2027 Rate Changes - Rhode Island: +20.1% indy, +8.7% sm. group, +15.5% lg. group (preliminary)

Sat, 06/20/2026 - 4:26pm

via the Rhode Island Insurance Commissioner:

2027 Requested Commercial Health Insurance Rates Have Been Submitted to OHIC for Review

The Office of Health Insurance Commissioner (OHIC) today released the individual, small group, and large group market premium rates requested by Rhode Island’s insurers. The requests were filed as part of OHIC’s rate review process (for coverage effective on or after January 1, 2027).

“Health insurers are once again seeking rate increases to cover the rising cost of health care and other expenses,” said Health Insurance Commissioner Cory King. He continued: “OHIC will thoroughly review these requests to determine whether they are justified.”

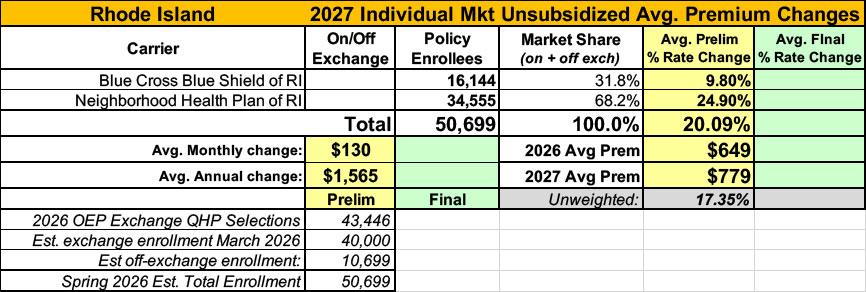

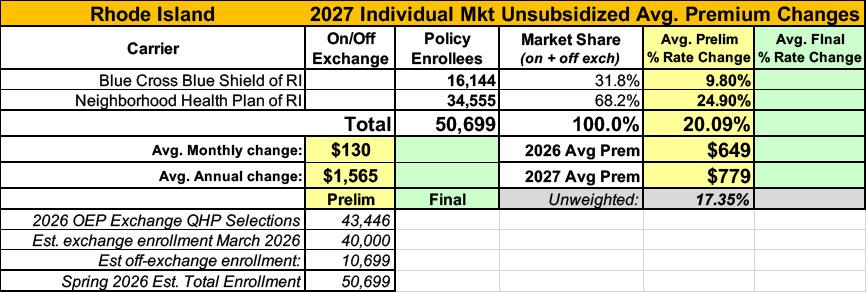

Two insurers, Blue Cross Blue Shield of Rhode Island (BCBSRI) and Neighborhood Health Plan of Rhode Island (NHPRI), filed rates for plans to be sold on the individual market to people and families who do not receive insurance through their employer.

In the individual market requested average rate increases for 2027 coverage range from 9.8% for BCBSRI to 24.9% for NHPRI. The weighted average increase of individual market requests for 2027 is 20.1%, compared to requested increase of 23.8% for 2026 coverage. Last year, OHIC approved an average individual market rate increase of 21.0% for 2026 coverage.

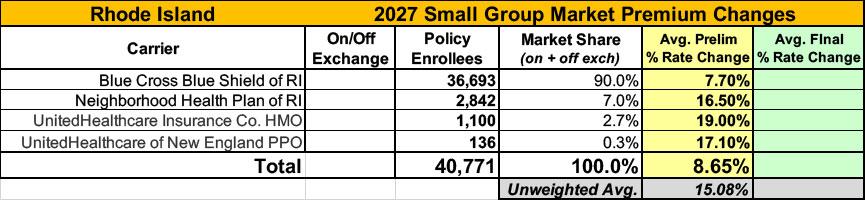

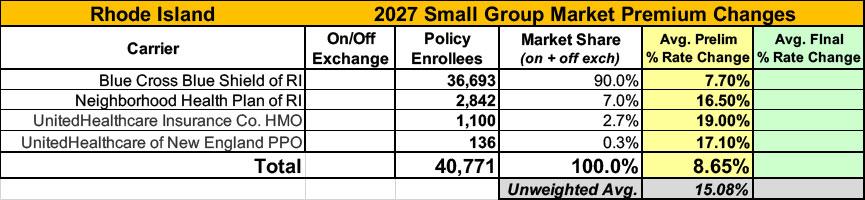

In the small group market, insurers requested average increases for 2027 ranging from 7.7% to 19.0%. The weighted average increase of small group market requests for 2027 is 8.7%, compared to the average requested increase of 22.0% for 2026 coverage. Last year, OHIC approved an average small group market rate increase of 17.6% for 2026 coverage.

