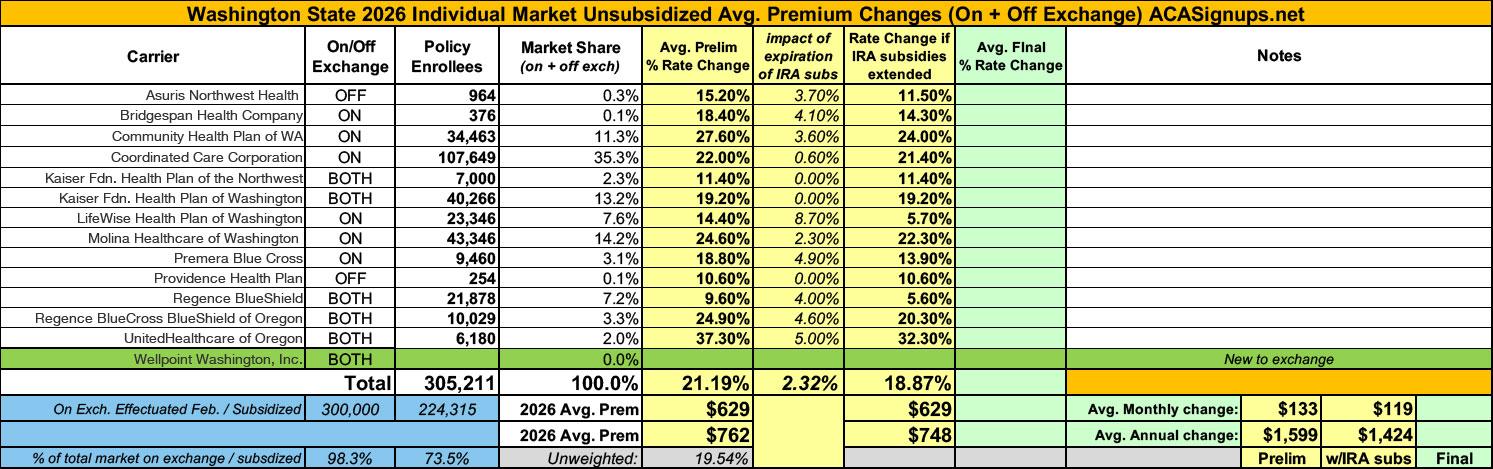

2026 Rate Changes - Washington: +21.2% avg; 2.3% due specifically to IRA subsidy expiration (preliminary)

Wed, 05/28/2025 - 11:17am

via the Office of the Washington Insurance Commissioner:

OLYMPIA, Wash. — Fourteen health insurers have requested an average rate change of 21.2% for Washington state's 2026 Individual Health Insurance Market. Insurers base their requested rate changes on assumptions they make about the services their policyholders will use and the cost to deliver that care. The health plans and proposed rate changes are currently under review by the Office of the Insurance Commissioner.

Wellpoint Washington, Inc. is new to the market and plans to sell in Grays Harbor, King and Spokane counties.

A factor impacting the requested increase this year is that the Enhanced Advance Premium Tax Credits are set to expire on Dec. 31, 2025, unless Congress renews them. While the premium subsidies provided under the Affordable Care Act help many people qualify for coverage, a significant number of people still struggle to afford coverage. Enhanced tax credits were created under the American Rescue Plan Act in 2021, and extended through 2025 by the Inflation Reduction Act, to help people who make more than 400% of the Federal Poverty Level ($62,600) afford coverage and increase the amount of help for people who make less than that.

According to the Washington Health Benefit Exchange, as many as 80,000 people will drop coverage if the subsidies are not extended. Health plans took this into account when creating their request for 2026. Based on the assumptions in the initial requested rate changes, renewing the tax credits could reduce the proposed rate changes by as much as 6.4%. Washington state Insurance Commissioner Patty Kuderer advocated for an extension of these tax credits while in Washington, D.C. earlier this month for the National Association of Insurance Commissioners (NAIC) 2025 Commissioner Fly-In.

"These tax credits are how many people afford critical coverage that protects themselves and their families," said Kuderer. "I know many members of Congress understand this and hopefully, they will prevail in these negotiations. Thousands of people in Washington state and millions across the country depend on the individual market and can't afford to see prices rise unnecessarily."

