2026 Final Gross Rate Changes - Mississippi: +43.4%; ~330,000 enrollees facing MASSIVE rate hikes starting in January (updated)

Fri, 10/31/2025 - 7:56am

Originally posted 8/08/25

Overall preliminary rate changes via SERFF database, Mississippi Insurance Dept. website and/or the federal Rate Review database.

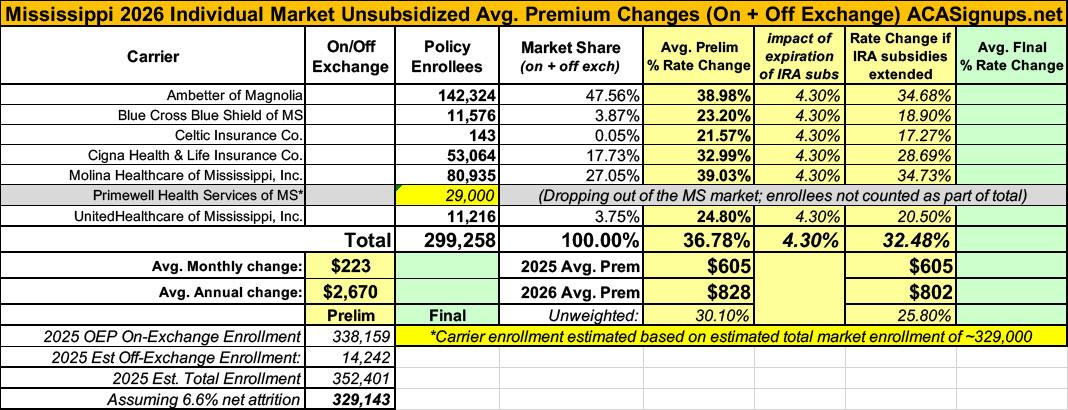

Ambetter of Magnolia Inc.

The proposed rate change of 39.0% applies to approximately 142,324 individuals. Ambetter of Magnolia Inc.’s projected administrative expenses for 2026 are $89.76 PMPM. Administrative expense does not include $34.22 for taxes and fees. The historical administrative expenses for 2025 were $73.84 PMPM, which excludes taxes and fees. The projected loss ratio is 84.4% which satisfies the federal minimum loss ratio requirement of 80.0%.

Blue Cross Blue Shield of MS:

The 2026 monthly health insurance premium is made up of four pieces: estimated claim costs, administrative costs, taxes and fees, and risk/profit margin.

Scope and range of the rate increase: The premium rate change from 2025 to 2026 is 23.2% for renewing members. The number of individuals impacted by the rate increase is 11,576. The increase varies by plan from 18.4% to 32.0%.

Financial experience of the product: Financial experience of the product: Blue Cross Blue Shield of Mississippi’s individual federal minimum loss ratio (MLR) has consistently run well above 80%. The 2026 rate increase is expected to produce a 1.0% profit and risk margin after taxes.

Changes in medical service costs: The main contributor to the change in rates is a year of medical and pharmacy trend, driven by utilization increases and provider reimbursement changes.

Changes in benefits: Additionally, two new plans were added and the Blue Care Health Savings 3100 plan increased the deductible (now Blue Care Health Savings 3300). Benefit changes are expected to have a small impact on premium

Administrative costs and anticipated margins: Administrative costs per member are decreasing in 2026 by 1.5% of premium over the prior filing. There are negligible differences to taxes and fees included within the 2025 and 2026 premium rates. Anticipated margin for this filing is 1.0% after taxes.

Celtic Insurance Company

The proposed rate change of 21.6% applies to approximately 143 individuals. Celtic Insurance Company’s projected administrative expenses for 2026 are $80.34 PMPM. Administrative expense does not include $16.94 for taxes and fees. The historical administrative expenses for 2025 were $76.38 PMPM, which excludes taxes and fees. The projected loss ratio is 83.6% which satisfies the federal minimum loss ratio requirement of 80.0%.

Cigna:

Cigna estimates that 53,064 customers will be impacted by this rate increase. On average, customers will see an increase of 33%, excluding the impact of aging, with a range of increases from 25% to 42%. In addition to the factors described below, each customer’s rate increase depends on factors such as where they live and what plan they are enrolled in.

The most significant factors causing the rate increase are:

- Expiration of APTC Subsidies: This rate filing assumes that APTC subsidies will expire on 12/31/2025. The conclusion of the enhanced subsidies is expected to lower enrollment and increase the average statewide morbidity.

