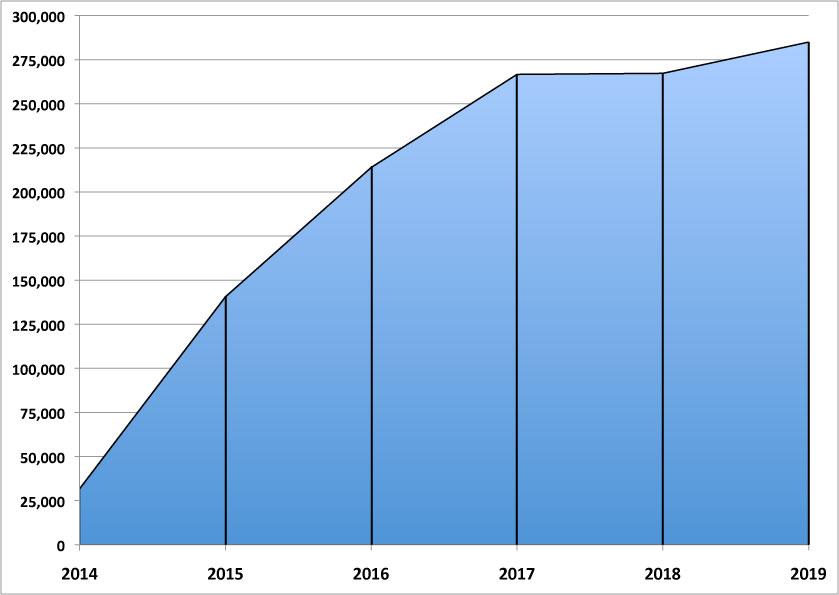

Once again: Massachusetts has managed to outperform their ACA enrollment numbers every year for five years running:

2014: 31,695 (major technical problems)

2015: 140,540 (complete platform overhaul)

2016: 213,883

2017: 266,664

2018: 267,260

2019: 284,969 and counting...

Just as impressive, if not more so: 97.2% of Massachusetts ACA enrollees have already paid their first monthly premium, which is well above the ~90% national average.

Last chance: MNsure Open Enrollment Period Ends this Sunday, January 13

January 10, 2019

ST. PAUL, Minn.—Minnesotans have until midnight on Sunday, January 13, to secure health insurance coverage through MNsure for 2019. Those who enroll by the deadline will have coverage that begins February 1.

"MNsure is the only place to get financial help to save money on your monthly premium," said MNsure CEO Nate Clark. "More than half of all MNsure enrollees are receiving tax credits."

Minnesotans can see if they qualify for financial help, while also comparing medical plans side by side, by using MNsure's plan comparison tool.

MNsure has extended Contact Center hours in the days leading up to the final deadline:

Rural Counties Lead Connect for Health Colorado® 2019 Health Coverage Sign Ups; Many Have Already Passed 2018 Totals

DENVER – Rural counties are leading the way in Connect for Health Colorado® sign ups as the state health insurance marketplace heads to the last week of the 2019 Open Enrollment period.

Overall, 2019 health plan selections through Connect for Health Colorado are running about 3 percent ahead of the comparable period a year ago but many rural counties have already exceeded the number of plan selections made in the entire two-and-a-half-month Open Enrollment period in 2018.

By January 3, 2019, 30 of the state’s 64 counties had matched or exceeded the number of plan selections made during all of last year’s Open Enrollment.This year’s Open Enrollment runs through January 15.

When I last checked on Access Health CT, Connecticut's ACA exchange, their 2019 Open Enrollment Period tally was about 10% short of their final number from 2018, by around 11,700 people. However, they still had a solid month left to make up the gap, with the enrollment deadline extended out until January 15th, 2019.

CT still has another week to go, but I just received a partial update, as of January 4th.

That's a net increase of 6,286 QHP selections between 12/15/18 - 1/04/19, or around 300 per day on average. At that rate, they'd add around 3,300 more by the final 1/15 deadline, putting them 112,000...still around 2,100 shy of last year. On the other hand, that timeframe included both Christmas and New Year's Eve, when enrollment tends to drop through the floor, so there's still a chance of Access Health CT at least matching 2018, though exceeding the 114,134 tally would be a pretty tall order at this point.

OK, with the FINAL HC.gov Report having been released, I can now fill in even more blanks in the 2019 Open Enrollment Period: A grand total of 11.24 million11.3 million QHP selections nationally so far. That includes 8.41 million on the federal exchange, plus another 2.82 million2.9 million on the 12 state-based exchanges.

If the counting were to stop right here, the total would be 3.9% 3.8% lower than last year nationally, which would actually be pretty good all things considered.

HOWEVER, it isn't over yet. Deadlines in several state-based exchanges haven't expired yet. New York and DC are open for business until January 31st, and many people in Alaska, Georgia and Florida still have time to enroll due to last fall's earthquake and hurricanes.

Press Release: NY State of Health Announces Qualified Health Plan Enrollment Tops January 31, 2018 Level

Jan 4, 2019

Still Time to Enroll

Consumer Demand for Affordable Coverage is High

ALBANY, N.Y. (January 4, 2019) - NY State of Health, New York’s official health plan Marketplace, today announced that as of January 1, 2019 more than 254,000 New Yorkers have enrolled in a Qualified Health Plan (QHP). With less than one month to go in the 2019 Open Enrollment Period, the number of QHP enrollees has already exceeded QHP enrollment at the end of the 2018 Open Enrollment Period.

So, it's over, right? Well...not quite. The 2019 ACA Open Enrollment Period officially ended last night...but only in 43 states. In the remaining seven (+DC), Open Enrollment hasn't ended yet. 2019 ACA Open Enrollment is still ongoing for nearly 10% of the population!

In Massachusetts, open enrollment runs through Jan. 23rd, 2019 for coverage starting February 1st

In the District of Columbia and New York, open enrollment runs through Jan. 31st for coverage starting March 1st

It's been pretty obvious for the past two years that the states which fully control their own ACA exchanges (including their own marketing and outreach budgets and their own exchange website platform) seem to be outperforming the states hosted by the federal exchange, HealthCare.Gov, in terms of open enrollment numbers year after year.

However, this can be a bit tricky to compare because some of the states have shifted back and forth...four states which ran their own platform for the first one to three years (Hawaii, Kentucky, Nevada and Oregon) moved home to the mothership in later years, while one state (Idaho) did the reverse--they stuck with HC.gov for 2014 but then broke off onto their own platform after that.

Yeesh...when it rains, it pours! Right on top of updated and/or final 2019 Open Enrollment numbers 41 states (Idaho, Rhode Island and the 39 states hosted by HealthCare.Gov) comes yet another updated tally from Massachusetts:

As of today:

274,317 enrollments for January

2,997 enrollments for February or March

3,763 plans selected (1st premium not paid but not due yet)

281,077 total

Retention rate is 91 percent, up 2.6 percent from last year.

The total is only 252 higher than their last update as of December 17th, but that's not surprising considering that we had both Christmas and New Year's in between. Again, MA has managed to improve their enrollment number every year for 5 years straight, an impressive feat indeed!

Again, Massachusetts' total from last year was 267,260 QHP selections, which means they're now 5.2% ahead of last year's final number...with 3 weeks left to go!