Most people get health coverage through their jobs, but more than 300,000 people in Washington do not have employer-sponsored health insurance and must buy a plan in the individual market. Last year, 286,526 people bought through the Exchange and 77% qualified for either federal premium tax credits or state-funded Cascade Care Savings.

- Asuris Northwest Health

Asuris only sells individual market plans off-exchange. This means none of their enrollees received any ACA premium subsidies at all, so you may not think that the expiration of the enhanced ARPA/IRA subsidies would impact their costs. However, it's more complicated than that: Any disruption which significantly impacts other carriers in the market will also have a ripple effect on Asuris as well, since many of those who drop coverage from one carrier will then shop around for another, which will in turn impact that carrier's morbidity...as well as Risk Adjustment payments/transfers.

The purpose of this memorandum is to identify the key assumptions and material factors that differ from the default set of rates should Congress extend the Expanded Premium Tax Credits guaranteed under the American Rescue Plan Act (ARPA) and the Inflation Reduction Act (IRA).

If Congress extends the EPTC as currently constituted through 2026, Asuris Northwest Health (ANH) expects the following interrelated assumptions to be impacted:

- Increase to market and carrier projected enrollment

- Decrease to market and carrier projected morbidity

- Decrease to the statewide average premium

- Smaller absolute value of transfer payment (reflecting the reduction to statewide average premium)

ANH’s default rates assume that individuals no longer eligible for PTC, or who will receive less PTC, will drop out of Washington’s individual market more readily than individuals with current or long-term health issues. The default rates assume a 4% increase to market morbidity. This increases the statewide average premium by a similar amount, which magnifies the anticipated transfer payment/receivable.

ANH’s morbidity model is not sensitive to the total projected market membership, nor to the mix of EPTC membership among metal levels. While these underlying assumptions may change as a result of EPTC extension, their impact is muted by offsetting effects.

If EPTC as currently constituted is extended through 2026, ANH’s 2026 rates would decrease by 3.7%.

There's a table below this which boils it down to the following: If the IRA subsidies are extended, Asuris would seek an 11.5% avg. rate hike; with the IRA subsidies expiring, it's 15.2%.

Most of the relevant section of BridgeSpan's memo is worded identically to Asuris', except for the actual impact:

If EPTC as currently constituted is extended through 2026, BHC’s 2026 rates would decrease by 4.1%.

If IRA subsidies are extended, BridgeSpan would ask for a 14.3% hike; if they expire, it's 18.4%.

CHP's actuarial memo is worded differently than the two above, but they still make it clear that the expiring IRA subsidies make up a chunk of the rate hikes:

Table 2.1 below describes and quantifies the primary drivers underlying the proposed rate change for 2026, including but not limited to, the estimated impact of enhanced premium tax credit subsidy expiration. This breakdown is intended only for explanatory purposes and is distinct from the development of rates, as described in the subsequent sections of this memorandum.

- Estimated Changes in Experience: 1.068

- Additional Year of Trend (2025 to 2026): 1.053

- Impact of eAPTC Subsidy Expiration: 1.036

- Changes in Net Morbidity and Risk Adjustment (Excluding eAPTC Subsidy Expiration Impact): 1.088

- Changes in Benefits: 0.997

- Changes in Plan Mix and CSR Rate Load: 1.034

- Changes in Administrative Costs: 0.989

We modeled adjustments to CHPW's projected claims and risk adjustment transfer position to account for the anticipated impact of enhanced premium tax credit subsidy expiration. This impact reflects some assumed level of deterioration in the single risk pool due to anticipated disenrollment in 2026.

If I'm reading this correctly, it looks like CHPs rate hike would be 3.6 points lower if IRA subsidies are extended, or 24.0% instead of 27.6%.

To account for eAPTC expiration prior to the 2026 benefit year, we have assumed rates will increase due to anticipated reductions in enrollment, both at the issuer and single risk pool level. As eAPTCs expire and enrollees subsequently face increased out-of-pocket premiums, we assume healthier individuals who tend to be more price sensitive will leave the market, worsening the average morbidity of the individual risk pool.

...The proposed rate increase of 22.0% reflected in this memorandum assumes that 1. eAPTCs expire at the end of 2025, and 2. CMS’ Marketplace Integrity and Affordability rule, as published in the Federal Register on March 19, 2025, is finalized as proposed.

