Once again: The true measure of ACA healthcare coverage enrollment isn't how many people select policies during the Open Enrollment Period, it's how many actually have those policies in effect (aka "effectuated enrollment")...as well as how comprehensive that coverage is, of course.

Yesterday, Pluribus News published a new story about effectuated enrollment across a dozen or so states (the reporters actually consulted with me several times about their data and how to present it, although I somehow didn't end up getting credited in the final version).

IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

I've written multiple times in the past about "Silver Loading," the ACA health insurance policy pricing strategy in which insurance carriers load the extra cost of their Cost Sharing Reduction financial burden (the portion of deductibles, co-pays & coinsurance which they're required to cover themselves for low-income enrollees who select Silver plans) onto the gross premium of those same Silver plans.

It gets a bit wonky, but the bottom line is that Silver Loading results in the gross price of Silver ACA plans increasing significantly even if the price of Bronze, Gold & Platinum plans only go up modestly. This may sound bad, but stay with me.

From the carriers perspective, how the CSR load is allocated doesn't matter much as long as they aren't left stuck with the bill...but pricing the plans in this fashion has major implications for the enrollees themselves.

As anyone not under a rock for the past few months knows by now, the improved federal Affordable Care Act tax credits which were put into place by President Biden and Congressional Democrats starting in 2021 are currently scheduled to expire at the end of December, just 2 1/2 months from now.

On top of this, the Trump Regime has also made administrative regulatory changes to how the ACA is structured resulting in the remaining tax credit formula becoming even less generous yet, while also eliminating eligibility for either financial assistance or even ACA enrollment whatsoever to many other Americans.

I still have the preliminary 2026 rate filings to analyze for about 10 more states, but I'm taking a break to go back and revisit ARKANSAS.

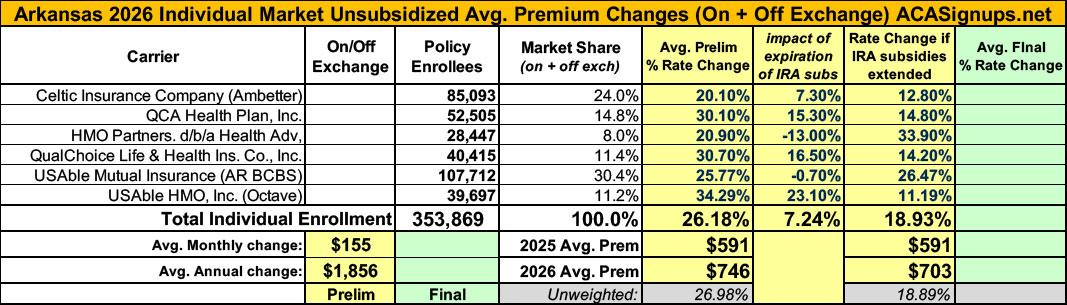

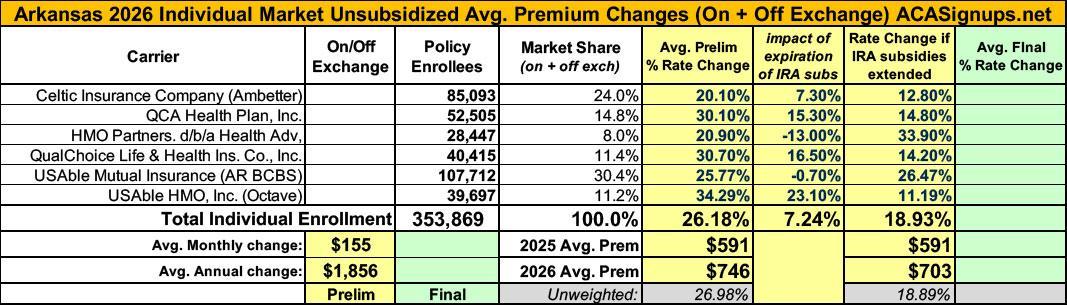

Back on July 18th, I posted my original analysis of ACA-compliant individual & small group market filings for Arkansas insurance carriers. At the time, I found that the weighted average increases being requested for individual market policies averaged a disturbingly high 26.2%. Here's what the breakout looked like:

Arkansas has around 166,000 residents enrolled in ACA exchange plans, 92% of whom are currently subsidized. I estimate they also have perhaps another ~11,000 unsubsidized off-exchange enrollees.

(sigh) OK, I'm not sure if we've reached the 5th or 6th chapter in this ongoing saga, but I hope it's the last one.

When we last left our story (just 5 days ago), I noted that both the current number of enrollees as well as the average rate increases for each of the carriers on the Arkansas individual market had jumped all over the place at least 4 times, and that while it's common for these numbers to change a bit here and there throughout the multi-month filing process, both the degree of some of the changes as well as the circumstances surrounding them were often far beyond what I've typically seen in over a decade of tracking this stuff:

Given all the confusing numbers I've posted before, I've boiled it all down to the simplified tables below which illustrate the mess:

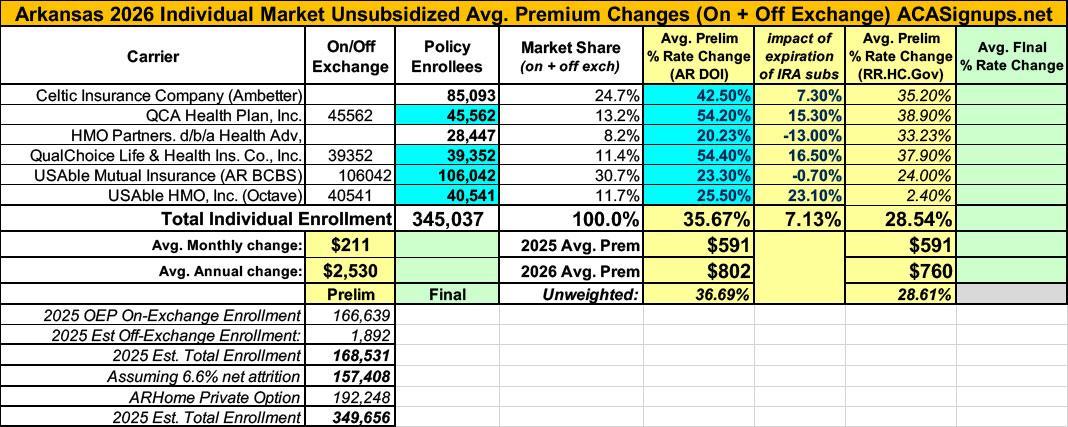

In the most recent chapter of the ongoing 2026 Arkansas rate filing saga, I noted that both the total number of residents enrolled in ACA individual market policies as well as the average 2026 rate increases for the six insurance carriers participating in the individual market next year kept changing, often in ways which were contradictory with other numbers claimed within the same press releases:

You'll notice that in addition to the rate changes being updated (increasing from a weighted average hike of 26.2% to 35.7%), most of the current enrollee figures were also modified, although these only changed slightly in most cases. Overall the total number of current individual market enrollees statewide dropped a bit from ~354,000 to ~345,000.

Minor changes like this aren't unusual; sometimes the carriers make slight tweaks as more recent data comes in or clerical errors are corrected; other times they round off the enrollee totals (that doesn't seem to be the case here, however).

Back in July I posted my analysis of the preliminary 2026 rate filings by the 6 Arkansas insurance carriers participating in the individual market. At the time, they looked like this: