2026 Final Gross Rate Changes - New Hampshire: +17.3%; ~80,000 enrollees facing MASSIVE rate hikes starting in January (updated)

Sat, 11/01/2025 - 9:56am

Originally posted 8/08/25

Overall preliminary rate changes via the SERFF database, New Hampshire Insurance Dept. and/or the federal Rate Review database.

Anthem Health Plans of NH (BCBS)

(Unfortunately, Anthem has redacted their current enrollment total; see below)

This is a rate filing for the Individual market ACA-compliant plans offered by Anthem Health Plans of New Hampshire, Inc., also referred to as Anthem. The policy forms associated with these plans are listed below. The proposed rates in this filing are for a new HMO product that will be effective for the 2026 plan year beginning January 1, 2026, and apply exclusively to off-exchange plans.

Per the filing requirements from New Hampshire Bulletin #INS 25-023-AB, two rate scenarios will be submitted for on-exchange business. The first reflects the continuation of enhanced ACA premium tax credits into the 2026 plan year, which requires an act of congress. The second reflects the expiration of enhanced ACA premium tax credits on December 31, 2025, which is in accordance with current regulation as of July 25, 2025. Since all plans issued in this filing are off-exchange only, the status of the enhanced ACA premium tax credits extension is not applicable. Therefore, only one rate scenario is provided.

In addition, New Hampshire has a Section 1332 State Innovation Waiver for a reinsurance program in the individual ACA market. The reinsurance program is expected to reimburse 41% of paid claims between $60,000 and $400,000 in 2026. The rates included in this filing reflect these reinsurance parameters. A separate rate template without the impact of the reinsurance program is included in the Supporting Documentation tab in SERFF. If the reinsurance parameters change, the rates contained in this filing may require revision.

...Anthem offers ACA plans in the Individual market through two different legal entities in New Hampshire: Anthem Health Plans of New Hampshire, Inc. and Matthew Thornton Health Plan, Inc. This rate filing pertains to the Individual market ACA-compliant plans offered by Anthem Health Plans of New Hampshire, Inc.

The Individual off-exchange EPO product offered in plan year 2025 is being terminated, and a new off-exchange HMO product will be introduced for plan year 2026 under this legal entity. The 2024 Individual ACA experience from Anthem Health Plans, also known as the experience rate, has been assigned 0.00% credibility in the rate development since it is not fully credible nor representative of the new Individual HMO off-exchange product being offered in 2026. The proposed rates for the new HMO product have been developed from a manual rate based on Anthem's 2024 ACA Individual off-exchange HMO experience with Matthew Thornton Health Plan. The development of the experience rate and manual rate are described in sections 6 and 7.

The proposed annual rate change for the product in this filing is (REDACTED). This methodology aligns with the Unified Rate Review Template. The annual rate change was derived, per guidance, by mapping the terminated EPO plans offered in 2025 plan year to the new HMO plans offered by this legal entity in 2026 plan year. Consequently, the HMO plans incorporating EPO membership and experience are categorized as Renewing in the URRT despite being new plans. Exhibit A shows the rate change for each plan.

Boston Medical Center / WellSense

(Unfortunately, BMC/WellSense has redacted their current enrollment total; see below)

Celtic Insurance Co

Celtic Insurance Company is filing rates for the individual block of business, effective January 1, 2026. This document is submitted in conjunction with the Part I Unified Rate Review Template and the Part III Actuarial Memorandum.

This information is intended for use by the New Hampshire Insurance Department, the Center for Consumer Information and Insurance Oversight (CCIIO), and health insurance consumers in New Hampshire to assist in the review of Celtic Insurance Company’s individual rate filing. The proposed rate change of 35.8% applies to approximately 25,683 individuals.

The results are actuarial projections. Actual experience will differ for a number of reasons, including population changes, claims experience, and random deviations from assumptions. This rate change reflects expected increases in the cost of providing coverage in the individual market. The primary factors contributing to the proposed rate increase include:

- Statewide Average Morbidity (SWAM) projection. SWAM has emerged as the primary driver of the change. 2025 Wakely data shows 2025 statewide morbidity trending well above initial projections and exceeding 2026 expectations. Our 2026 projected statewide morbidity trend was updated for market dynamics and a deteriorating risk pool.

- Statewide Average Premium (SWAP) projection. The filing reflects updates to SWAP assumptions to align premiums with the elevated statewide morbidity and corresponding increase in anticipated market-wide claims costs. Specifically, the projected 2026 SWAP has increased reflecting the deteriorating risk pool and associated cost pressures.