Both policy changes are expected to materially affect projected enrollment and morbidity for plan year 2026 at the issuer and single risk pool level. Most notably, as eAPTCs expire and enrollees face increased out-of-pocket premiums, we assume healthier individuals who tend to be more price sensitive will exit the market, worsening the average morbidity of the individual risk pool. Shifts in statewide average morbidity, including both above policy changes, are expected to increase the Index Rate by 1.0% between the base and projection period.

Under an alternate scenario where eAPTCs are funded for plan year 2026 and CMS’ proposed rule is implemented without modifications, shifts in statewide average morbidity is expected to increase the Index Rate by -0.7% between the base and projection period. Key provisions included in the proposed rule related to open enrollment, special enrollment periods and annual eligibility redeterminations (e.g. requiring $5 premium obligation for auto re-enrollees) are still expected to drive a meaningful decline in enrollment, particularly among healthier enrollees and adversely affect the average morbidity of the single risk pool.

The overall average rate change under this alternate scenario is 21.4%, compared to 22.0% in the baseline scenario reflected in this memorandum. The difference in average rate changes also reflects other varying assumptions between scenarios, such as CSR loading, administrative expenses, and other demographic factors.

Note that the requested rate change may not be the same across all plans within a product due to changes to the member cost sharing amounts by plan. Additionally, the defunding of CSR subsidies has contributed to the rate levels being higher than if the subsidies were to be funded.

CCC actually anticipates a pretty mild impact...just 0.6 points.

Kaiser, oddly, doesn't seem to anticipate any significant impact of the subsidies expiring at all...apparently due to changes in how Silver Loading works specifically in Washington State...I think:

The projected allocation of members by plan follows the emerging distribution of members for March 2025 with modifications to account for two new plans as well as implications of the increased CSR load and restrictions that will only allow 87% and 94% CSR members to enroll in Silver On-Exchange plans. Overall participation in the Individual market continues to be volatile, as price sensitivity and the weakening of the Individual Mandate continue to cause member movement between carriers as well as an overall reduction in market participation. The expiration of ARPA subsidies is heavily offset by increases in the CSR load, so KFHP is not projecting any market contraction for 2026.

Even more confusingly, later in the same filing memo, it contradicts itself by saying that the filing assumes the subsidies will be extended...but still makes a reference to the "mandated CSR load:"

This rate filing assumes that the Individual Mandate will continue to be powerless with no replacement provision for the 2026 plan year. Additionally, this rate filing assumes that the additional premium subsidies of the American Rescue Plan Act (ARPA) will be renewed at the end of 2025 and continue through 2026 and Cost Share Reduction Subsidies will continue to be un-funded for the 2026 plan year, and additional plan paid claims costs will be applied only to the On-Exchange Silver tier plans. Whether or not the ARPA subsidies are renewed for 2026 KFHP assumes the impacts on the market will be the same. The mandated CSR Loads are expected to make up for the loss of ARPA subsidies in the case of expiration. If ARPA is extended KFHP is assuming that there are not enough un-insured lives available in the market to make a material increase the market size.

I'm not entirely sure what to make of this but it sounds like Kaiser NW doesn't expect any net impact either way.

This filing assumes that the enhanced premium tax credits that were extended by the Inflation Reduction Act will expire at the end of 2025. However, we have included no additional load in the morbidity assumptions in Worksheet 1. For plan year 2026, there is a mandated 43.5 percent silver load for on-exchange plans, significantly increasing the premium for the benchmark plan and thereby making bronze and gold plans more affordable for members receiving premium subsidies. Between the increased subsidies and the already low uninsured rate in Washington, our best estimate is that neither the population nor its average morbidity will change with the expiration of the enhanced premium tax credits.

OK, there it is: Similar to Kaiser NW, Kaiser of WA also thinks that the impact of expiration of the IRA subsidies will be cancelled out by the mandated Silver Switcharoo CSR rule implemented by the state insurance commissioner back in March:

The Office of the Insurance Commissioner (OIC) must review and approve all individual health plan rates prior to their use. This emergency rule adjusts health insurer rate development components for Plan Year 2026 to preserve consumer affordability and stability in Washington state’s individual health insurance market. It applies a uniform cost-sharing reduction silver load adjustment factor to rates for silver level qualified health plans (QHPs) sold on the Washington state Health Benefit Exchange. This emergency rule is necessary for the preservation of the public health, safety, or general welfare by keeping health insurance affordable for up to 80,000 individuals who are at risk of losing health insurance when the Enhanced Advance Premium Tax Credits (eAPTCs) expire on December 31, 2025.