- Changes in Medical Service Costs: The increasing cost of medical and pharmacy services and supplies impacts the premium rate increases. Cigna anticipates that the cost of medical and pharmacy services and supplies in 2026 will increase over the 2024 level because the prices charged by doctors, hospitals, and other providers are increasing. Additionally, the more frequent use of medical services by customers also increases Cigna's costs. The recent increase in Consumer Price Index (CPI) inflation is adding additional inflationary pressure for network contracts and provider payment mechanisms.

- Changes for the healthiness of the population: The health exchanges for individual plans continue to evolve, following the introduction of the Patient Protection and Affordable Care Act. The overall health of the population is significantly impacted by changes in:

- enrollment decreases from year to year, as this tends to increase the average healthcare cost of the remaining market enrollees

- anticipated changes to regulations regarding things like Short Term Medical and Association Health Plans that will impact the Affordable Care Act population are likely to attract healthier consumers away from the individual market, which increases the average healthcare cost per customer

Molina Healthcare of Mississippi, Inc.

1. Scope and range of the rate increase: Molina’s proposed rates represent an overall rate change of 39.0% for the 80,935 Molina members enrolled in continuing plans effective March 2025. The proposed rate changes vary by metal tier. Members would receive premium changes ranging from 15.7% to 57.3% depending on their geographic location, metal tier, and age.

...3. Changes in Medical Service Costs: Medical inflation related to the utilization and cost of covered services increased claims by 10.6%. Historical medical and pharmacy claims experience and prospective trend are the primary contributors to an increase in rates. Changes in provider contracting rates also contribute to the regional rate changes.

4. Changes in Benefits: Molina is renewing nine gold, silver, and bronze plan offerings from 2025. The impact on rates from benefit design changes for all renewal plans is minimal.

5. Administrative costs and anticipated profits: Total administrative expenses are expected to decrease, contributing to a decrease in rates of approximately 0.8%. Targeted profit margin remains the same as the prior year’s filing.

6. Program Changes: The expiration of the enhanced Premium Tax Credits (eAPTCs) and Program Integrity will lead to people leaving Marketplace, with a higher skew of healthier people leaving and therefore driving up the acuity in the risk pool

UnitedHealthcare Insurance Company

Scope and Range of the Rate Increase

UHCMS is filing 2026 rates for individual products. The proposed rate change is 24.80% and will affect 11,216 individuals. The rate changes vary between 19.47% and 27.94%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

...Some of the key healthcare cost trends that have affected this year’s rate actions include:

- Increasing cost of medical services: Annual increases in reimbursement rates to healthcare providers, such as hospitals, doctors, and pharmaceutical companies.

- Increased utilization: The number of office visits and other services continues to grow. In addition, total healthcare spending will vary by the intensity of care and use of different types of health services. The price of care can be affected using expensive procedures such as surgery versus simply monitoring or providing medications.

- Expiration of enhanced premium tax credits: Expanded and enhanced federal premium tax credits for consumers will expire at the end of 2025. As a result, post-tax credit premiums will increase for calendar year 2026.

- Changes in market morbidity: Premiums reflect the expected increase in the average cost per member due to healthier members leaving the market if enhanced ATPCs are allowed to expire.

It also looks as though Primewell Health Services is dropping out of the individual market.

Total 2025 Mississippi Open Enrollment Period (OEP) on-exchange enrollment was 338,159. I'm assuming another ~14,000 off-exchange enrollees (based on 2024 liability risk score data from CMS), minus 6.6% net attrition thru April (via CMS) for a total of around ~330,000 individual market enrollees.

This would put Primewell at perhaps ~52,000 enrollees who will have to shop around for another carrier for 2026, although they aren't included in the weighted average at all.

This puts the semi-weighted average requested rate hike at ~36.8%.

It's important to remember that this is for unsubsidized enrollees only; for subsidized enrollees, ACTUAL net rate hikes will likely be MUCH HIGHER for most enrollees due to the expiration of the improved ACA subsidies & the Trump CMS "Affordability & Integrity" rule changes.

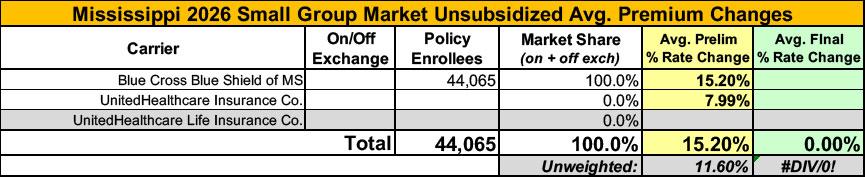

Meanwhile, I have no enrollment data at all for the small group carriers; the unweighted average 2026 rate hike there is around 11.6%