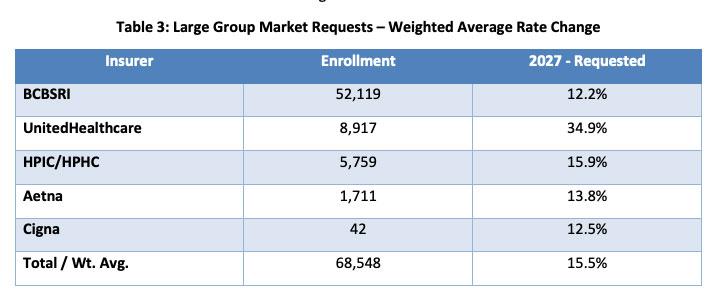

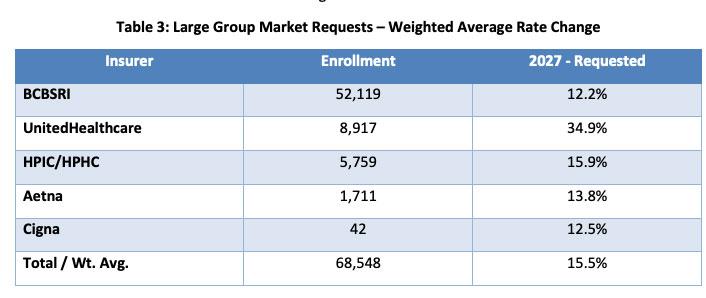

Five insurers – BCBSRI, UnitedHealthcare, Harvard Pilgrim Health Care of New England, Inc (HPHC)/HPHC Insurance Company (HPIC), Aetna, and Cigna – filed large group rates. Large group market requested average rate increases for 2027 range from 12.2% to 34.9%. The weighted average increase of large group market requests in 2027 is 15.5%, compared to the average requested increase of 24.1% for 2026 coverage. Last year, OHIC approved an average large group market rate increase of 19.3% for 2026 coverage.

OHIC will review all data, pricing assumptions, administrative charges, and other information to assess the reasonability of the premium requests by each insurer. The Commissioner may approve as filed, modify, or reject an insurer’s rate filing in accordance with powers vested in the Office by the Rhode Island General Laws. Approval decisions on rates are based on data, actuarial analysis, and the requirements of Rhode Island law.

The proposed rate increases do not apply to self-funded employer groups that account for approximately 65% of Rhode Islanders with employer-sponsored coverage. Self-funded employers pay the health care expenses of their employees and dependents directly, commonly relying on health insurance companies for administrative services, such as member enrollment, provider contracting, and claims processing.

OHIC will also review each health insurer’s coverage and benefit contracts with consumers to ensure that plans sold in Rhode Island meet all benefit, access, and member cost sharing standards required by state and federal law. OHIC’s final decision to approve, modify, or reject the proposed rates is expected in mid-September.

This year the individual market rates filed by NHPRI will be considered as part of an administrative hearing process. The hearing is scheduled for the following dates:

- NHPRI Hearing: July 14th and July 15th.

Additional details on the rate hearing can be found in the Public Comment Solicitation. OHIC will accept written public comments on the proposed rates through Friday July 24, 2026. Comments may be submitted in writing via email to OHIC.HealthInsInq@ohic.ri.gov.

Blue Cross Blue Shield of RI:

Blue Cross & Blue Shield of Rhode Island (“BCBSRI”) has submitted its annual rate filing for the individual market. This document gives an overview of that filing.

Scope and Range of the Rate Increase:

BCBSRI has calculated the weighted average rate increase for BCBSRI plans, before reflecting changes due to age, as 9.8%.

The range of rate increases for BCBSRI plans, before reflecting changes due to age, which consumers will experience is: 6.9% to 31.0%.

The actual increase for an individual now enrolled will vary based upon:

- the age of each person enrolled;

- the plan chosen; and

- if the person is eligible for federal subsidies.

This filing impacts about 16,138 individuals now enrolled with BCBSRI and new customers joining after January 1, 2027. These individuals are enrolled either:

- directly with BCBSRI; or

- through Rhode Island’s health insurance marketplace (HealthSource RI).

The rate increase will take effect January 1, 2027. Rates will stay in effect until December 31, 2027.

Key Drivers for this Filing:

The rate increase for 2027 is due in large part to the continuing increase in the total cost of health care in Rhode Island.