...Under current federal law, eAPTCs will expire on December 31, 2025 absent congressional action, making them unavailable to consumers beginning on January 1, 2026, i.e., Plan Year 2026. The original APTCs are permanently authorized in federal law and would remain when eAPTCs expire; however, the original APTCs offer a lower level of premium subsidies than the eAPTCs. eAPTCs enhance affordability by lowering net premiums for households with income above 400% of FPL ($62,600 per year for an individual in 2025) and by increasing subsidy levels for people with income below 400% of FPL who were originally eligible for APTCs. The eAPTCs have particularly made health care more affordable for people ages 55 to 64 who face high health care costs but are not yet eligible for Medicare. For this population, HBE estimates that the eAPTCs have decreased annual net premium costs by $1,900. Under current state law, Cascade Care Savings are also set to expire on June 30, 2025, absent state legislative action to fund them for state fiscal years 2026 and 2027 [Engrossed Substitute Senate Bill 5950, Chapter 376, Laws of 2024; RCW 43.71.110].

...OIC is adjusting insurer rate development components in three ways:

1. Uniform CSR Silver Load Adjustment: Sets a uniform CSR silver load adjustment for the individual on-Exchange health plans.

2. Standardized Induced Demand Factors (IDFs): Sets induced demand factors for individual and small group market health plans.

3. Pricing Actuarial Value (AV) Guardrails: Establishes restrictions on AV pricing value to ±3% of the plan’s Federal AV metal value for individual and small group market health plans.

OIC expects these adjustments to lessen the negative impact of the eAPTC expiration. Overall, OIC expects these adjustments to result in a higher level of premium tax credits (APTCs), thereby reducing net premiums for HBE consumers enrolled in a silver plan and mitigating negative impacts on consumers who choose to enroll in non-silver plans. HBE consumers enrolled in a non-silver plan represent about half of all HBE enrollees, according to HBE data shared with OIC in 2024. OIC expects these changes to have the overall effect of keeping more enrollees covered by lessening the premium increases that consumers would otherwise experience in 2026. This in turn will result in better health outcomes for up to 80,000 Washingtonians, promote individual health insurance market stability, and reduce potential increased uncompensated care demands for health care facilities and providers.

I'm not sure how this CSR Silver Switcharoo rule escaped my attention before; I should have written a full blog post up about it. Regardless, this is a simple & clever way for Washington to mitigate the impact of the IRA subsidies expiring for most of their enrollees. Unfortunately it doesn't do anything to help those who earn more than 400% FPL, who won't be eligible for any federal subsidies at all.

With the expiration of the enhanced advanced premium tax credits in 2026 and the new uniform silver loading rule, we expect deterioration of our experience as heathy people exit the market or purchase less expensive plans. To determine this adjustment, LifeWise projected the contribution margin before and after these changes by looking at who would likely leave LifeWise or migrate to a different LifeWise plan. This change in contribution margin is then grossed up to an allowed basis and divided by the projected index rate to get the adjustment factor. The development of this adjustment of 1.087 is shown in Appendix 2.3d.

...LifeWise is proposing a one-time transitioning C&R charge of -2.7% to ease the impact on premium increase due to recent or expected rules changes. The negative C&R offsets the impact of the expected expiration of the enhanced advanced premium tax credit and the new rules around the development of the AV & Cost Sharing Adjustment. LifeWise is committed in the individual market and is willing to take a one-time hit to support the emergency rule with the uncertainty of how membership will react to the changes.

Sure enough, a table a few pages later puts the adjustment factor at 8.7 percentage points...or more than half the overall 14.4% rate hike being requested.

The rate methodology and resulting premiums outlined in this Actuarial Memorandum assume current law, which includes the following:

- The expiration of the American Rescue Plan (ARP) enhanced premium tax credit subsidies at the end of 2025.

- Cost-Sharing Reduction (CSR) subsidies remain unfunded.

- The parameters of the HHS Notice of Benefit and Payment Parameters for 2026 (Final 2026 Payment Notice), which became effective on January 15th, 2025.

