. The proposed rate change is 43.67% and will affect 96,850 individuals. The rate changes vary between 41.29% and 53.76%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

As noted above, one carrier (Aetna/CVS/Banner) is dropping out of the individual market with 55,553 enrollees who have to shop around for a new carrier. Note that those enrollees aren't included in the weighted average at all.

Two others (Antidote and Imperial) have redacted their enrollment figures. This means I can't run a fully weighted average rate change and instead have to use estimated enrollees for them. Total 2025 Open Enrollment Period (OEP) on-exchange enrollment was ~423,000; assuming roughly another ~8,000 off-exchange enrollees (based on 2024 liability risk score data from CMS) gives a total of around ~431,200 individual market enrollees.

This leaves around ~82,200 exchange enrollees unaccounted for. If I assume equal enrollment in each of the "blank" carriers, that means roughly 41,100 apiece.

This puts the weighted statewide average preliminary rate increase at 32.6%.

Update 7/14/25: Not sure if I missed this or if it was changed, but Antidote's rate hike has changed from 0.34% to 6.51%.

In addition, I've modified my estimated enrollment for Antidote and Imperial to reflect CMS's April 2025 Medicaid/CHIP report that national ACA exchange enrollment has dropped by 6.6% nationally.

These two changes raise Arizona's weighted average rate increase to 36.1%.

The table below has been updated.

It's important to remember that this is for unsubsidized enrollees only; for subsidized enrollees, ACTUAL net rate hikes will likely be MUCH HIGHER for most enrollees due to the expiration of the improved ACA subsidies & the Trump CMS "Affordability & Integrity" rule changes.

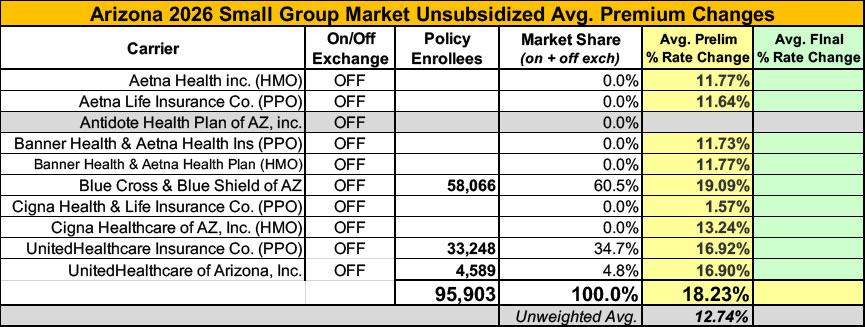

Meanwhile, I have no enrollment data for most of the small group carriers; the unweighted average 2026 rate hike there is 12.7%

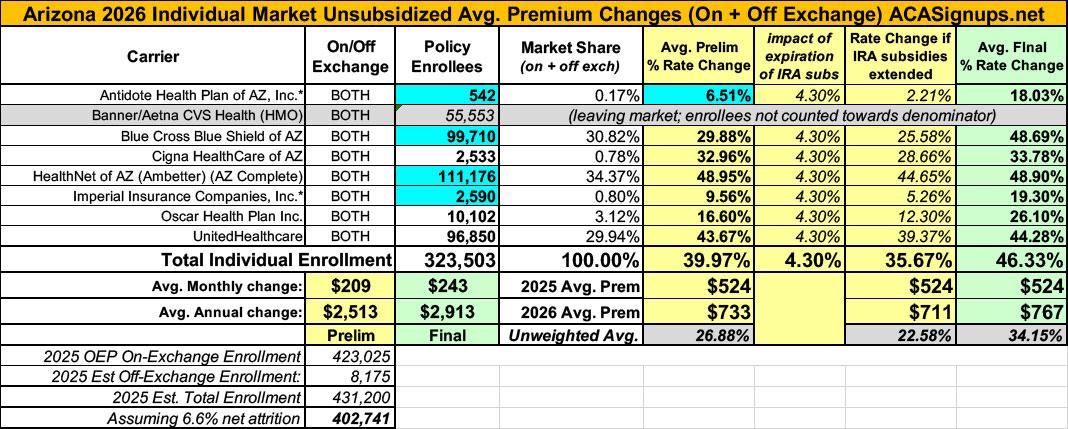

UPDATE 10/10/25: Hoo boy. Arizona's individual market insurance carriers have uploaded their final, approved 2026 rate filings to the SERFF database, and it's uglier than I already estimated.

