The other shoe to drop: How many enrollees were forced to "buy down" to a worse plan with higher out of pocket costs?

Thu, 02/05/2026 - 1:03pm

Back in December, I issued a strong warning that the official 2026 ACA Open Enrollment Period data would have to be taken with a huge grain of salt, since the actual effectuated enrollment data would likely take much longer to know:

...I'm bringing all of this back up again today because I strongly suspect that the situation is about to reverse itself, with the Trump Administration already preparing to brag about impressive-sounding ACA enrollment numbers for 2026 in spite of the enhanced tax credits expiring less than 60 hours from now...even though the actual negative impact of the expiring tax credits (along with several other administrative policy changes made by CMS this year) likely won't be known for several months after Open Enrollment officially ends in January.

...I honestly don't know exactly what it will look like. The main point to keep in mind is that CMS is unlikely to actually publish that data until sometime in July 2026 if at all, so any crowing by the Trump Administration, Congressional Republicans or their allies about the tax credits expiring having a "minimal impact" etc. should be taken with a massive grain of salt until then.

Sure enough, just 3 weeks later, the Wall St. Journal editorial board did exactly what I was afraid of: They published a bullshit piece falsely claiming that 2026 ACA enrollment had dropped off by far less than the Congressional Budget Office projected even though a) we won't know that for sure for months and b) the data on hand, when compared against earlier years with similar circumstances, strongly suggests that the drop-off in enrollment will actually be pretty close to what the CBO experts predicted (and potentially even worse).

Today I'm happy to report that numerous higher profile healthcare news platforms have taken my warning to heart. For instance, here's a CNBC article from yesterday:

The public will get a clearer picture of how many people dropped their ACA marketplace coverage and the demographics of those individuals when data becomes available over the summer, Wager said.

Even better, here's KFF with a piece focusing specifically on...pretty much every point I was making back in December:

2026 marks the first year since 2020 that enrollees in the Affordable Care Act Marketplaces do not have access to enhanced premium tax credits. The effect of the expiration on how many people will use ACA Marketplace coverage remains unclear.

New data released by CMS on plan selections show that ACA sign-ups for 2026 are down by over 1 million people compared to the same time last year, marking the first year since 2020 that sign-ups appear to have declined. A more detailed Health Insurance Exchanges Open Enrollment Report is expected in March or April that will detail demographics, income, and metal levels for people who select or are automatically renewed into a plan. Plan selection data is unable to fully capture the effects of the enhanced tax credits expiring on the number of people with coverage. As people fail to make their premium payments, actual enrollment—known as “effectuated” enrollment—will inevitably decline. With the expiration of enhanced premium tax credits, premium payments are estimated to have increased 114%, on average, for subsidized enrollees who stay in the same plan. With such steep increases, it is not yet clear how many people who have selected a plan during Open Enrollment will make a payment.

This brief explains the limitations of early data in understanding the impact of the expiration of enhanced premiums tax credit on ACA enrollment. It also provides a timeline of when more complete data will become available. The bottom line is that it will be quite a while before we get a complete picture of how much enrollment has dropped following expiration of the enhanced premium tax credits.

While I'm glad to see this point breaking through to the mainstream, it's still only half the story. The other half is the issue of those people who did enroll in 2026 ACA exchange coverage "Buying Down" (aka downgrading their healthcare plan to a worse one with higher out of pocket costs, worse provider networks, etc.) in order to mitigate the massive premium increases caused by the expired tax credits.

I wrote an in depth look at my own family's situation on this topic back in November. The short version is that we ended up having to downgrade from a Silver PPO to a Bronze HMO. This ultimately ended up keeping our premiums from skyrocketing over 33% higher (ouch!)...at the expense of seeing our deductible (which we're guranateed to max out due to an insanely expensive prescription medication my wife requires) go up 150% instead.

The end result is that our overall healthcare expenses are still going to be a whopping $15,000 higher this year than they were last year even though our premiums are essentially identical.

What about everyone else, though?

About a month ago I posted another warning about not being misled by initial 2026 Open Enrollment data. This time I mainly focused on the "average premium increases" which I warned will likely appear to be considerably lower than KFF's prediction of 114% net hikes on average for three pretty obvious reasons...the first of which is the "buying down" trend:

1. Millions of existing enrollees downgraded their plans to try & avoid at least some of the net premium hikes

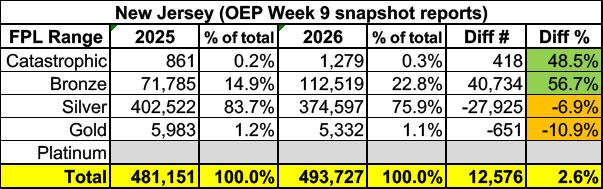

There's already hard evidence of this from Get Covered NJ, the New Jersey exchange,...

...Millions of other enrollees will still see their net premiums go up even if they downgrade their policies...it's just that it might be, say, a 40% increase instead of 200% or whatever.