Notably, the Marketplace Integrity and Affordability Proposed Rule (Program Integrity Rule) was published by CMS in the Federal Register on March 19th, 2025, followed by a comment period that could substantially alter the proposed rule. The rate methodology and resulting premiums outlined in this Actuarial Memorandum were prepared prior to the finalization of the Program Integrity Rule and therefore do not reflect the changes proposed in the Program Integrity Rule.

Molina will seek regulatory approval to file revised rates if material changes to the regulatory environment occur, including, but not limited to, changes to the above mentioned items.

...he acuity change from the 2025 current period to the 2026 projection period is calculated in the same way, weighting 2025 and 2026 risk scores with 2026 projected metal mix. With the implementation of uniform silver-loading, the majority of Molina’s Silver members are expected to move to Gold plans decreasing the projected average risk score for Gold members.

Under current law, Enhanced Premium Tax Credits (ePTCs) are scheduled to expire at the end of 2025. Molina retained Milliman to analyze the impact of expiring premium subsidies on statewide morbidity. We reviewed the study and determined that the best estimate for an acuity adjustment is 1.023. The total acuity adjustment factor for the 2025 current period to the 2026 projection period is 0.930.

...We are anticipating that Molina will not offer one of the lowest cost Silver plans in 2026, and as a result, will continue to decline in Silver membership. This is partially because new members tend to select one of the lowest cost offerings in the market, including Cascade Select plan offerings from other carriers. As a result, Molina modeled a reduction in the proportion of available Silver members in the market compared to current membership. With the anticipated expiration of ePTCs, Molina modeled a reduction in membership. These members may move to other carriers or leave the market.

It looks like Molina is baking in a 2.3 point hike due specifically to IRA subsidy expiration.

Premera is using an Other Adjustment factor of 1.237 for 2026.

This factor is a combination of 1) the projected paid to allowed vs AV & cost sharing adjustment and 2) the impact of the expiration of the enhanced advanced premium tax credits and the new rule on the silver CSR loading.

1) Due to the new Emergency rule from the OIC, the overall AV & Cost Sharing factor varies from the projected paid to allowed factor, and an adjustment factor is added. LifeWise calculated the actual projected paid to allowed ratio based on the experience period paid to allowed, adjusting for the projected change in benefits and cost sharing, then took the projected paid to allowed divided by the projected AV & Cost Share factor to determine the adjustment factor needed. The development of this adjustment of 1.180 is shown in Appendix 2.3a.

2) With the expiration of the enhanced advanced premium tax credits in 2026 and the new uniform silver loading rule, we expect deterioration of our experience as heathy people exit the market or purchase less expensive plans. To determine this adjustment, Premera projected the contribution margin before and after these changes by looking who would likely leave Premera or migrate to a different Premera plan. This change in contribution margin is then grossed up to an allowed basis and divided by the projected index rate to get the adjustment factor. The development of this adjustment of 1.049 is shown in Appendix 2.3b.

Premera is anticipating that about 4.9 points of their rate hike will be caused by IRA subsidies expiring.

Providence is another carrier only offering off-exchange plans, although in this case it sounds like they don't think it'll impact them to any significant degree:

We believe the premium rates filed are reasonable in relation to the benefits provided and are not excessive, inadequate, or unfairly discriminatory based on the provisions of the ACA as currently implemented; however, future modifications in legislation, regulation, and/or court decisions may affect the appropriateness of the premium rates. The values in this report, unless stated otherwise, reflect the scenario in which enhanced premium tax credits (ePTCs) expire at the end of calendar year 2025. No adjustments were made for other proposed regulation, including CSR appropriation. Wakely and PHP would like to reserve the right to change assumptions that become materially impacted due to a change in the regulatory environment up until filings are approved in order to ensure rates are as accurate as possible, to the extent the Washington OIC and federal rules allow.

...No additional morbidity adjustments were deemed necessary. Due to PHP’s unique population, the expiration of the enhanced premium tax credits (ePTC) at the end of 2025 is not expected to impact PHP’s enrollment or population morbidity. The statewide impact is accounted for within the risk adjustment buildup.