Normally for the final filings I just post an updated version of the spreadsheet, but under the circumstances I want to be as transparent as possible, so I'm posting the confirmation from the carrier rate filings as well:

- "Antidote’s average proposed rate increase of 18.03%, effective January 1, 2026, is expected to impact 542 members based on March 2025 membership. The rate increase is the same for all adult members within a given plan, though it varies by plan, ranging between 14.50% and 23.96%. Rate changes vary by plan due to the impact of changes in benefits, changes to profit by metal, and changes to the Cost Sharing Reduction (CSR) shortfall load."

"BCBSAZ is filing an average rate increase for plans in the Arizona Individual market of 48.69%, varying between 31.3% and 58.7%, excluding federally prescribed age factors. The average increase is calculated from the most recently implemented rates which were effective January 1, 2025. This increase will be effective on January 1, 2026 and will affect 71,871 Arizona policyholders* (as of March 2025). The following considerations were included in the development of the filed rates."

*Another BCBSAZ filing form lists the total actual number of covered lives as 99,710.

"Cigna estimates that 2,533 customers will be impacted by this rate increase. On average, customers will see an increase of 33.78%, excluding the impact of aging, with a range of increases from 17.06% to 42.87%. In addition to the factors described below, each customer’s rate increase depends on factors such as where they live and what plan they are enrolled in."

"Arizona Complete Health (AZCH)* currently provides health care coverage for over 112,000 members enrolled in our Ambetter plans. Premium rates are expected to increase on average by 49.0% for members on renewing plans, effective January 1, 2026. Annual rate changes may range between 36.8% and 57.1%, depending on what county current enrollees reside in and their current plan selection."

*AZCH is also known as HealthNet of Arizona via Ambetter; another filing form in the package lists the exact number of enrollees as 111,176.

"Imperial Insurance Companies, Inc. (Imperial) has submi ed its 2026 filing for its Individual HMO product. The weighted average premium increase is 19.3%, with a minimum and maximum increase by plan of 1.29% and 21.64% respectively.

Note: The summary memo doesn't include the number of enrollees, but that's listed on another form in the filing package as just 2,590.

OSCAR HEALTH PLAN, INC: Using in-force business as of March 2025 , the proposed average rate increase for renewing plans is 26.1%. Rate increases vary by plan due to a combination of factors including shifts in benefit leveraging and cost-sharing modifications. This rate increase is absent of rate changes due to attained age. The rate increase impacts an estimated 10,102 members.

UHCAZ is filing 2026 rates for individual products. The proposed rate change is 44.28% and will affect 96,850 individuals. The rate changes vary between 41.16% and 53.60%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

In short, the final, approved filings are higher than the preliminary filings for 6 of the 7 carriers...and are dramatically higher for several of them, including Antidote (form 6.5% to 18.0%), BCBS (from 29.9% to 48.7%), Imperial (from 9.6% to 19.3%) and Oscar (from 16.6% to 26.1%).

In addition, both of the carriers which I had to estimate the enrollment numbers for turned out to have far lower enrollee totals than I thought: Antidote only has 542 while Imperial only has 2,590...and as it happens, these are also the two carriers with the lowest avg. approved rate increases (18.0% & 19.3% respectively).

The combination of all of these factors means that the preliminary weighted average rate increase was actually 40.0% (vs. my 36.1% estimate)...and the final, approved average increase is a jaw-dropping 46.3%.

| Attachment | Size |

|---|---|

| 1.34 MB | |

| 125.79 KB | |

| 319.53 KB | |

| 81.22 KB | |

| 174.44 KB | |

| 259.52 KB | |

| 106 KB | |

| 153.49 KB | |

| 83.06 KB | |

| 103.87 KB | |

| 242.31 KB | |

| 319.53 KB | |

| 660.28 KB | |

| 96.47 KB | |

| 195.03 KB |

Advertisement