Unfortunately, data on the types of plans people selected (primarily by Metal Level and Cost Sharing Reduction (CSR) plan status) won't be publicly available for most states until the 2026 Marketplace Open Enrollment Period Public Use Files are published, which likely won't happen until sometime in April or early May.

Thankfully, some of the state-based ACA exchanges do publish this type of demographic data far earlier than CMS's more comprehensive national report. In addition to New Jersey, there are four other state-based exchanges (so far) which have posted enough hard Metal Level enrollment data for me to run a year over year comparison:

Before I continue, it's vitally important to keep in mind that four of these states are providing supplemental state-based premium subsidies which cancel out either some or all of the lost federal tax credits for some (or all, in the case of New Mexico) of their enrollees...and the fifth state (Minnesota) has a special Basic Health Plan (BHP) program which covers residents earning less than 200% of the Federal Poverty Level (FPL), which makes up a whopping 65% of all ACA exchange enrollees nationally.

In other words, these states are not remotely representative of what either the effectuated enrollment dropoff or the "buying down" pattern looks like nationally. Unfortunately, this is all I have to work with for the moment, so it will have to do for now.

Remember, officially, Bronze plans cover ~60% of average medical expenses in aggregate; Silver plans cover ~70%; Gold plans cover ~80% and Platinum plans cover ~90%.

It's also important to keep in mind that last year around 68% of the Silver plan enrollees in these 5 states also received CSR assistance last year (nationally it was around 90%). I don't have the CSR breakout for 2026 for any of them yet, unfortuantely.

With all of this in mind, here's a summary of the year over year metal level enrollment for each, followed by all five combined.

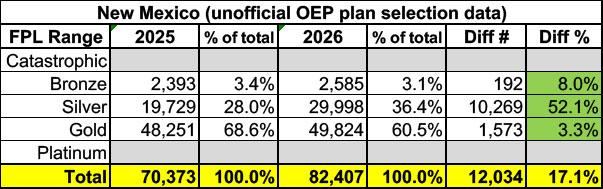

- Catastrophic plans weren't available in New Mexico in either year.

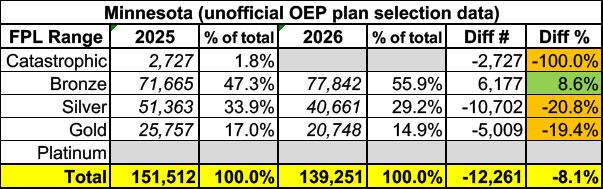

- Catastrophic plans were available in 2025 but aren't in 2026.

- Platinum plans weren't available in Minnesota, New Jersey or New Mexico either year.

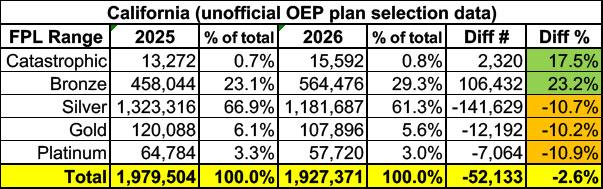

California, with the largest total population and having the largest state-based ACA exchange saw dramatic "buying down" even with the expired tax credits being fully backfilled for all enrollees earning less than 150% FPL (around 15% of all enrollees).

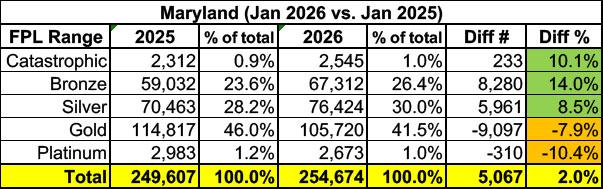

Maryland saw fariiy modest "buying down" this year, likely due in large part to them backfilling 100% of lost tax credits for enrollees earning up to 200% FPL (~32% of all enrollees) and 50% of it for enrollees earning 200 - 400% FPL (another ~33% of all enrollees).

Minnesota saw massive "buying down" from Gold and Silver to Bronze (presumably mitigated somewhat by Catastrophic plans having little choice but to move to Bronze due to Catastrophic plans not being available this year).

New Jersey also saw significant "buying down." While they do have state-based subsidies in place, those haven't changed since last year.

Finally, New Mexico saw enrollment increases at all metal levels thanks to the state fully covering the lost federal tax credits for every enrollee (in addition to their existing state subsidy program, I should note)!

When you combine all five states, this is what it looks like:

- Platinum plan enrollment has dropped nearly 11%

- Gold plan enrollment has dropped 8.1%

- Silver plan enrollment has dropped 8.8%

Silver/Gold/Platinum plans are down a combined 8.7%, while Bronze and Catastrophic plan enrollment are up a combined 23.8%.

Put another way, that's 197,000 fewer people with low-deductible plans and 162,000 more people with high-deductible plans.

And again, keep in mind that these are all states with various levels of additional financial support for enrollees. I can't begin to fathom what it's gonna look like in states like, say, Oklahoma, Tennessee or Indiana which don't have any such mitigating circumstances.

We'll find out (hopefully) later this spring...

Advertisement