...For the primary filing, each of the statewide components was additionally adjusted for the projected impact of the expiration of ePTCs. Using public data sources, the Wakely claims ACA database, and 2024 WNRAR results provided by the client, Wakely estimated the impact of changes in member net premiums (defined as gross premiums net of advanced premium tax credits) by age bracket, plan metal/CSR tier, and income bracket as a percentage of the Federal Poverty Level (FPL) to determine the range of ACA individual market impacts in 2026 due to the expiration of ePTCs. For a consumer of a given age, plan metal/CSR tier, and income, the change in the net premium post-expiration of ePTC was combined with a price elasticity of demand for health insurance to estimate the proportion of members dropping coverage and the proportion of members switching to a less expensive plan metal tier (“buying down” or “buydown”). Adjustments were made to account for shifts in PLRS, AV, IDF, and the statewide average premium. The resulting adjustments were set to 1.000 for the secondary set of rates.

The purpose of this memorandum is to identify the key assumptions and material factors that differ from the default set of rates should Congress extend the Expanded Premium Tax Credits guaranteed under the American Rescue Plan Act (ARPA) and the Inflation Reduction Act (IRA).

If Congress extends the EPTC as currently constituted through 2026, Regence BlueShield (RBS) expects the following interrelated assumptions to be impacted:

- • Increase to market and carrier projected enrollment

- • Decrease to market and carrier projected morbidity

- • Decrease to the statewide average premium

- • Smaller absolute value of transfer payment (reflecting the reduction to statewide average premium)

RBS’s default rates assume that individuals no longer eligible for PTC, or who will receive less PTC, will drop out of Washington’s individual market more readily than individuals with current or long-term health issues. The default rates assume a 4% increase to market morbidity. This increases the statewide average premium by a similar amount, which magnifies the anticipated transfer payment/receivable.

RBS’s morbidity model is not sensitive to the total projected market membership, nor to the mix of EPTC membership among metal levels. While these underlying assumptions may change as a result of EPTC extension, their impact is muted by offsetting effects.

If EPTC as currently constituted is extended through 2026, RBS’s 2026 rates would decrease by 4%.

That's 5.6% vs. 9.6%.

Basically the same text as Regence BlueShield, except that Regence BCBS puts their IRA expiration impact at 4.6 points.

Expiration of Enhanced Subsidies and Other Regulatory Changes

An adjustment was applied to account for additional anticipated changes in morbidity due to the expiration of enhanced premium subsidies and other regulatory changes

...ARPA Expiration Morbidity Impact 1.050

That's a 5-point hike for IRA subsidy expiration.

Wellpoint is new to the Washington market, so there's no rate changes to speak of; I'm including their filing for completeness sake.

Plug them all into a spreadsheet and here's what it looks like...it ain't pretty no matter what:

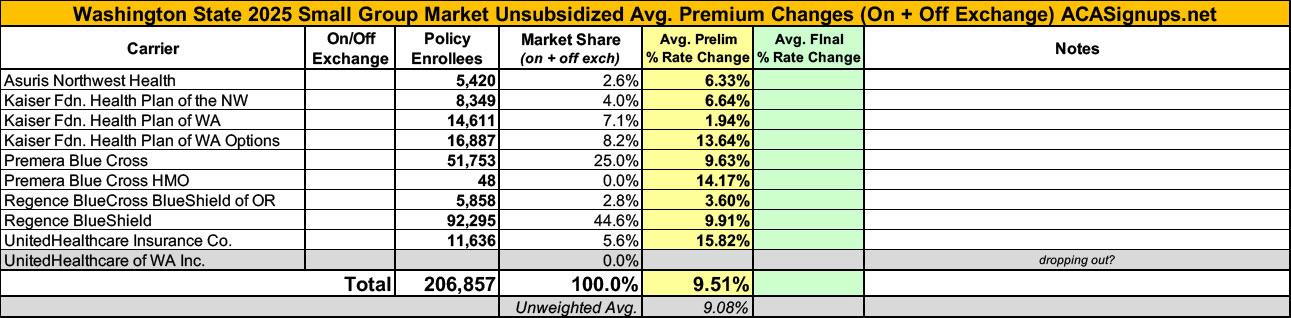

Meanwhile, Washington's small group market carriers are seeking an average rate increase of 9.5%:

| Attachment | Size |

|---|---|

| 9.81 MB | |

| 8.18 MB | |

| 4.7 MB | |

| 7.35 MB | |

| 6.78 MB | |

| 9.14 MB | |

| 15.32 MB | |

| 22.99 MB | |

| 14.11 MB | |

| 5.14 MB | |

| 11.4 MB | |

| 13.23 MB | |

| 9.08 MB | |

| 10.61 MB |

Advertisement