Contributing to the projected SWAM is the expected expiration of the Enhanced Advance Premium Tax Credits. The federal eAPTCs, which have existed since 2021, are currently scheduled to expire at the end of 2025. With the expected expiration, net premiums are projected to rise significantly for many enrollees. This is anticipated to result in adverse selection, as healthier and more price sensitive individuals are more likely to forgo coverage, leading to a higher average morbidity within the individual market risk pool.

The resulting shift in risk is expected to contribute materially to higher claims costs and overall premium requirements for 2026. In addition to these drivers, annually rising medical costs continue to affect premiums. Some of these drivers include increases in the price of services, the number of services used, and the shift toward more complex and intensive treatments. This filing reflects the cost of providing comprehensive health coverage in the individual market under current federal and state policy expectations.

Harvard Pilgrim Health Care

Scope and range of the rate increase: Harvard Pilgrim Health Care (HPHC) is filing rates for Individual policyholders renewing in the first quarter of 2026. For existing plans, annual rate increases by plan range from 32.6% to 54.9%, before the impact of demographic changes. Our expected average rate increase for renewing policyholders is 42.4%. There are currently 2,382 policyholders and 3,623 members with HMO products that will be impacted by the filed rate increases. Rate increases vary by plan due to changes in benefit design that vary by plan, updated underlying benefit pricing assumptions, and updated Silver benefit pricing assuming CSR will not be funded. Increases will also vary depending on members’ age.

Matthew Thornton Health Plan (Anthem)

Matthew Thornton Health Plan, Inc., also referred to as Anthem, has made an application to the New Hampshire Insurance Department for premium rate changes for its fully ACA-compliant individual health plan products. This increase will impact approximately 29,500 New Hampshire insured members renewing on 1/1/2026 with Anthem. At the individual plan level, rate increases range from 14.4% to 34.0%. A subscriber’s actual rate could be higher or lower depending on the age characteristics, dependent coverage, and other factors. Anthem expects some members to have an increase over 15%.

Financial Experience

Anthem expects the proposed rate increase will cover projected medical trends and yield a medical loss ratio of 84.6%, meaning about eighty-five cents of each premium dollar are expected to go towards covering our members’ medical expenses and improving health care quality. This projected MLR of 84.6% exceeds the minimum MLR requirement of 80% as defined in the Affordable Care Act (ACA). In the event Anthem’s MLR is less than the Federal required minimum for a three-year period, Anthem will refund the difference to policyholders, consistent with federal regulations.

Drivers of Rate Increase

The primary drivers of premium increases are associated with increased cost of benefit expense for this ACA‐compliant block. Increased cost of benefit expense is driven by increases in the price of services primarily from hospitals, physicians, and pharmacies, coupled with members increasing their use of health care services, also called “utilization.” Increases in the price of services are driven by technological advances, new specialty medications, and a variety of other factors. Increased utilization is driven by member level utilization and selection patterns in the guaranteed issue ACA market.

Efforts to Control Costs

Anthem is committed to working to hold down the cost of insurance and price the individual ACA market for long term sustainability. We continue to explore innovative collaboration with providers and negotiate deeper discounts at our hospitals. We provide members with tools to make informed decisions about where and how to receive treatment. Despite these efforts to moderate the cost of insurance, the cost of benefit expense in the individual ACA market has continued to outpace premium on a large scale due to the drivers described above. In light of emerging costs, 2026 premium increases are needed to price Anthem’s ACA-compliant individual health plan products for long term sustainability.

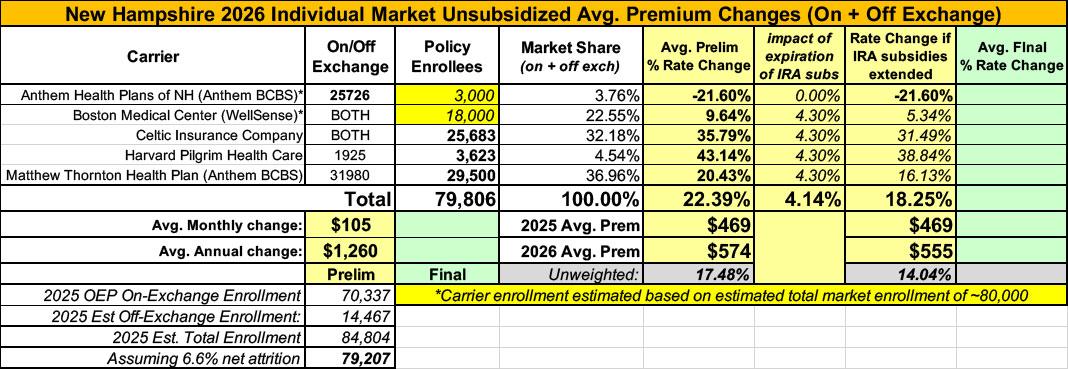

As noted above, unfortunately, the actual current enrollment is redacted for two of the 5 carriers in the NH market (Anthem and BMC/WellSense).