Significant inflation in the cost of goods and services in all sectors of the economy has had a profound impact on the cost of medical services, and BCBSRI expects to see substantial increases in provider unit costs for 2027. Specialty drug treatments also account for a large part of the increase in medical costs. Additionally, increases in how often and how much health care is received are driving an increase in rates for 2027. Required increases in primary care provider payments are also contributing to the rate increase.

Administrative costs factor into this filing as well. These include state and federal taxes, such as the state premium tax, and a state fee used to fund HealthSource RI. The state fee used to fund HealthSource RI adds 1.6% to the rate.

This filing reflects a projected medical loss ratio (“MLR”) of 86.0% using the federal formula. The MLR is the percent of each premium dollar that we spend to pay for healthcare services and activities that improve the quality of care of our members. The federal government requires an MLR of 80% or higher in the individual market.

Changes in Benefits:

At the same time as this filing, BCBSRI submitted our 2027 health plans to the Office of the Health Insurance Commissioner for approval. The plan filing includes benefit changes consistent with state and federal regulations, including changes to:

- cost sharing amounts; and

- annual out of pocket maximums.

These benefit changes will take effect on January 1, 2027.

Neighborhood Health Plan:

Neighborhood Health Plan of Rhode Island’s (Neighborhood) mission is to be an innovative health insurance company that, in partnership with Rhode Island’s Community Health Centers, secures access to high quality, cost-effective health care for Rhode Island’s at-risk populations. In service of this mission, Neighborhood has submitted its annual rate filing for the individual market. An overview of the filing is described below.

Scope and range of increase:

Weighted Average Rate Increase: This represents the average rate increase, including modifications to prior year benefits and other pricing adjustments. The average premium increase to consumers, before reflecting changes in age, is expected to be 24.9%.

The range of rate changes, before reflecting changes in age, which consumers will experience, is approximately 17.9% to 29.3%.

The key drivers of this rate change, further described below, are an increase in medical services costs driven by required hospital rate increases tied to inflation and pharmacy costs, as well as an increase from anticipated growth in risk adjustment transfers. There is uncertainty in impacts of inflation beyond the hospital rate increase (particularly due to expanded primary care coverage mandates), uncertainty in market size due to Medicaid eligibility requirements, and significant high costs for new drugs coming on the market. Neighborhood’s financial health is a key component in being able to continue to offer the lowest priced products in the Marketplace.

Financial experience of product:

In January 2014, Neighborhood for the first time offered individual insurance coverage through HealthSource RI (HSRI). Stable membership from 2015 through 2025 has allowed Neighborhood to develop rates based on actual experience. Neighborhood retained actuarial expertise who utilized models along with Neighborhood’s commercial market experience to prepare the premium rates for individual market plans to be offered on HSRI and directly with Neighborhood in 2027.

Reserves have been established that allow Neighborhood to continue serving our members and maintain financial stability. Since Neighborhood first started offering products on HSRI in calendar year 2014,

Neighborhood’s commercial reserves have contributed to total reserves on average by 7% annually. Neighborhood will continue to grow our reserves by including a 7.0% contribution in this filing.

Changes in Benefits:

Neighborhood has updated the benefit packages in 2027 to comply with federal Actuarial Value (AV) requirements. These benefit changes impacted the rate change by approximately -2.0%, which reduced the overall rate increase.

Changes in Medical Service costs:

A main driver of premium increases includes a higher percentage of members electing bronze level plans in 2026 that is anticipated to be sustained in 2027, increasing medical costs on paid claims for our members resulting in an approximate 8.9% medical/prescription drug annual trend assumption. Components of this trend also include increases in unit costs of medical services due to inflation, increased medical utilization, primary care coverage mandates, increases in specialty drug expenses, technology advances in medicine, equipment and drugs, changes in network provider contracts, and other factors. To ensure members are getting the best high quality, cost-effective health care, Neighborhood regularly reviews medical expenses to find innovative ways to decrease medical costs for our members.

Administrative costs and anticipated profits:

Neighborhood is committed to high quality, cost-effective health care which involves managing administrative costs by increasing operating efficiencies and reducing unnecessary expenditures.

Administrative cost changes resulted in a negligible increase to average premium. This does not include taxes and fees.

Neighborhood anticipates that 87.3% of premium dollars (net of taxes and fees) will go towards medical expenses. This is an estimate that will be subject to change based on medical trends and other adjustments under federal regulations as well as emerging experience. Federal requirements under the ACA state at least 80% of premium dollars need to be utilized for medical expenses. If less than 80% of premium dollars go towards medical expenses under the federal requirement, members will receive a premium rebate based on the difference. Neighborhood is in compliance with ACA regulations.

Advertisement