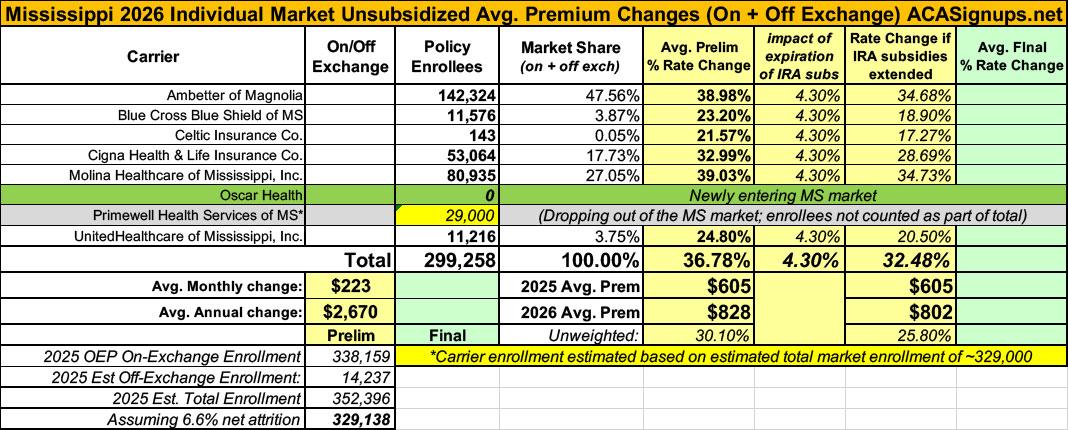

UPDATE 10/20/25: Thanks to my colleague Louise Norris for pointing me towards this post from Agility Insurance Services noting that Oscar Health is expanding into the Mississippi ACA individual market for 2026:

Oscar Health, one of the leading ACA insurance marketplace carriers in the nation, is expanding into Alabama and Mississippi for 2026. Oscar Health will be entering the following counties in each state:

Mississippi

- Jackson (Rating Area 3): Hinds, Madison, Rankin, and Warren Counties.

- Northern MS (Rating Area 1): DeSoto, Marshall, Tate, and Tunica Counties.

- Benton, Lafayette, and Panola Counties.

The key provider partners in these Mississippi counties will be Baptist Health and Merit Health (Community Health Systems).

I had already noted Oscar's expansion into Alabama. I'm still waiting on the final/approved rates for Mississippi, so this is a pretty minor update for now:

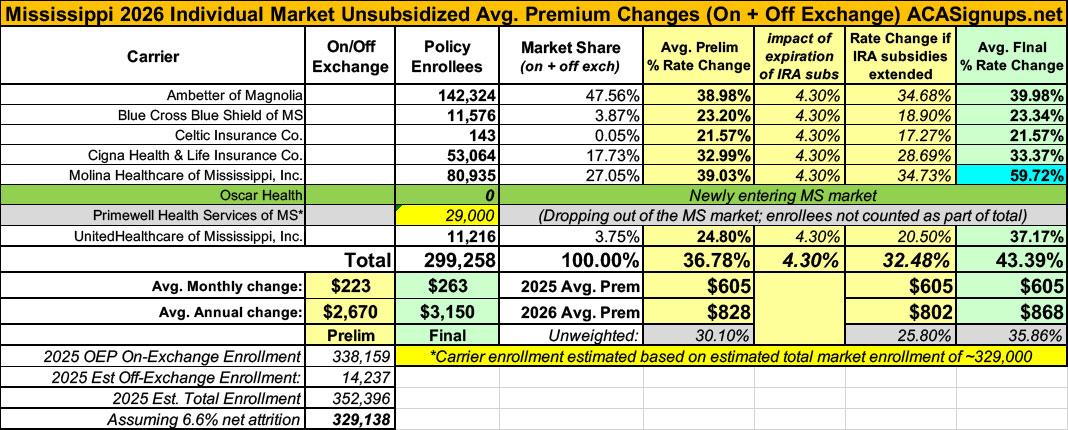

UPDATE 10/31/25: On the eve of Open Enrollment launching, the federal Rate Review database has finally been updated with the final, approved 2026 rate filings for every state, allowing me to fill in Mississippi.

Four of the six MS carriers were approved pretty much as is, but UnitedHealthcare's increase jumped dramatically from 24.8% to 36.2%...and MOLINA Healthcare was raised by a stunning ~21 points, from 39% to 59.7%

As a result, Mississippi's overall weighted gross average premium increase ends up going from "only" 36.8% to a whopping 43.4% (which, amazingly, still leaves it as the 2nd highest avg. percent rate increase nationally after Arizona).

| Attachment | Size |

|---|---|

| 24.31 KB | |

| 138.92 KB | |

| 24.27 KB | |

| 162.49 KB | |

| 117 KB | |

| 355.89 KB | |

| 41.06 KB | |

| 319.31 KB |

Advertisement