In order to run a semi-weighted average, I first used 2024 CMS liability risk score data to estimate/extrapolate roughly 85,000 total 2025 individual market enrollees. Since the remaining 3 carriers report ~59,000 enrollees, that leaves around ~26,000 unaccounted for.

Normally at this point I would split that between the two remaining carriers, except that Anthem is only offering off-exchange plans, which means they should have a far smaller enrollment tally. I'm therefore assuming roughly a 4,000/22,000 split between the two.

If so, this would give a semi-weighted average individual market rate increase of ~21.3%.

It's important to remember that this is for unsubsidized enrollees only; for subsidized enrollees, ACTUAL net rate hikes will likely be MUCH HIGHER for most enrollees due to the expiration of the improved ACA subsidies & the Trump CMS "Affordability & Integrity" rule changes.

UPDATE 8/14/25: I've revised my estimate of the total market size down to ~80,000, which results in a slight bump in the weighted overall average to 22.4%.

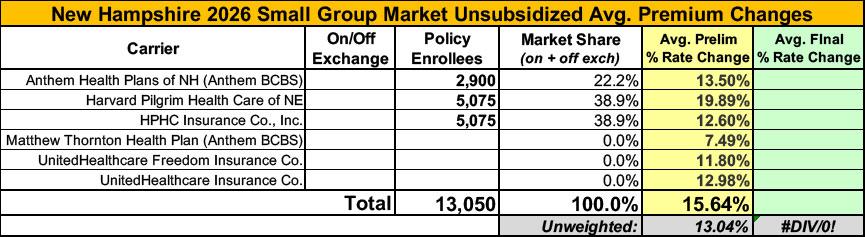

Meanwhile, I have no enrollment data at all for half of the small group carriers; the unweighted average 2026 rate hike there is around 13.0%.

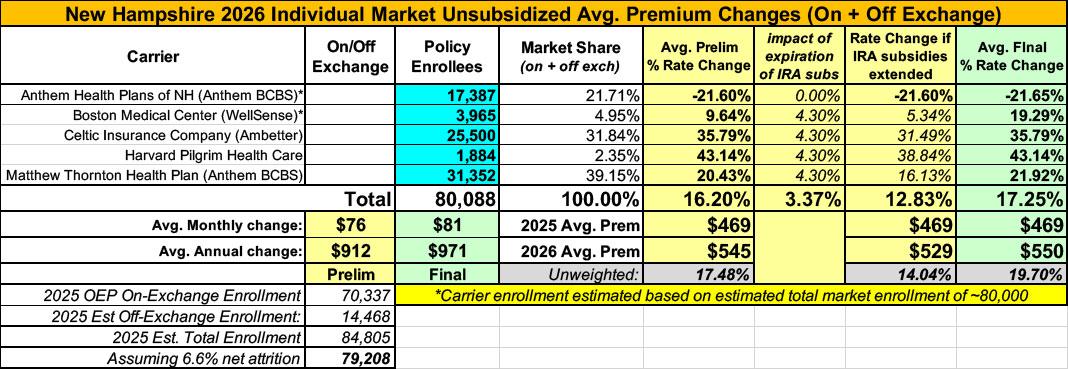

UPDATE 11/01/25: Just hours before the launch of the Open Enrollment Period, the final/approved filings were published at the federal rate review database.

The good news (such as it is) is that even though four of the five carriers had their rates approved pretty much as is and the fifth one saw a dramatic increase in their average rate change (Boston Medical Center went from 9.6% to 19.3%), the weighted average actually dropped several points from my preliminary estimate because it seems some of my enrollment estimates were off by a wide margin.

In the end, the weighted average increase for New Hampshire comes in at 17.3%:

| Attachment | Size |

|---|---|

| 41.54 KB | |

| 301.98 KB | |

| 496.2 KB | |

| 24.45 KB | |

| 167.9 KB | |

| 112.45 KB |

Advertisement